Electric vehicles (EVs) powered the German new-car market’s return to growth in February. What part did purchase incentives play in this development? Autovista24 editor Tom Geggus examines the numbers.

Germany’s new-car market recorded 211,262 registrations in February, up by 3.8% year on year, according to the KBA. This was a comeback from January’s 6.6% decline, but meant the market still fell in the year to date. At 405,243 units, registrations dropped by 1.4%.

EVs, including battery-electric vehicles (BEVs) and plug-in hybrids (PHEVs), have held the market up so far this year. Both powertrains experienced year-on-year growth acceleration last month, as internal-combustion engine (ICE) models continued to decline.

Incentives powering EV market?

With a combined total of 70,603 registrations in February, 27.3% more EVs took to German roads than 12 months prior. Plug-ins captured 33.4% of the entire new-car market, an increase of 6.1 percentage points (pp) compared with February 2025.

BEVs led in terms of volume and growth, with deliveries increasing by 28.7% to 46,275 units. This meant 21.9% of all new cars hitting German roads last month were all-electric, up by 4.2pp. PHEVs claimed nearly half this share at 11.5%, up by 1.9pp from February 2025. Registrations of the technology climbed by 24.5% to 24,328 units.

In the year to date, EVs represented a third of the German new-car market at 33.3%. This signalled a 7.1pp upswing for plug-ins, as deliveries grew by 25.4% to 135,085 units.

Purchase incentive puzzle

New purchase incentives were introduced at the start of the year, with retroactive applications eligible back to 1 January. Taxable household income and family size determine the amount of funding available for BEV, PHEV and extended-range electric vehicle purchases. Users will be able to apply for support online; however, the portal will not open until May.

‘The February figures show that the passenger-car market is picking up again, and demand for BEVs is showing clear growth impulses, even though the subsidy has not yet taken effect,’ explained ZDK president Thomas Peckruhn.

‘Customers are still asking who will ultimately receive the premium, whether they will have to advance the money themselves, and what documentation is required. As long as these questions remain unanswered, the subsidy cannot unfold its signalling effect in the market,’ he added.

So, incentives could have helped boost recent EV growth. Some consumers would have been able to cover the upfront costs and make a claim later, encouraging uptake. Meanwhile, those more reliant on the scheme may continue to wait until May, at which point the full effect will start to become more apparent.

Stagnant hybrid market

EVs were not the only powertrains to record growth last month. Hybrids, including full and mild variants, recorded a 4.1% year-on-year increase in registrations. With 60,510 units delivered, the technology accounted for 28.6% of all deliveries in the country.

While this was 5.7pp ahead of the next most popular powertrain, it was stagnant compared with February 2025’s result. Alongside a single-digit increase in registrations, this reveals an ongoing struggle for hybrids.

Combined with a fall in January this year, the powertrain managed a 1.1% increase in the year to date. Its market share only increased slightly from 28.6% 12 months ago to 29.3%.

Together, EVs and hybrids recorded 131,113 deliveries, up 15.4% year on year. This pushed the market share to 62.1%, up from 55.9% 12 months ago. In the year to date, this equated to a 62.6% share with registrations up 12.8% to 253,801.

Skating on thin ICE

ICE deliveries dropped by 10.4% in February, as 79,742 units hit the road. This meant the combined market share for petrol and diesel fell by 6.1pp to 37.7%. While petrol led this decline, its volume was still ahead of diesel.

With registrations down by 14.9%, 48,404 new petrol-powered passenger cars hit German roads. The fuel type accounted for 22.9% of all deliveries, down 5.1pp year on year.

Diesel’s market share suffered a shorter fall of 2.4% to 31,338 units. However, this followed continued declines in popularity as it took a share of 14.8%, down 1pp.

Following a far worse January, its drop was more severe in the year to date. Registrations declined by 9.9% to 58,647 units as its share reached 14.5%, down from the 15.8% hold recorded 12 months earlier.

Petrol was in the same boat, as its year-to-date performance cast a darker shadow than its monthly decline. Deliveries plummeted by 22.8% to 92,099 units, with its share hitting 22.7%, down from 29% a year ago.

This gave ICE a 37.2% market share after the first two months of 2026. Representing a loss of 7.6pp, this share effectively transferred to EVs. In total, 150,746 petrol and diesel passenger cars hit the country’s roads, down by 18.2% year on year.

VW commands German market

Volkswagen continued to command a leading share of the German new-car market in February. While claiming a market share of 19% with 40,174 registrations, this equated to a year-on-year delivery decline of 2.1%.

Audi and SEAT also saw deliveries decline, down 2.3% and 11.1% respectively. However, some brands within the VW Group managed to record registration growth, including Skoda and Porsche, up 26.5% and 10%, respectively.

