Utilities Intelligence Report

March 2023

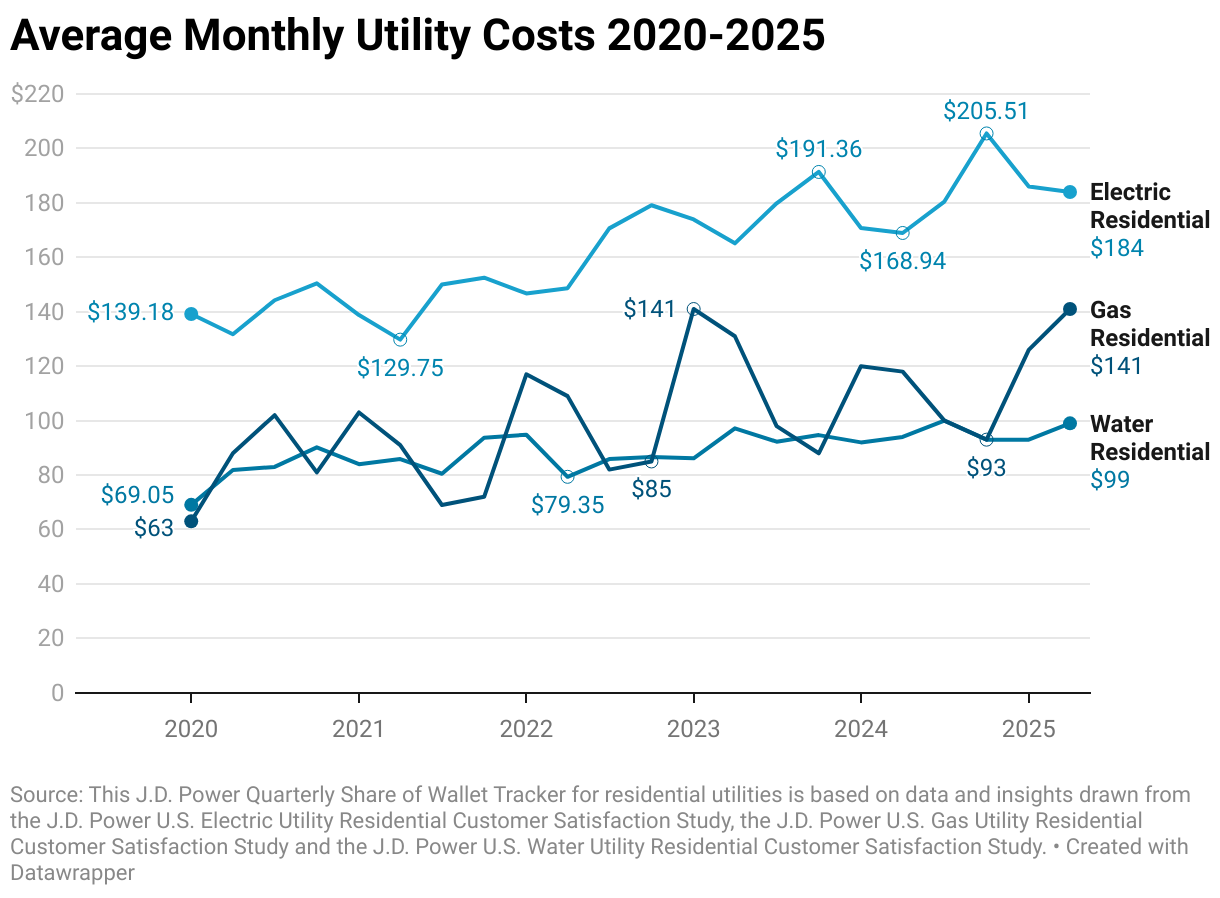

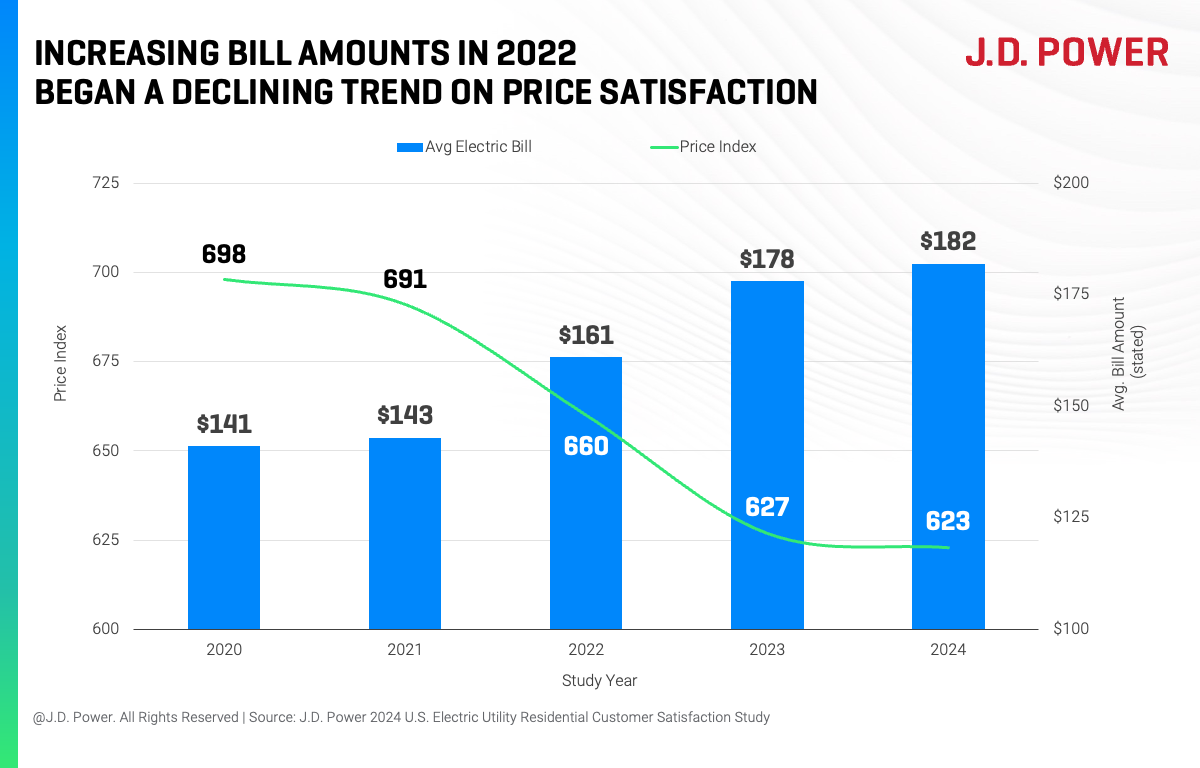

Electricity bills in the United States rose 13.1% on average in 2022, higher than the overall rate of inflation. Concurrent with this trend, utilities have introduced aggressive carbon reduction goals and sustainability initiatives that rely on customers reducing their energy consumption through a combination of time-of-use rates, energy-saving appliance rebate programs and more.

In fact, 81% of electric utility customers are now served by a utility with a stated carbon reduction target. Despite this decade-long push to change emissions by spurring customer participation in these programs, many customers are completely unaware that energy conservation and sustainability programs even exist. Is the recent run-up in electricity prices proving the catalyst to finally change consumer behavior?

According to the latest JD Power data, even record high energy prices haven’t been enough to spur a significant increase in awareness of energy conservation and sustainability initiatives. However, a handful of utilities are starting to see their investments in sustainability pay off in the form of improved customer satisfaction and increased perceptions of affordability among customers. While these examples are in the minority, they offer a playbook for strategies that are working when it comes to consumer awareness of utility sustainability initiatives.

Ultimately, our research finds that utilities with a clearly stated sustainability goal, a concerted plan to achieve that goal and widespread support for that plan among customers are slowly changing customer behaviors and perceptions. These examples are rare, however, and the vast majority of electric utilities and utility customers are largely in the dark on sustainability and energy conservation initiatives – even as record high prices are hitting their wallets each month. Without a dramatic change of course, these utilities will struggle to meet their sustainability targets.

