Banking and Payments Intelligence Report

December 2023

Financial Malaise Forces Bank Customers in the U.S. to Revamp their Holiday Plans

While the United States economy experienced virtually an across-the-board rally in November, financial sentiment among bank customers in the U.S. remains stubbornly low, and it is leading to many re-thinking their 2023 holiday plans.

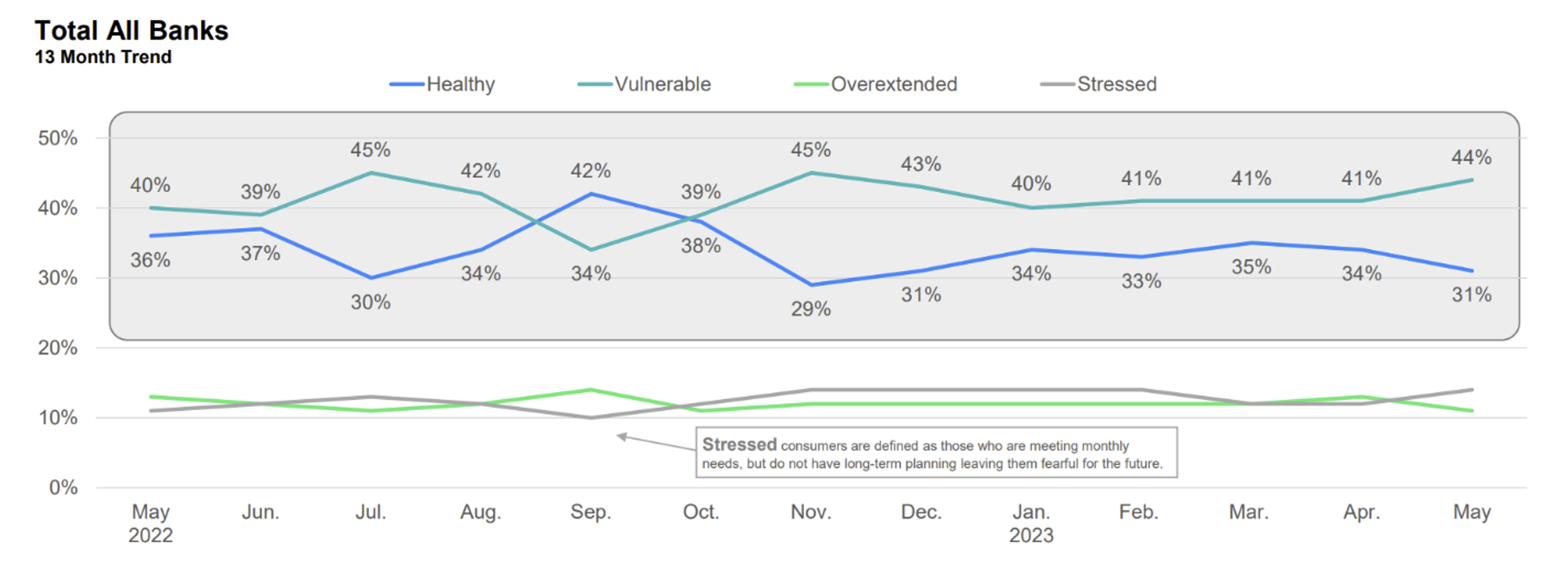

According to JD Power, the percentage of U.S. bank customers that are financially healthy[1] has fallen to an all-time low. As a result, some customers are pumping the breaks on their plans to spend and travel this December.

