By embracing innovation and prioritizing personalized experiences, banks and credit card providers can redefine their role in enhancing financial well-being. We unpack the latest insights from the 2024 U.S. Retail Banking Advice Satisfaction Study in the June 2024 JD Power Financial Services Intelligence.

Here are some key insights that you can’t miss:

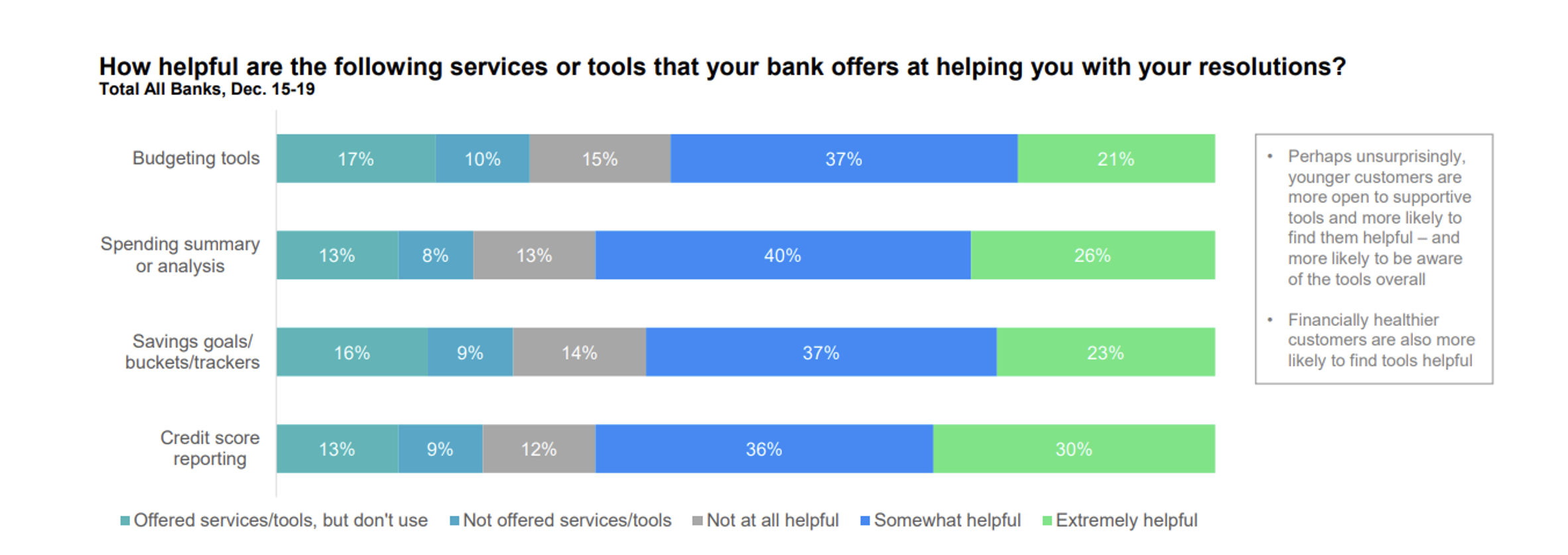

- Youthful Engagement: Younger consumers (<40) are actively seeking personalized financial advice. While they act on the advice received, satisfaction levels indicate room for improvement. Delivering robust tools and services alongside advice is crucial.

- Industry Standard Setters: Leaders like Citi, Bank of America, Chase, and American Express set benchmarks with proactive financial guidance, defining satisfaction norms.

- Frequency Optimization: Increasing interaction frequency across digital and traditional channels enhances satisfaction, engagement, and loyalty. A multichannel approach ensures comprehensive service accessibility.

Watch the full video for impactful insights on how improving customers’ financial health impacts loyalty and advocacy.

