Banking and Payments Intelligence Report

May 2023

Is Paze Ready to Fight Apple and PayPal in the Battle for Hearts and Minds of Consumers and Merchants?

Early Warning, the bank-owned operator of the peer-to-peer payments platform, Zelle, officially entered the digital payments gold rush last month when it announced plans to create a new digital wallet called Paze. The new service will compete directly with an increasingly crowded field of digital wallet providers including the likes of PayPal, Apple and Google.

The announcement signals that it is officially game-on in the battle between banks and fintechs to secure the hearts and minds of consumers and merchants. Ultimately, the outcome of this aggressive push to create new digital platforms and services will determine the future of the digital payments landscape.

Consumer Awareness

Early Warning’s decision to move into the digital wallet space is both a validation that financial services incumbents are not going to cede victory to fintechs and a clear sign to the marketplace that digital payments are here to stay, even after experiencing “bubble-esque” growth rates during the pandemic. In fact, according to JD Power data, the percentage of Americans that said that they used a mobile wallet for a purchase at some point in the previous three months increased from 45% in 2021 to 51% in 2022.

Despite the growing consumer interest and the huge boost Paze will have from its bank backers, the service will still have its work cut out for it when it comes to building customer awareness.

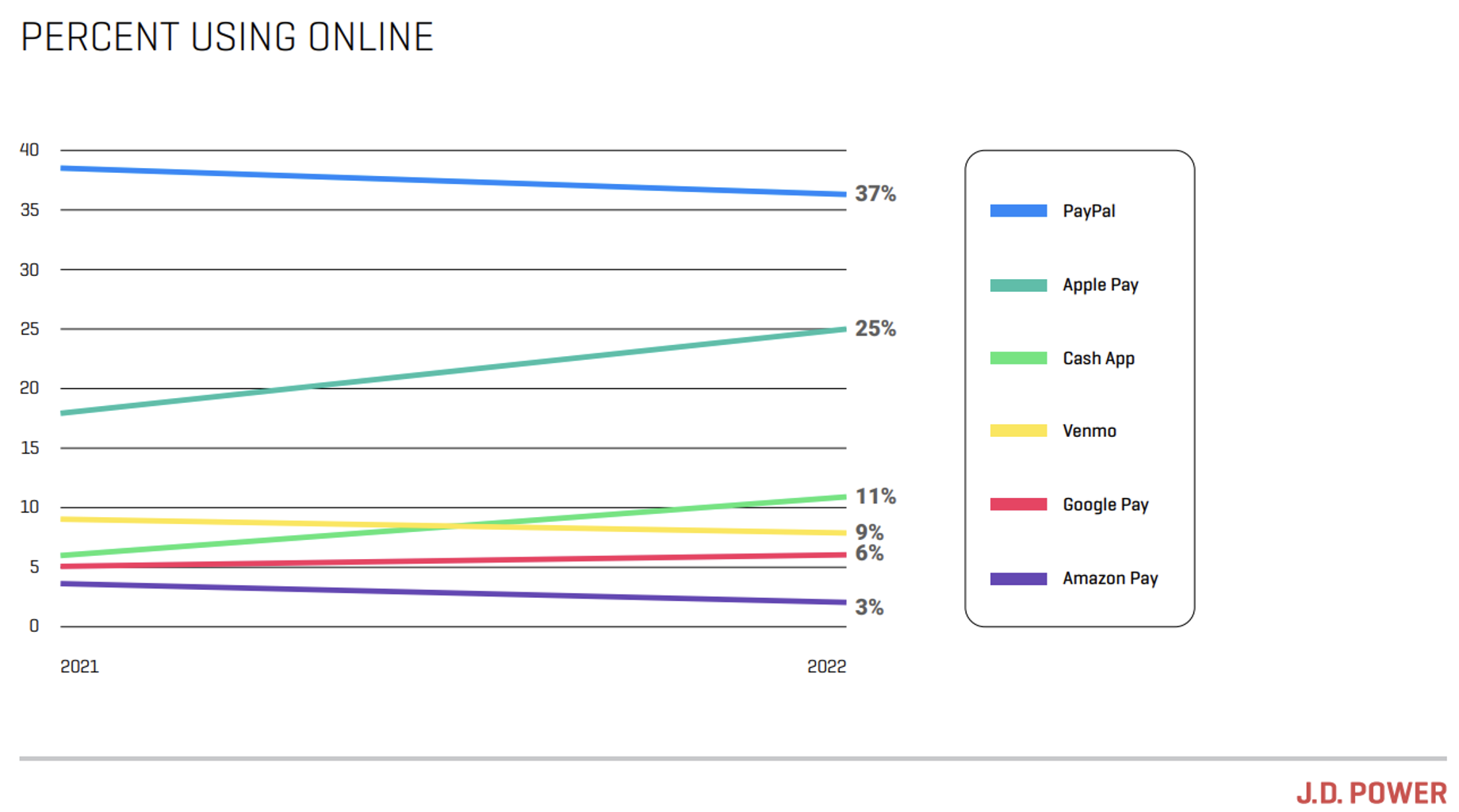

Overall, PayPal is the most recognized brand of digital wallets at 82%, followed by Apple Pay at 64% and Venmo at 60%, according to JD Power data. However, when it comes to consumer preference, PayPal is the most preferred digital wallet brand for online purchases (37%) while Apple Pay is most preferred in-store (33%). Google Pay follows just behind the leaders when it comes to brand awareness, with 53% brand recognition, but its point-of-sale consumer preference scores are considerably lower, with just 6% customer preference for online transactions and 7% consumer preference for in-store transactions.

Clearly, brand awareness is a big deal for consumers using digital wallet technology. PayPal is benefitting from its decade-long head-start in the space for online purchases and Apple is benefiting from sustained effective marketing to consumers and merchants alike. That level of awareness will be tough to fight.

