Cracking the Code on Affluent Clients: Trust, Technology, and Opportunity

VIDEO: Financial Services Intelligence Update — January 2025

When it comes to affluent consumers, one thing stands out above all else: trust. It’s not just important—it’s the ultimate differentiator. As wealth transfers between generations and new technologies reshape the industry, JD Power’s latest research offers exclusive insights into how banks and wealth firms can meet—and exceed—the expectations of their most valuable clients.

In the newly released JD Power Affluent Client Trend Report, JD Power combines several benchmark studies to provide valuable insights into the affluent and emerging affluent customer base. Drawing on data from more than 250 financial institutions, we highlight key trends and strategies that can drive loyalty and growth with these valuable customers.

To explore how firms can better serve this critical demographic, JD Power’s Craig Martin, Executive Managing Director at JD Power, joined Miles Tullo, Managing Direct, for a deep dive into the evolving landscape of affluent clients.

Key Insights for Winning Affluent Clients’ Trust and Loyalty in 2025

- Trust Is Multifaceted: While banks earn high marks on transactional trust—ensuring secure, efficient daily operations—wealth firms excel in building holistic, goals-based relationships.

- Generational Wealth and Opportunity: Younger consumers represent untapped potential, but firms need tailored strategies to engage this demographic.

- Technology Meets Strategy: As artificial intelligence and digital tools transform the financial industry, aligning these innovations with human-centric approaches will be essential for success.

Understanding the Affluent Client

Craig Martin explains that affluent clients are not a monolithic group. Their behaviors, preferences, and trust levels vary across age groups and wealth tiers. While Baby Boomers typically have established financial relationships, younger affluent consumers represent a significant growth opportunity for both banks and wealth firms.

“Understanding the affluent consumer requires delving into the nuances of these groups and addressing what truly builds trust. It’s not just about satisfaction—it’s about creating loyal brand advocates,” Martin said.