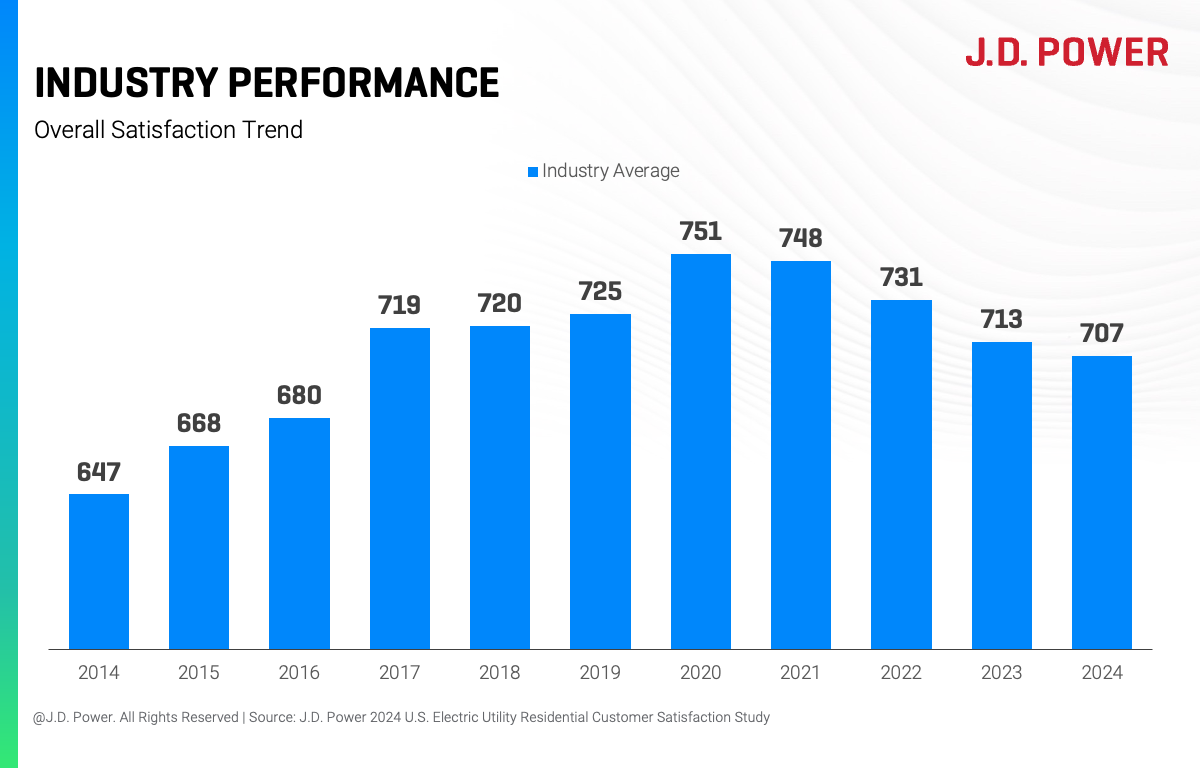

RECORD HIGH RESIDENTIAL ELECTRICITY PRICES DECOUPLED FROM SUSTAINABILITY

Customers in the U.S. are notoriously sensitive to changes in commodity prices and those changes often influence behavior. We see this trend prominently in our automotive data set, where incremental movements in the price per gallon of gas are directly correlated with consumer interest in electric vehicles, and, conversely how those rising fuel prices negatively affect the sale of large, gas-powered SUVs. The same cannot be said, however, for the correlation between rising electricity prices and consumer participation in utility energy management programs.

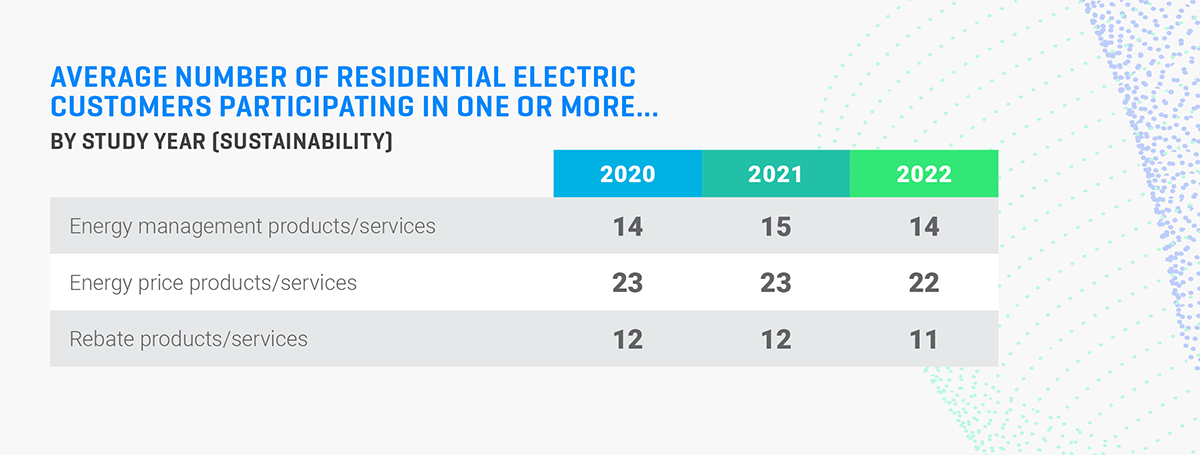

In fact, according to our data, just 14% of residential electric utility customers participated in one or more energy management programs offered by their utilities in 2022, a rate that was unchanged from 2020. Perhaps even more surprising, the number of residential electric customers participating in one or more price reduction or rebate programs, such as those offering discounts for using energy-efficient appliances, actually declined one percentage point between 2020 and 2022.