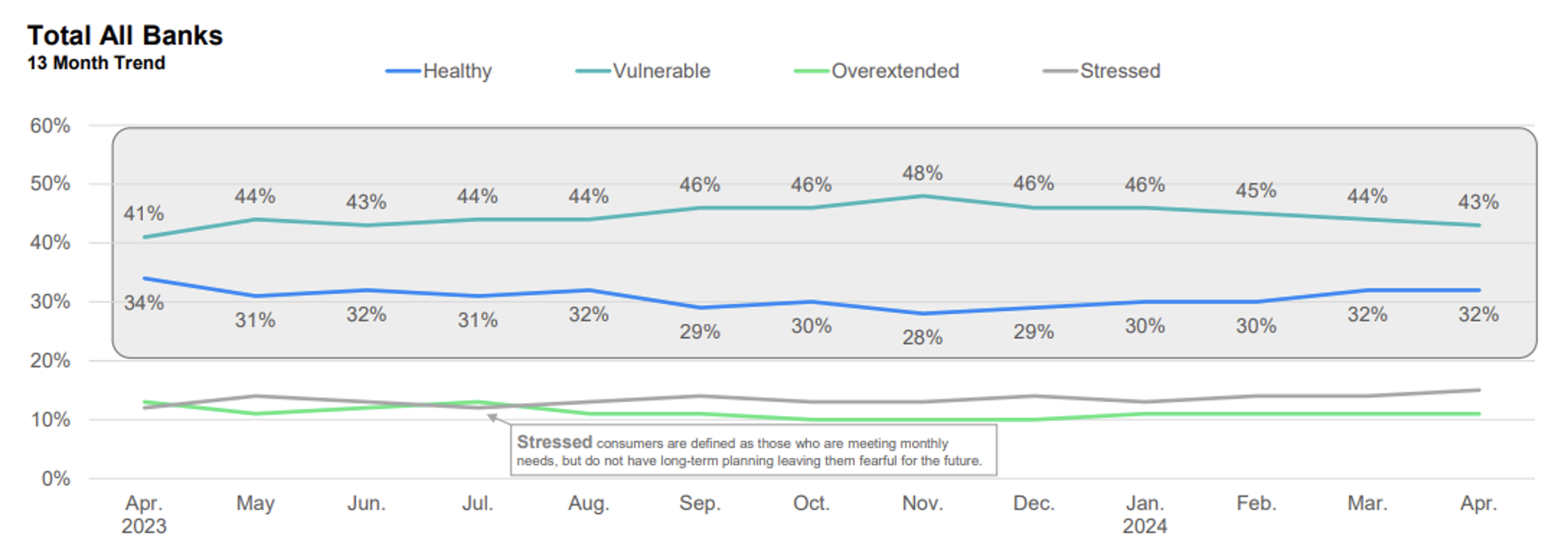

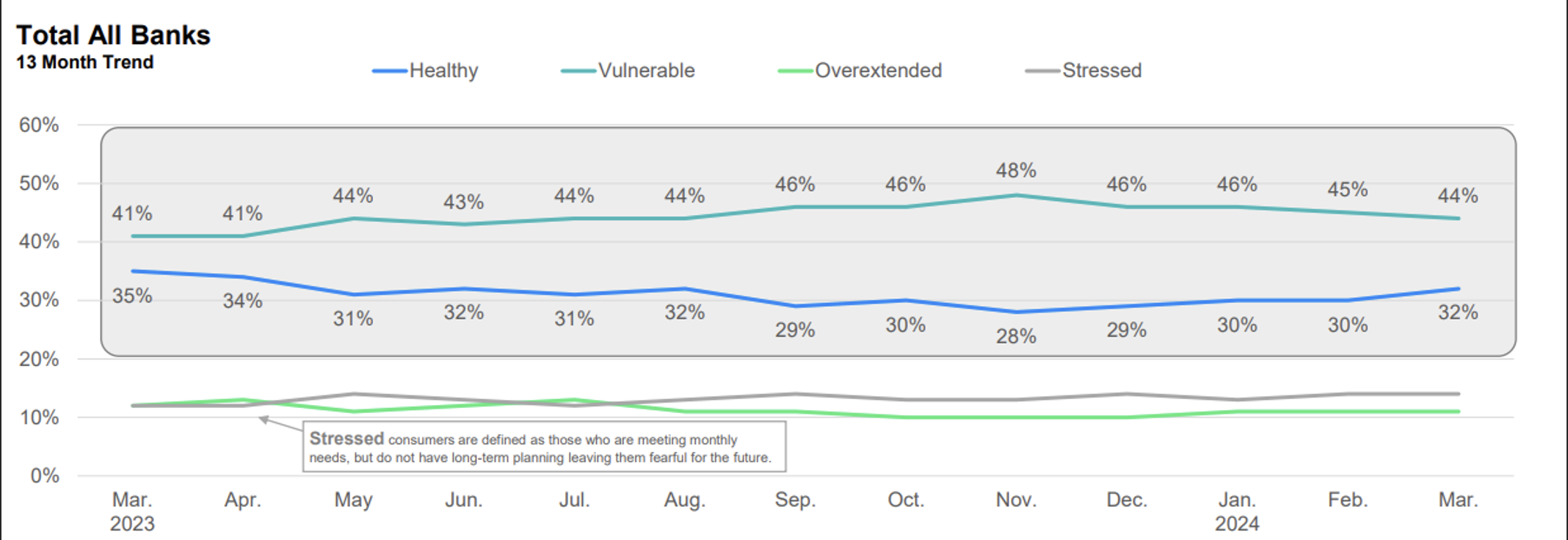

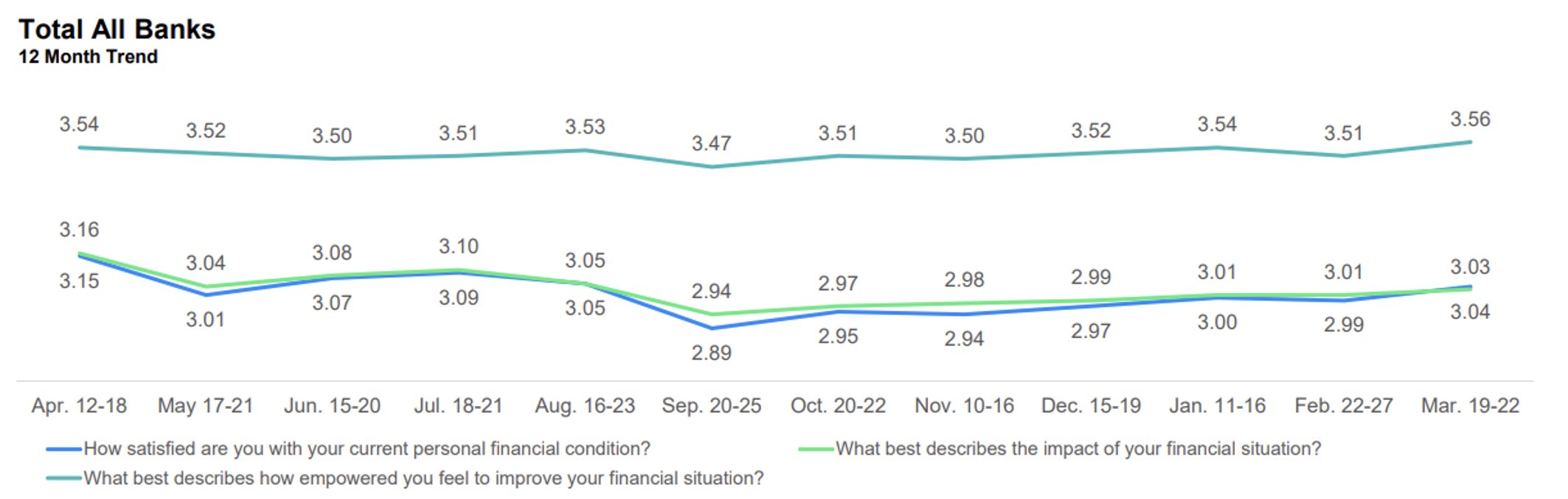

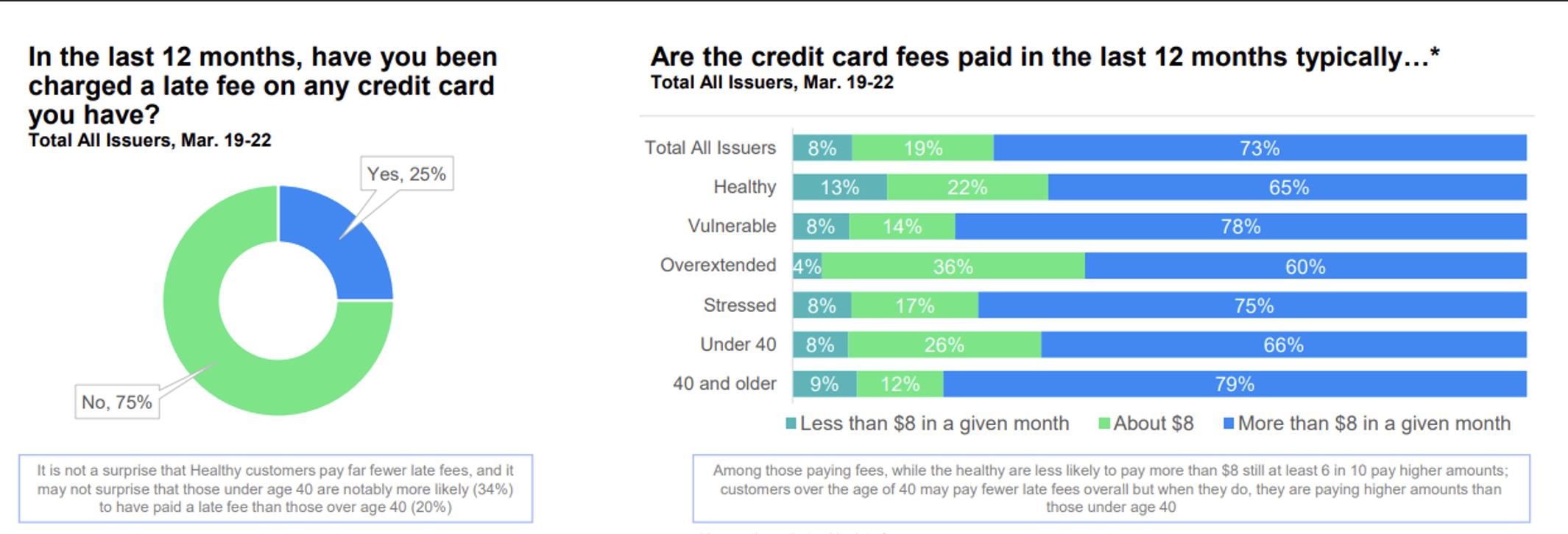

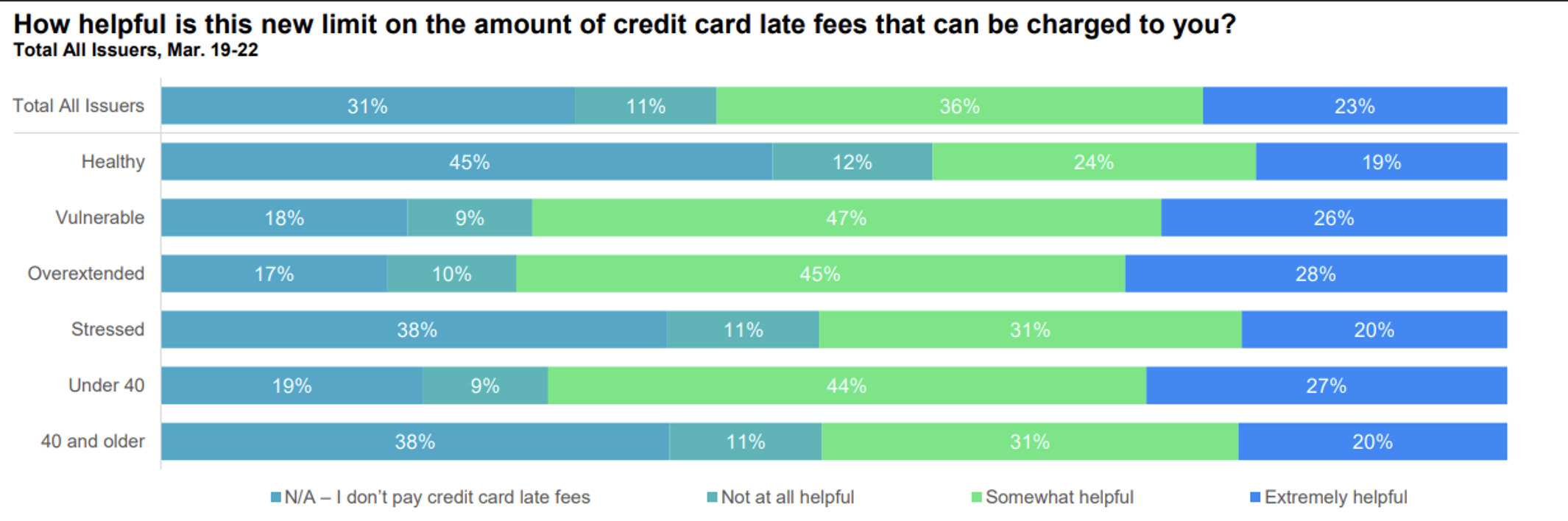

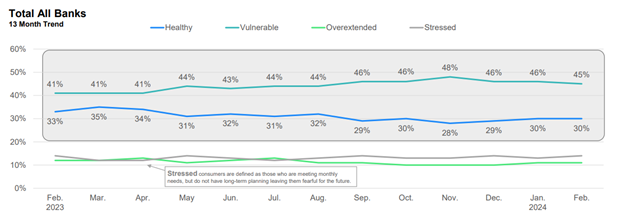

Bonus Content: Financial Health Personas

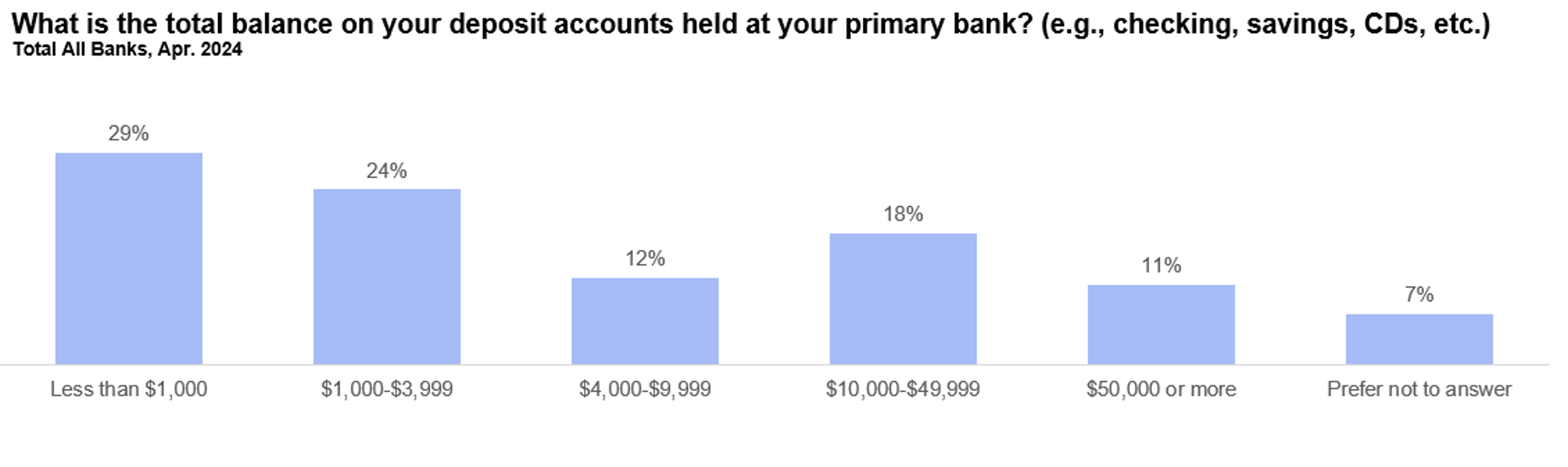

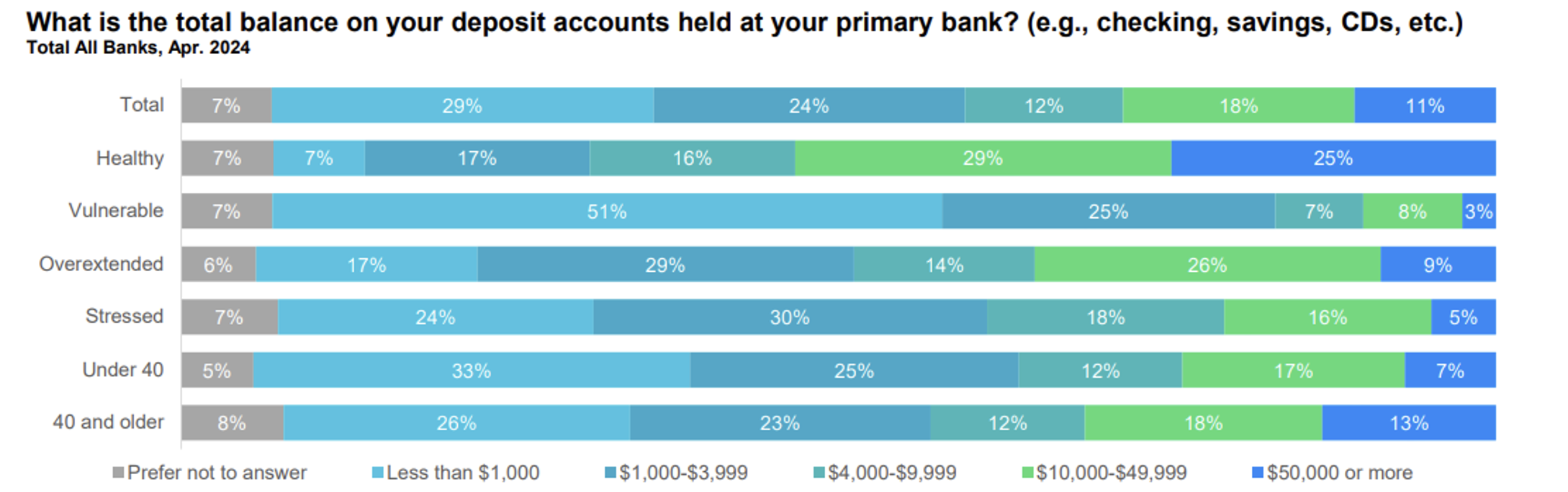