Financial Erosion Continues

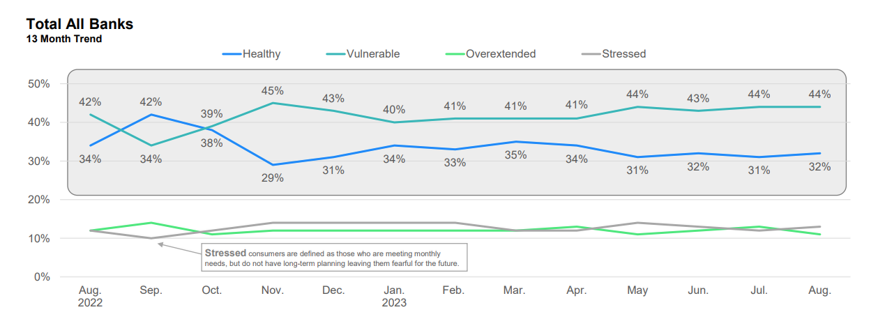

Customers’ financial health has sunk to an all-time low. Just more than one-fourth (28%) of respondents are financially healthy, while 48% fall into the vulnerable category. Those numbers paint a bleaker picture than two months ago, when the previous grim benchmarks were established.

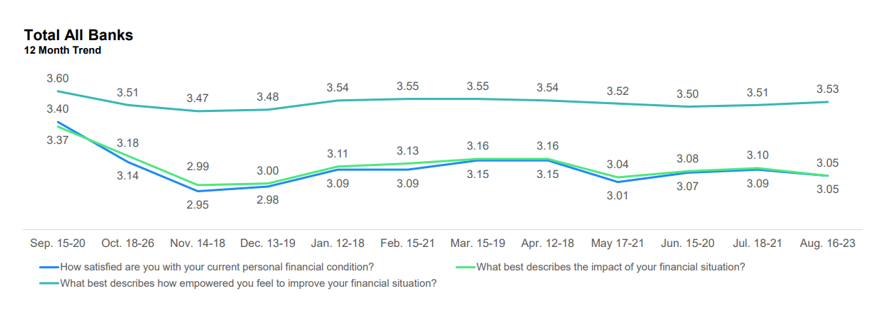

Customer sentiment regarding financial health status, stress levels and empowerment to improve one’s financial situation all remain stubbornly low, as a sense of malaise has begun to affect a wide swath of consumers.