PERSISTENTLY LOW LEVELS OF CUSTOMER AWARENESS

The likely driver of these low participation rates is lack of customer awareness. Unlike the auto industry, which blankets the airwaves, news headlines and social media feeds with special offers on hybrids and EVs, the moment the national average gas price crests the $3.25 per gallon mark, the nation’s electric utilities have struggled to build awareness for consumer participation in their energy conservation programs.

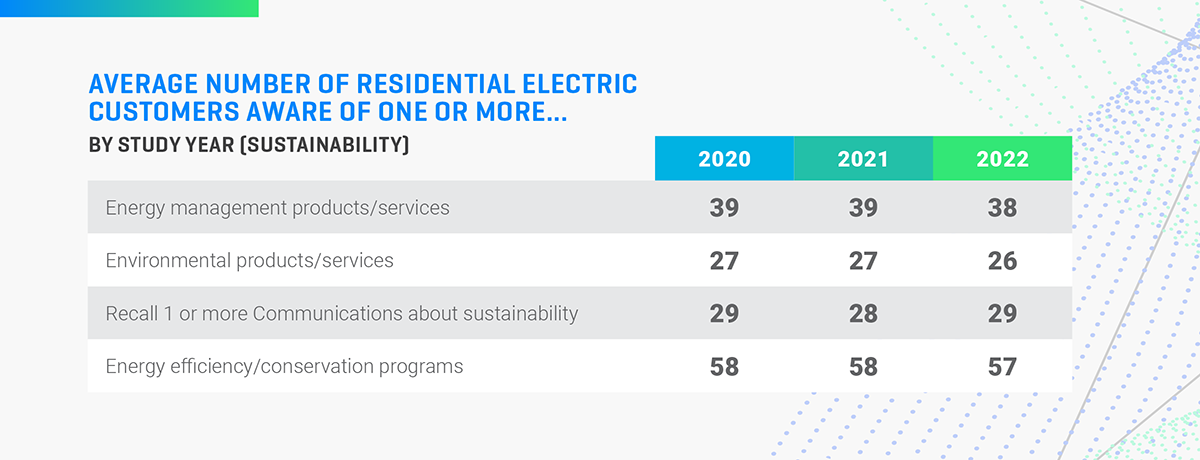

According to our data, just 38% of residential electric utility customers were aware of one or more energy management product or service and just 26% were aware of one or more environmental product or service through the end of 2022. Both numbers are down one percentage point from 2020. Likewise, consumer awareness for utility efforts to increase the use of clean energy and recall of any utility communications about sustainability have been flat at 28% and 29%, respectively, for the past three years.

WHAT WILL IT TAKE TO FORCE A BEHAVIOR CHANGE?