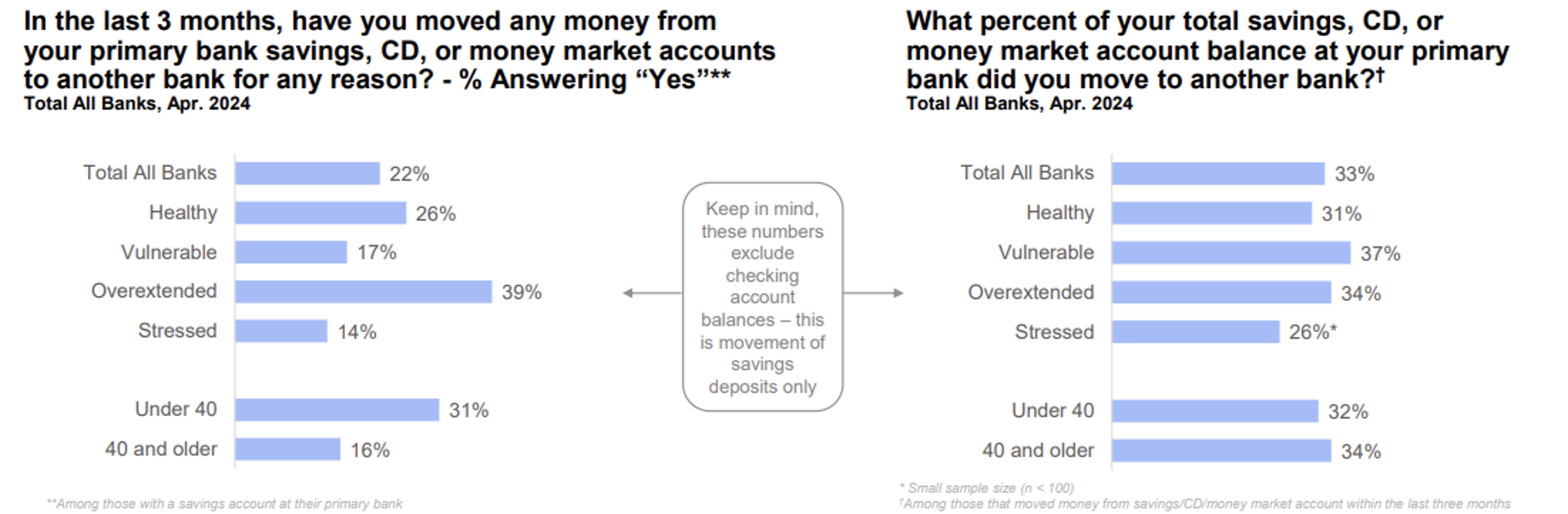

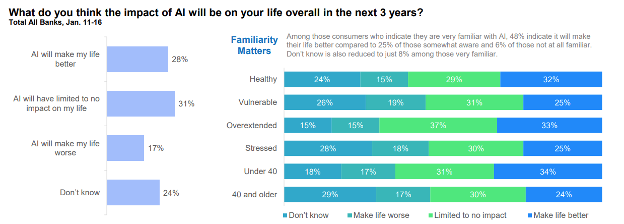

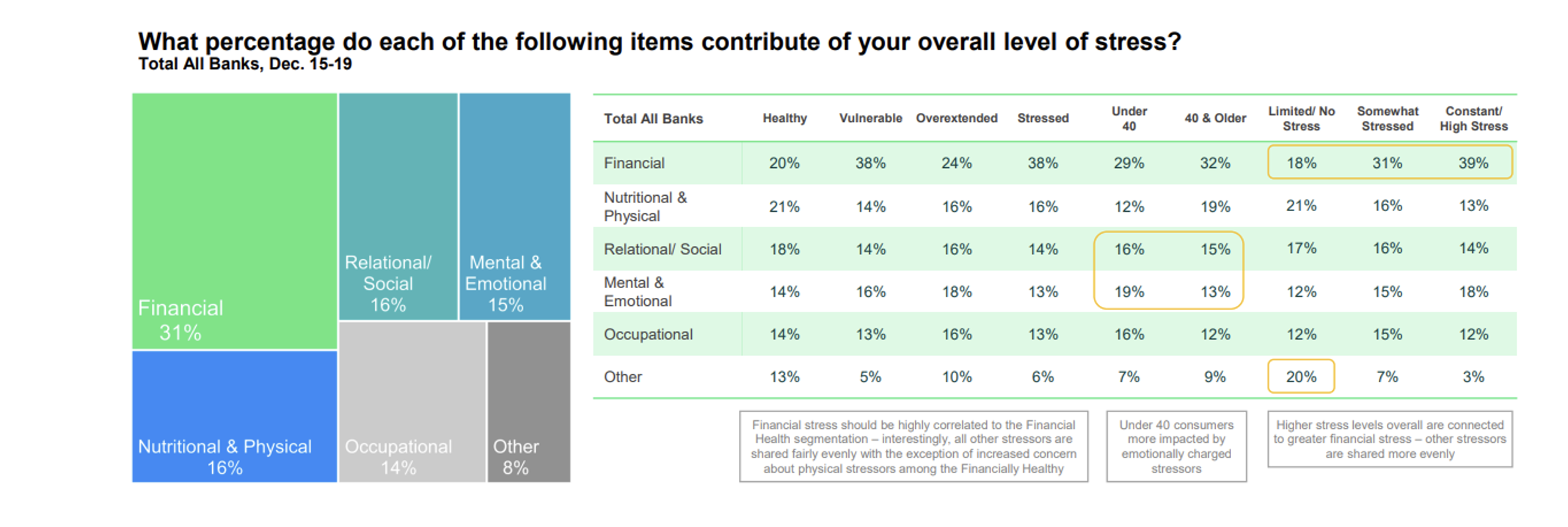

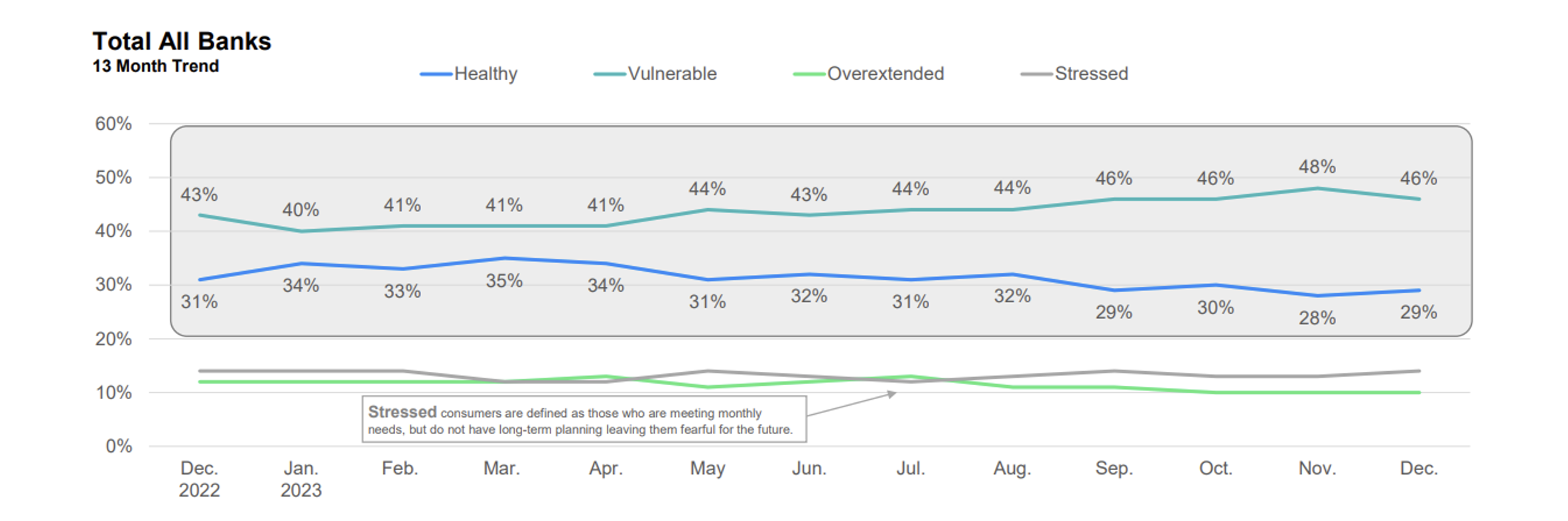

Understand the different groupings that Jennifer referenced in this edition of Financial Services Update. Your teams can begin to personalize financial services with strategic segmentation based on customer financial