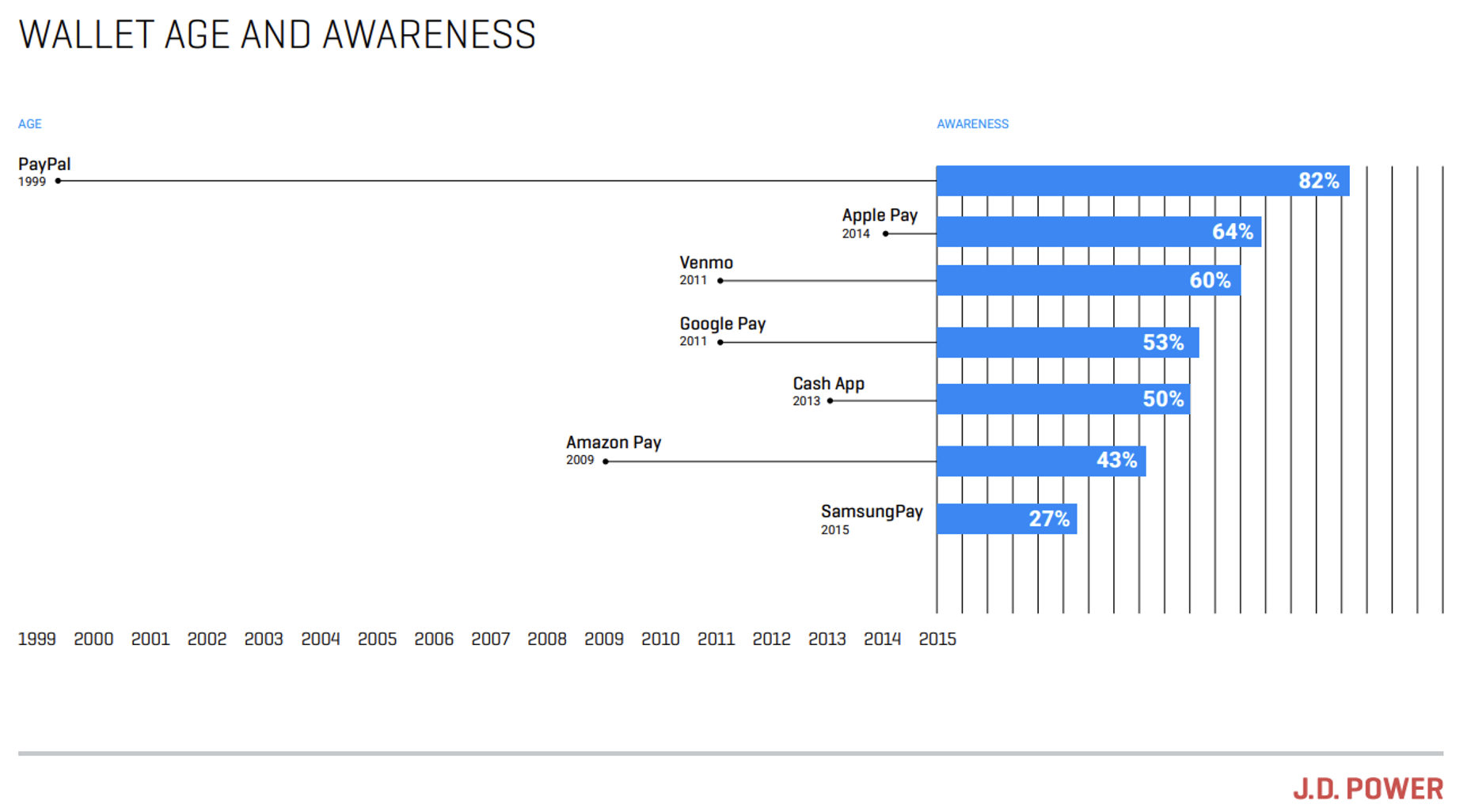

The importance of consumer awareness can be seen in the following chart, which illustrates digital wallet brand awareness based on the age of the service. While PayPal has been around the longest and has the highest overall level of brand awareness (82%), Apple Pay is relatively young by comparison and has already climbed to second place, with 64% total brand awareness.

While Apple Pay is one of the newest entrants in the space, it has established widespread awareness quickly through aggressive consumer and merchant-focused marketing efforts. SamsungPay, by contrast, was launched just one year after Apple Pay and is still at the bottom of the field in terms of customer awareness. Paze will need to move swiftly and effectively to build its brand.

Wooing Merchants

The other half of the equation, of course, is availability. Merchants need to accept these payment methods, and as digital payments platforms proliferate, that means making every payment option available at every point of possible interaction from the corner convenience store to the ecommerce website to the municipal parking meters that are increasingly fed with apps instead of quarters.

This is a hill that EWS will need to climb with its Paze digital wallet. The brand is entering the market with a big tailwind in the form of instant enrollment of more than 150 million credit cards, through its direct integration with bank networks. But the brand will need to generate merchant interest quickly by touting its vast network and, ideally, by introducing safe-pay features and other special benefits they can provide by virtue of their relationship with the big banks.

Sweetening the Deal