Santa Maybe

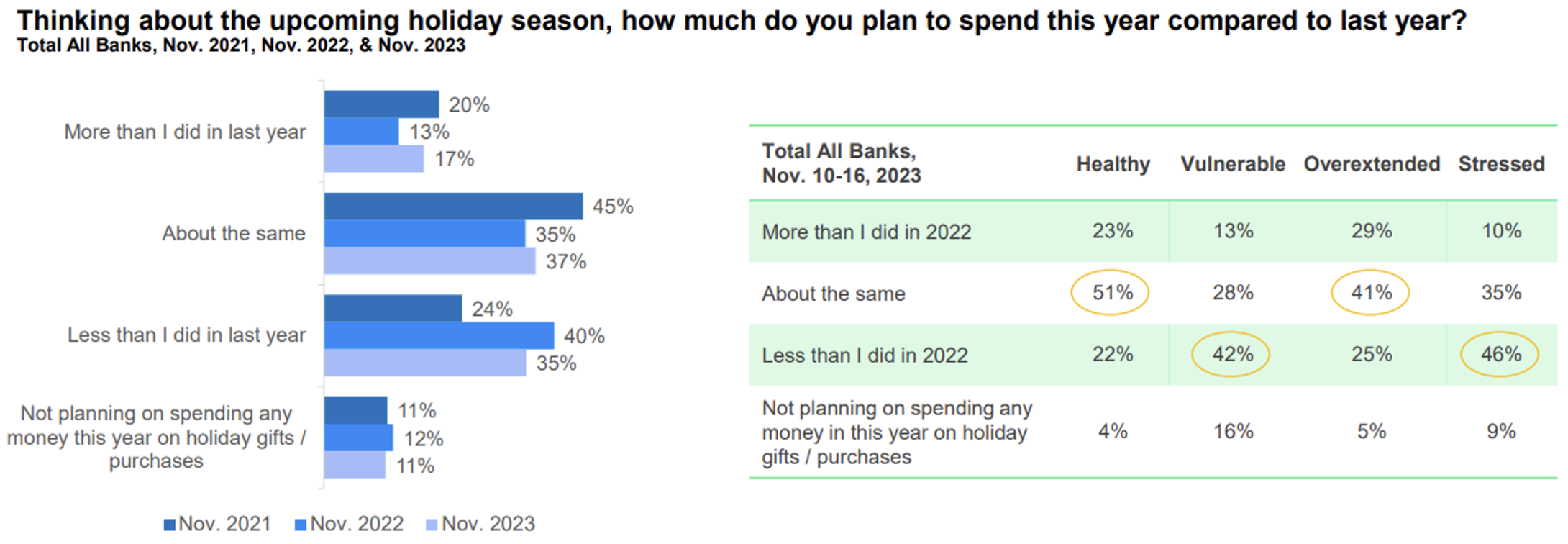

With the holiday season upon us, 35% of customers say they plan to spend less on holiday shopping than last year. That is down from 40% a year ago, but still reflects a significant number of customers looking to cut costs by skimping on the holidays. Just 17% said they plan to spend more than a year ago. Somewhat confoundingly, the overextended population (29%) is the more likely to say they plan to spend more than they did in 2022.

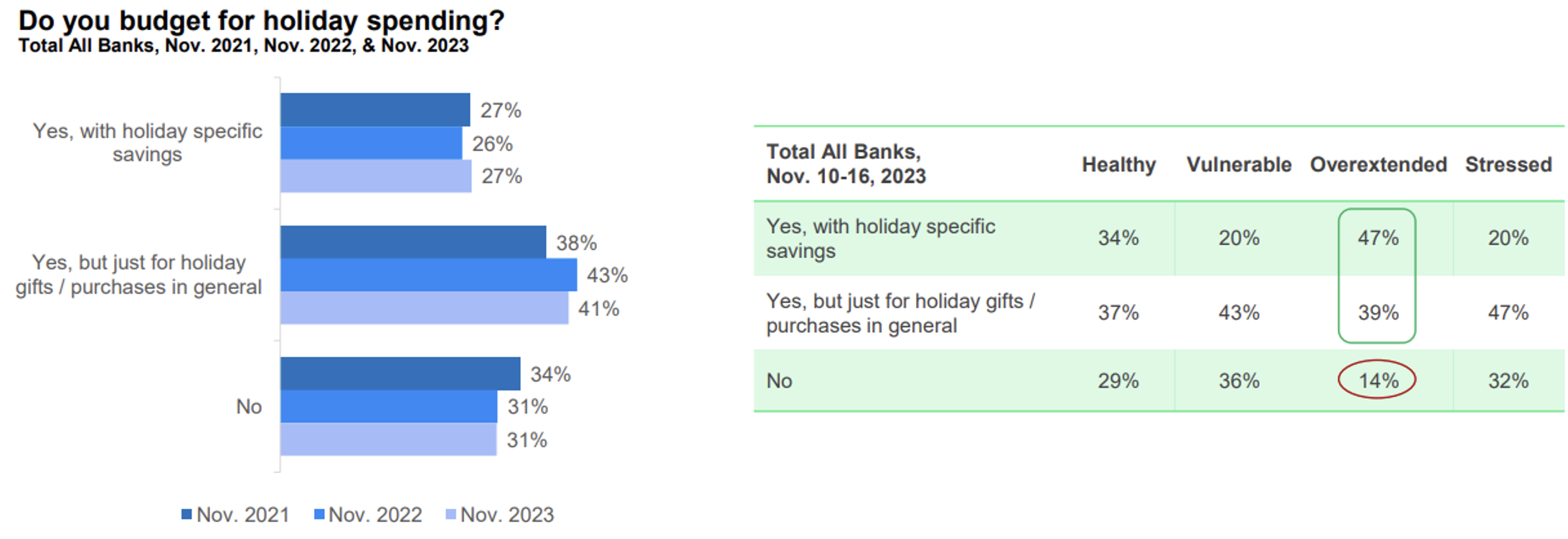

Despite persistent price concerns and eroding financial health, the proportion of customers who budget for the holidays is not increasing over time. Nearly one-third (31%) said they do not budget for holidays spending, a rate that included 36% of the vulnerable population and 32% of the stressed population.