Elsewhere, BMW was able to take market share of 8.1% as its registrations remained level compared to February 2025, growing by 0.3%. Meanwhile, Mercedes-Benz saw a 9.9% drop in deliveries, putting it 0.1pp behind BMW.

Fiat and Opel had a far better month as their sales increased by 113.2% and 44.4% respectively. Hyundai also saw an increase, with deliveries up 16.2%, while Ford recorded a drop of 19.4%.

BYD enjoyed another month of comparatively high performance as its registrations grew by 1,550.3% year on year. With its 3,053 units, the brand was able to take the same market share as Mini at 1.4%. The BMW Group marque also saw an increase in deliveries, up 49.2%. Leapmotor also posted surging sales last month. Volumes were up 486.6% to 1,091 units.

Commercial fleets have access to more accurate data, stronger system integration, and advanced artificial intelligence (AI) applications. How exactly will this improve efficiency and enhance fleet decisions? Autovista24 journalist Tom Hooker investigates.

The face of global light-commercial vehicle (LCV) fleets is changing rapidly and becoming increasingly technological. Today, fleets have multiple data points, software systems and AI tools at their disposal.

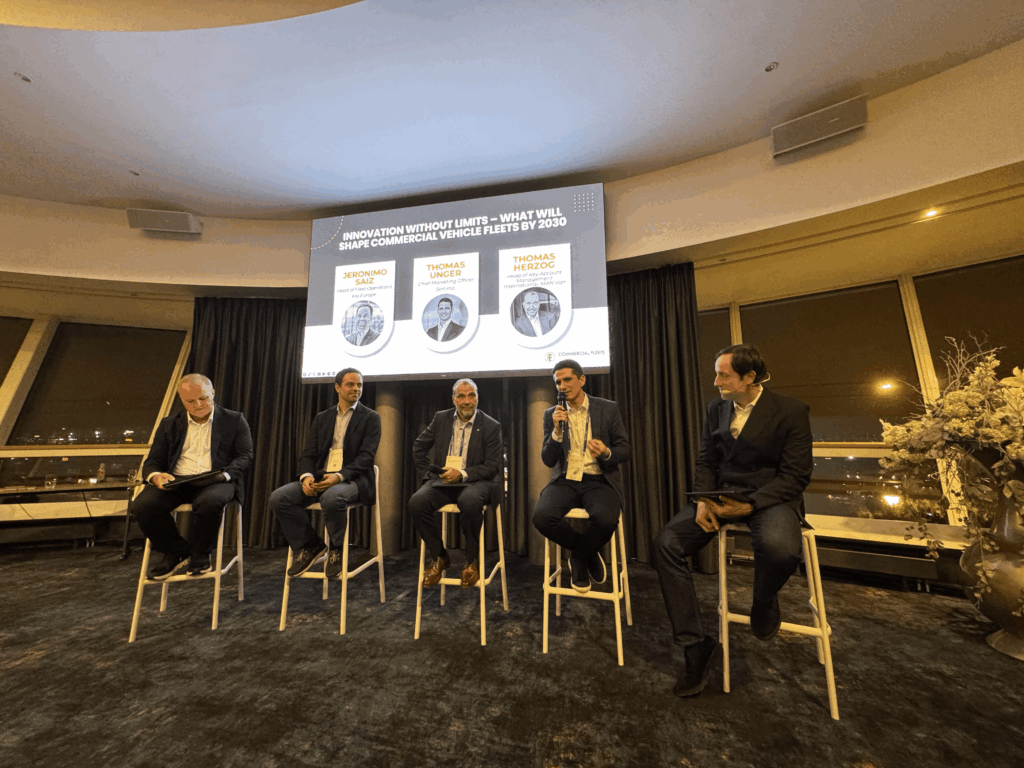

At this year’s Commercial Fleets Summit 2026, industry experts focused on the different ways these technologies can benefit businesses. This ranged from enabling predictive maintenance to AI-based driver coaching.

However, unless developments like these actually resolve key fleet concerns, they will remain inconsequential. So, can a more connected fleet really improve on important metrics such as return on investment (ROI), productivity and uptime?

Fleet productivity and the wider ecosystem

For some, the future of connected fleets is about much more than the vehicle itself. ‘Today is not about having the best van. It is about having the integration of the whole system,’ explained Jeronimo Saiz, head of fleet operations at Kia Europe.

‘You need to look at not only purchasing the van, but also having the telematics, a fantastic upfit and the best financing partner. It is a huge advantage. You are going to save money with energy consumption, route planning, how and where you service the vehicle, and how you forecast,’ he added.