The wild card that is likely to start becoming a bigger factor in consumer adoption of digital payments and digital wallet technologies is incentives. Right now, the space is so new, that most customers are stumbling into a provider through a combination of general brand awareness and convenience. Perhaps they are at the check-out of an ecommerce site and a handful of options are presented and they pick the one for which they remember the password, or the one they used last time. Perhaps they are Android users and already have Google Pay loaded on their phones, or iPhone users with Apple Pay. It’s still early days and consumers are experimenting.

As digital payment consumers get more sophisticated, however, patterns of usage will evolve and customers will be swayed by incentives. Google Pay, for example, has already started offering rewards on every purchase, similar to the model followed by virtually every major credit card provider. Expect to see this area heat up if Paze begins to scale.

While Paze does have some significant advantages going for it, largely by virtue of its built-in relationship with the major banks, this space has grown so quickly and is becoming so competitive, that it will take more than just availability to open the new customer floodgates. Early Warning will need to double-down on consumer brand building, merchant relationship development, and perhaps incentives before Paze can become an entrenched part of rapidly changing patterns of consumer behavior.

Find out More

This Banking and Payments Intelligence Report is based on data from the JD Power U.S. Retail Banking Satisfaction Study, which is a yearly study that includes more than 20,000 responses annually, and the U.S. Merchant Services Satisfaction Study, which collects customer satisfaction data from over 4,000 small business customers of merchant services providers. It was authored by Miles Tullo, Managing Director of Banking and Payments at JD Power. Please contact us at the numbers below to connect with Mr. Tullo or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]