Home for the Holidays

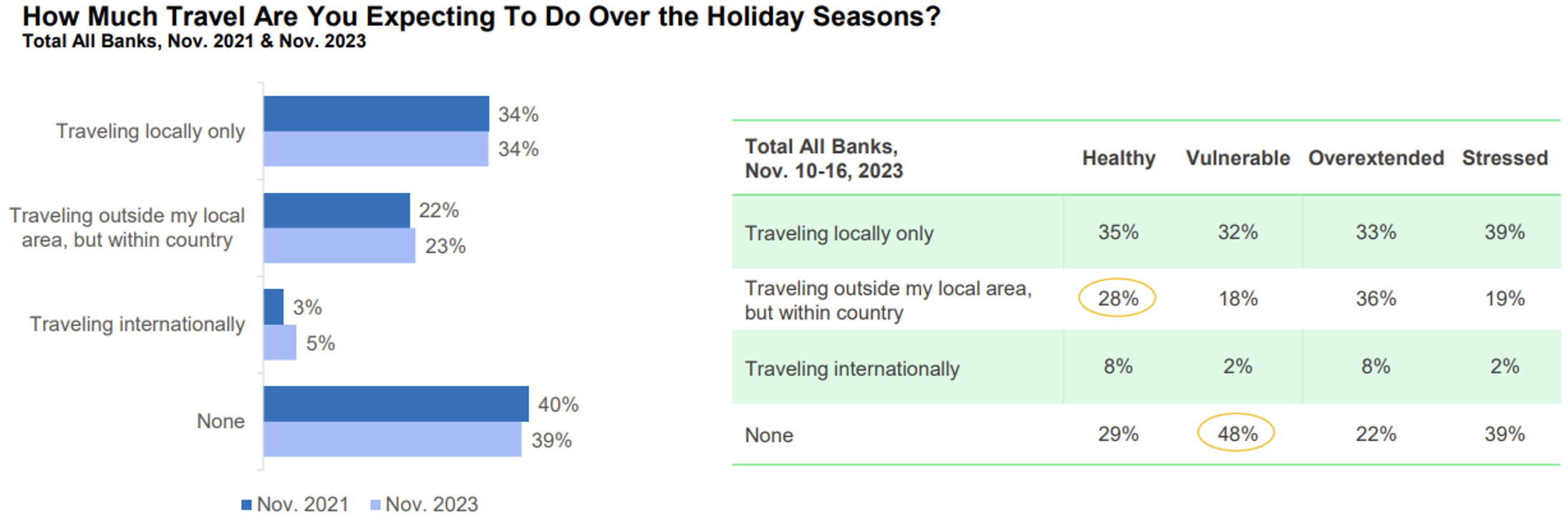

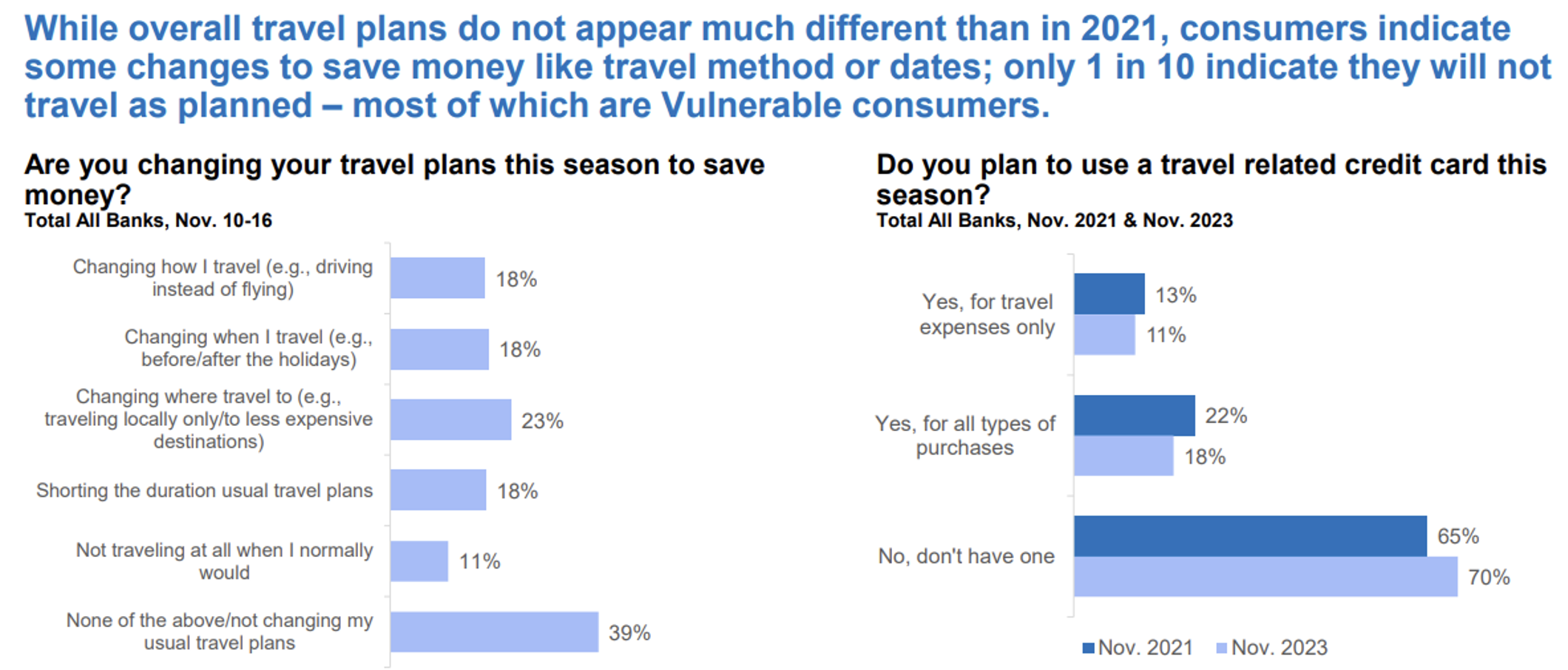

Customers appear to be content to remain in their own homes for the holidays, as 39% said they do not plan to travel during the season. That’s in line with two years ago (41%), but it’s worth nothing that the 2021 season still included widespread lingering concerns about the pandemic, a variable that is likely not a factor with the bulk of customers anymore.

For those that have decided to take a holiday trip, the majority are changing the way they travel. Nearly one-fourth (23%) of customers that intend to travel are changing their destination to somewhere local and/or less expensive, while 18% say they are changing when they travel, and another 18% say they are changing how they travel (i.e., driving instead of flying).

Early Financial Resolutions

Just like a month ago, it seems like there is a disconnect between the positive financial reports from the press and the muted reality that many customers in the U.S. are living. Holiday spending and travel are usually good indicators of how healthy most Americans are, and these data make that a sobering thought.

Still, as the calendar prepares to turn to the new year, there are plenty of opportunities for banks to help their customers navigate their way through a tenuous time of year. For example, budgeting solutions are desperately in need for the bulk of the population. Customers that find that this assistance can be beneficial now may develop healthier habits, which can help banks forge more meaningful relationships and customers into better financial situations.

Find out More

This Banking and Payments Intelligence Report is based on responses from 4,000 retail bank customers nationwide and was fielded in November 2023. It was authored by Jennifer White, senior director of banking and payments intelligence at JD Power. Please contact us at the numbers below to connect with Ms. White or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]

[1] JD Power measures the financial health of any consumer as a metric combining their spending/savings ratio, creditworthiness, and safety net items like insurance coverage. Consumers are placed on a continuum from healthy to vulnerable.