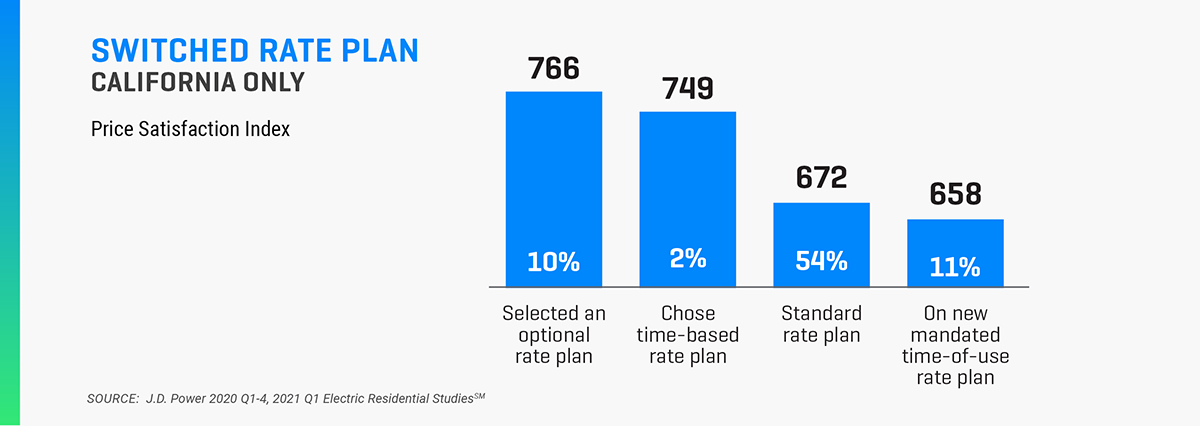

While very few U.S. electric utilities have the customer awareness and support they will need to meet their stated carbon reduction targets, some pioneers have taken a more aggressive approach to getting customers to change their behaviors by introducing time of use (ToU) rates. This pricing scheme, which sets different rates for electricity use based on hours of peak demand during, is meant to encourage use of high-energy consuming tasks—such as dishwasher and washer and dryer use—outside of the hours of peak demand on the power grid. In California, for example, the Public Utility Commission (CPUC) has mandated that all investor-owned utilities operating in the state adopt new ToU rate structures.

The California program was first piloted in 2016 and we’ve been tracking customer experience with it since 2018. Overall, we’ve found that customers who proactively chose to be part of a ToU have had significantly higher levels of customer satisfaction and improved perception of affordability. However, when customers were mandated to participate in these programs, satisfaction scores plummeted. Verbatim responses from consumers who were forced into these programs ranged from simple gripes like: “Lose the time-of-day usage,” to more urgent pleas: “The new increased rate for electric use from 4 to 9 p.m. has raised our bill significantly even though we do much to conserve.”

Source: JD Power 2020 Q1-4, 2021 Q1 Electric Residential StudiesSM

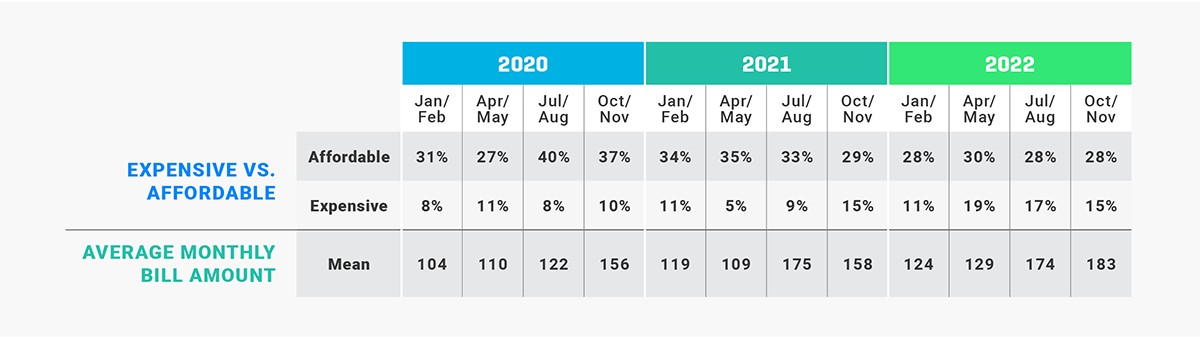

Among the few electric utilities that have been able to successfully manage this transition, the Sacramento Municipal Utility District (SMUD) has been able to burnish its image with its customers by carefully communicating its goal, putting a defined plan behind it and slowly building customer support. Throughout the first three years of the multi-year roll-out of its ToU initiative (or “Time of Day” as it’s referred to in Sacramento)—even as customers’ average bills have increased—customer perceptions of affordability have held strong.

More recently, however, as energy prices have started to climb nationwide, even SMUD, which has been a pioneer in sustainability has started to see customer perceptions of affordability decline. Between 2021 and 2022, the percentage of SMUD customers characterizing the utility’s pricing as “affordable” has declined from 35% to 28%.