Trust: The Cornerstone of Client Relationships

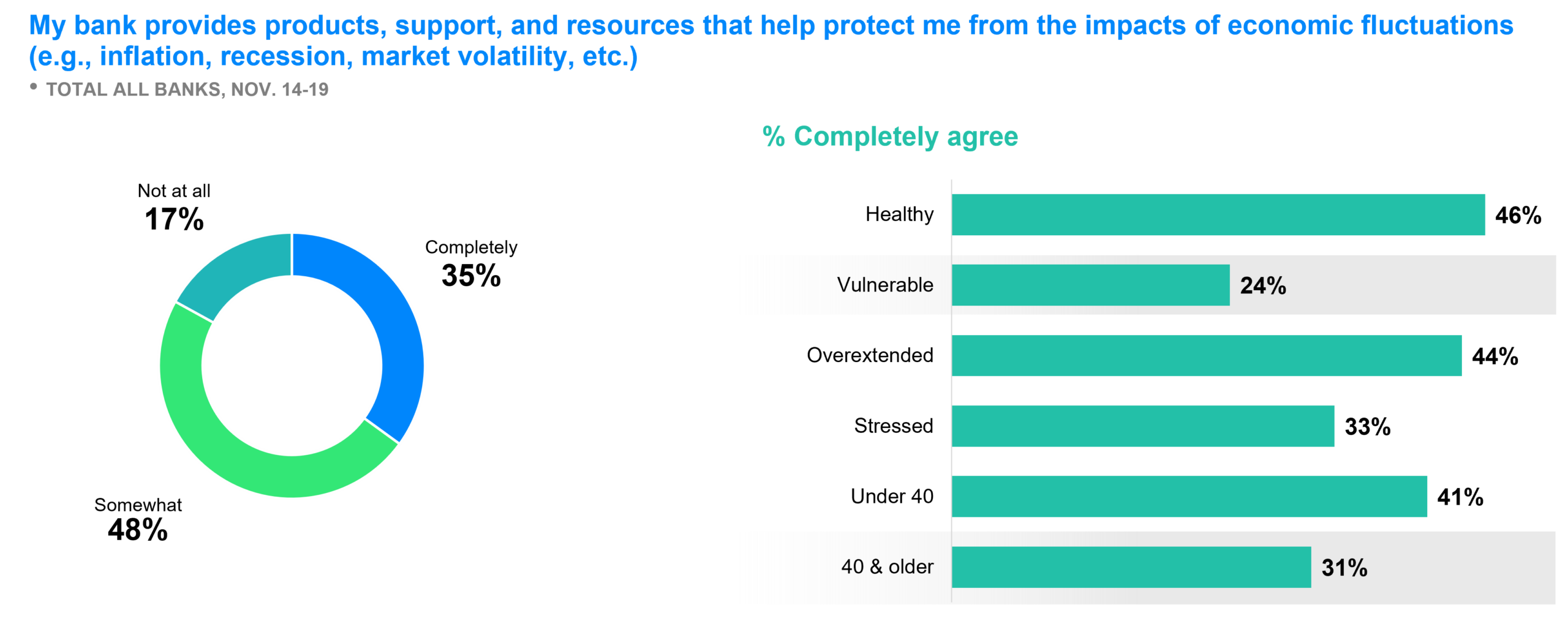

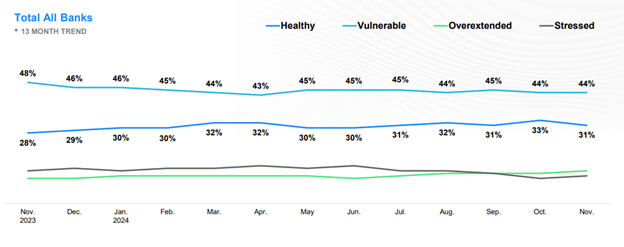

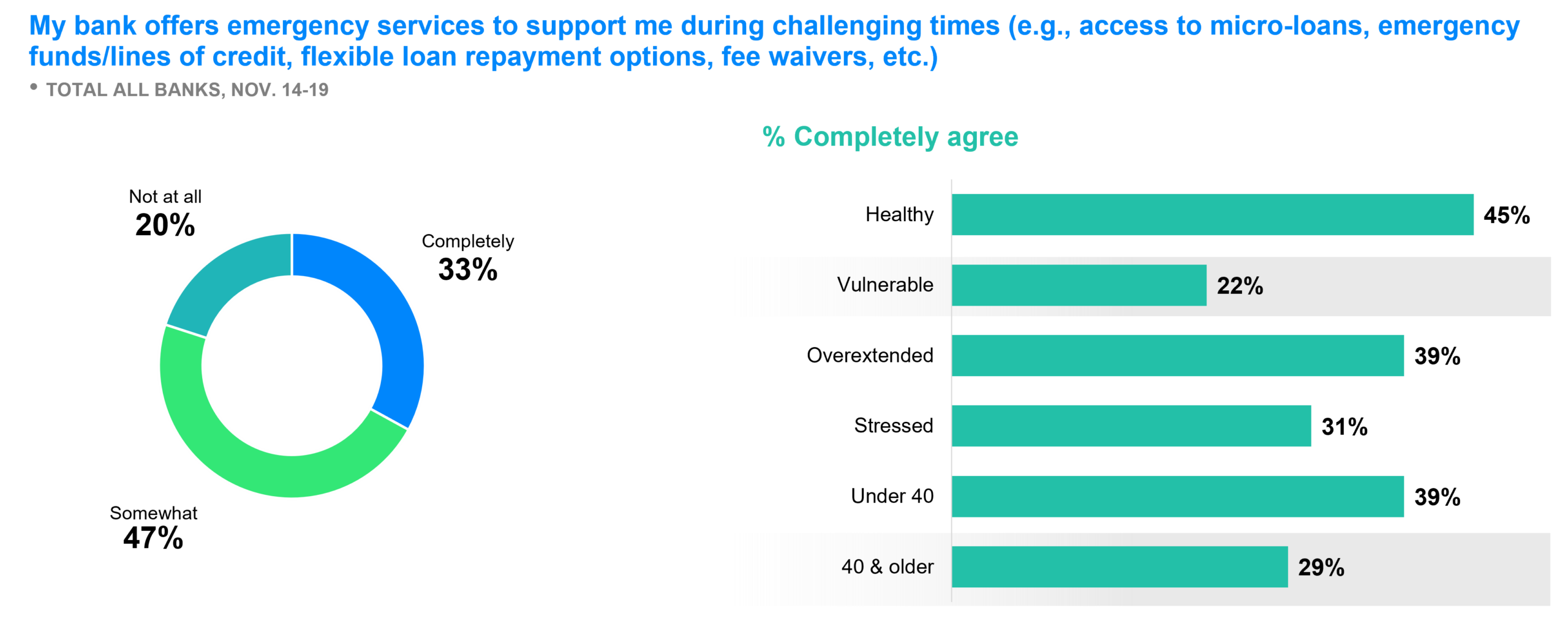

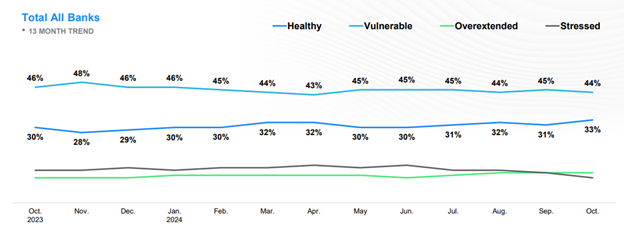

Trust emerged as a central theme in the conversation. The report reveals that wealth firms are generally more successful at establishing high trust levels than banks. Affluent clients have different trust expectations depending on whether they interact with a bank or a wealth manager.

“For banks, trust is often linked to transactional reliability—keeping data secure, offering seamless transfers, and maintaining technical soundness,” Martin explained. “For wealth managers, trust goes beyond transactions, requiring a focus on relationship-building and personalized advice.”

A Data-Driven Approach to Growth

The Affluent Client Trend Report offers more than just trends—it provides actionable insights. By analyzing the behaviors of over 10,000 consumers, the report outlines ways firms can:

- Leverage AI and digital tools to personalize services.

- Adapt strategies for generational wealth transfers.

- Prioritize high-value opportunities in a competitive landscape.

Martin emphasized the need for strategic resource allocation: “Firms don’t have unlimited budgets or personnel. The challenge lies in determining how to prioritize investments in technology, people, and processes to meet the evolving needs of affluent clients.”

When it comes to affluent consumers, trust is more than just a factor—it’s the key to winning their loyalty

Preview the Affluent Client Report

The JD Power Affluent Client Trend Report is now available for preview. The report offers exclusive insights into the behaviors and expectations of affluent consumers, along with key trends and strategies for driving loyalty and growth. Preview the report today.

Preview now: Affluent Client Trends Report Preview

Craig Martin is the executive managing director, dedicated to driving positive change in the financial services sector and helping clients achieve superior business outcomes by focusing on their customers.

Craig’s insights have been featured in numerous publications addressing customer experience and the correlation between customer satisfaction and business success.

Miles Tullo is Managing Director of Financial Services at JD Power. He oversees client engagement with financial services clients in North America. Drawing from extensive experience in payments and lending, Miles brings valuable expertise to clients and contributes regularly to JD Power’s thought leadership initiatives.