health personas. Access key demographics on the financially healthy, vulnerable, overextended, and stressed personas.

Where can you find more insights like this?

The JD Power U.S. Financial Health and Advice Program empowers banks and credit card providers to elevate customer financial wellness. By analyzing deep consumer insights and benchmarking performance, financial institutions can enhance their advisory services. Leveraging this data enables banks and credit card providers to optimize customer satisfaction, implement best practices, and refine strategies for superior financial outcomes. This proactive approach not only boosts service quality but also strengthens customer loyalty and market competitiveness.

More About These Experts

Jennifer White is the Senior Director of Banking and Payments Intelligence at JD Power, is pivotal in shaping the financial industry’s understanding of consumer behavior. With over 20 years of market research experience, Jennifer leads prestigious studies, including the Retail Banking Satisfaction Studies and the Financial Health & Advice Program, driving critical insights that influence banking strategies across the U.S. and Canada. Her work on consumer financial health, digital banking trends, and fraud impacts is highly regarded and widely featured in top-tier publications like Forbes, The New York Times, and The Wall Street Journal. A respected thought leader and speaker, Jennifer’s expertise helps financial institutions enhance customer satisfaction, loyalty, and trust through innovative, data-driven strategies.

Miles Tullo is the managing director of the JD Power Financial Services team. He oversees the company’s consumer payments program, focusing on point-of-sale choice and non-credit card payment methods. Drawing from over 20 years of experience in both payments and mortgage lending, Miles brings valuable expertise to clients.