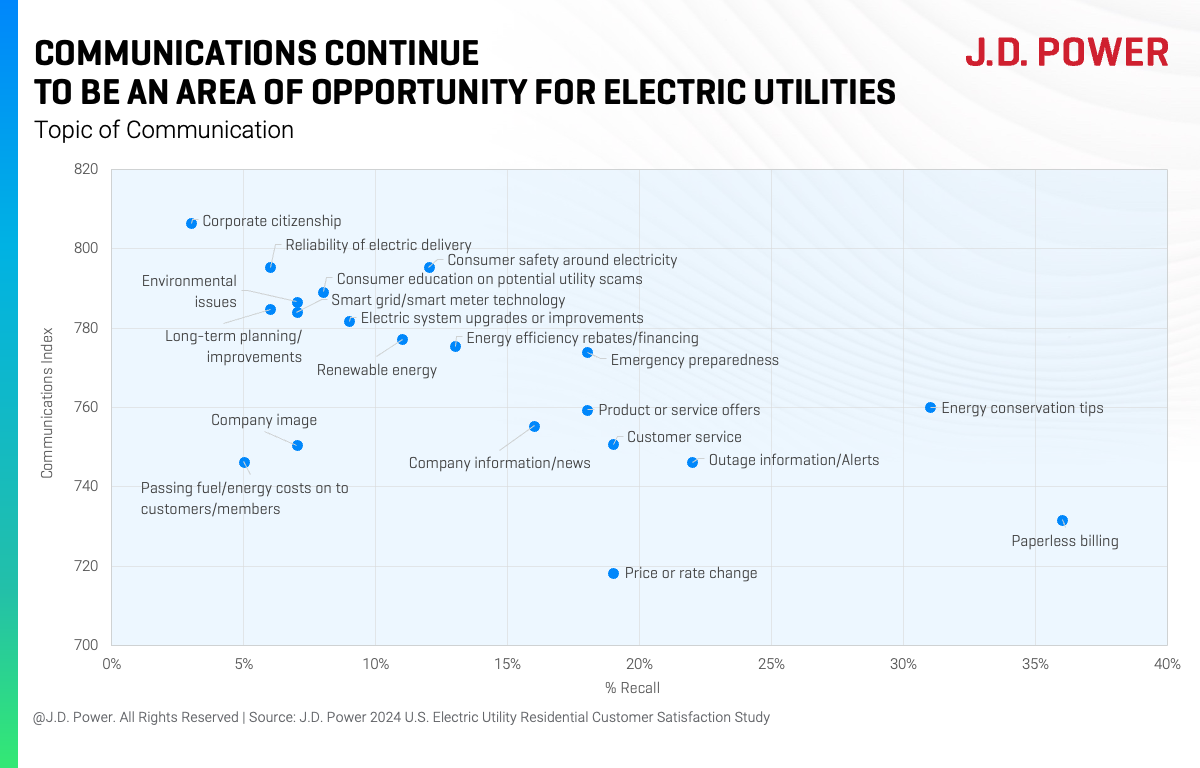

COMMUNICATION IS THE MISSING LINK

If energy conservation and transition to more sustainable alternatives are the goals for electric utilities, sky-high rates should be the catalyst to driving the consumer behavior changes needed to finally meet those goals. But that’s not happening today, and it’s largely a function of communication. Right now, even the best-performing utilities are not where they need to be in terms of customer engagement, awareness and support for sustainability initiatives. They need to get serious about customer communication to drive participation in these programs and, eventually, make a clear link in the customer’s eyes between sustainability and affordability.

MAKE IT EASY

Awareness is a big problem, but, even in cases where customers are aware of sustainability and energy conservation initiatives, they are often ignored. Far too often, products and services that are required to meet clean energy goals are designed to make things easy for the utility, not necessarily easy for the consumer. For example, many rebate programs can be difficult to find on utility websites and it is not always clear which appliances qualify or what information needs to be provided.

It’s no surprise that customers then struggle to understand the benefits of these programs, and how they can play a role in helping to use more clean energy and helping their electric utility meets its sustainability goals.

FIND OUT MORE

This Utilities Intelligence Report is based on data from the 2020, 2021 and 2022 editions of the JD Power 2022 Sustainability Index and the JD Power Special Report on the Impact of Time of Use Rates.

It was authored by Andrew Heath, managing director, utilities intelligence at JD Power. Please contact us at the numbers below to connect with Dr. Heath or to learn more about the underlying research.

Download a copy of the report here

MEDIA CONTACTS

Brian Jaklitsch – East Coast

631-584-2200

[email protected]

Geno Effler, JD Power – West Coast

714-621-6224

[email protected]

jdpower.com/business/utilities

JD Power does not guarantee the accuracy, adequacy, or completeness of any information contained in this publication and is not responsible for any errors or omissions or for the results obtained from use of such information. Advertising claims cannot be based on information published in this publication. Reproduction of any material contained in this publication, including photocopying in part or in whole, is prohibited without the express written permission of JD Power. Any material quoted from this publication must be attributed to JD Power.

© 2023 JD Power. All Rights Reserved.