From left to right: Ben Varey, commercial fleet expert at Nexus Communication. Jeronimo Saiz, head of fleet operations at Kia Europe. Thomas Herzog, head of key account management international, MAN Truck & Bus AG. Thomas Unger, chief marketing officer at Sortimo. Steven Schoefs, head of strategic relations at Nexus Communication

For this advantage to come to fruition, fleet connectivity across the whole ecosystem is vital. Telematics partners, maintenance partners, and the vehicle itself all need to work together. However, for many, that potential is yet to be realised.

‘Most of the large fleets are not yet fully connected. We are not getting the very best out of what we could. Connectivity, together with AI, should drive savings, more efficiency and better fleet management,’ projected Saiz.

Yet any advantages may not just appear in the balance sheet. With the help of AI, a more connected LCV fleet may present other material benefits.

‘When you talk about normal wear and tear, this is what I think could be the biggest advantage of AI, to reduce [unnecessary] stops,’ highlighted Thomas Herzog, head of key account management international, MAN Truck & Bus AG.

‘Yes, we make revenue in our workshops. But if we can reduce it and help to have the van only stop working once per year, then that is beneficial for all of us,’ he added. ‘What we are facing is the chance with AI to escape from routine work and daily routines to have more time and capacity to interact with customers.’

AI agents in fleets

Some of the most advanced fleets are using AI to help operations. However, the effectiveness of these agents is still reliant on data from the field.

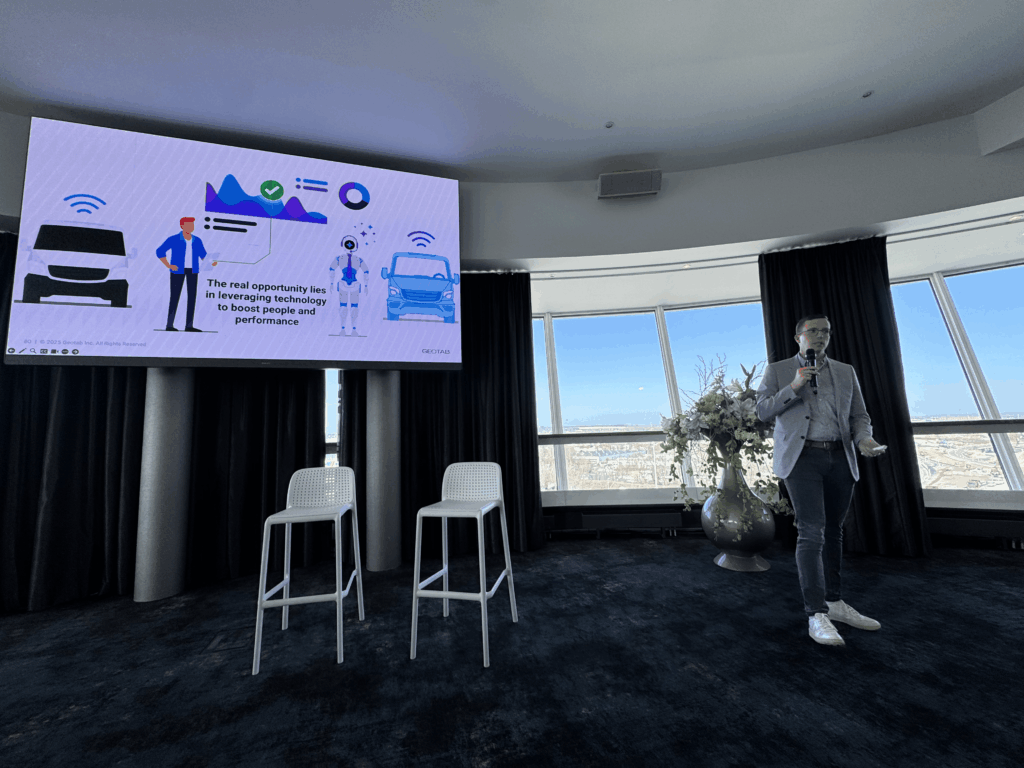

‘How do we see fleet management in the future? At the centre, there should be an AI agent that brings the data of various systems together,’ stated Fabian Seithel, associate vice president of sales and business development EMEA at Geotab.

Fabian Seithel, associate vice president of sales and business development EMEA at Geotab

‘Today, data is siloed far too much. That makes it very difficult for AI to act. A lot of it depends on input. So, the future should be an AI agent acting independently but supervised by a fleet manager who sets the tone for the agent,’ he commented.

A clear shift

This marks a clear shift away from using multiple telematic systems and towards more unified and automated operations.

‘Telematics started with track and trace a long time ago. Then it moved to data extraction: I want to know the fuel level [of a van in my fleet] or a fault code. But now, we are in the AI-powered phase,’ Seithel said.

These systems can observe, plan, act and evaluate. For fleets, this means they can identify a problem, decide what to do and trigger the next step.

Seithel cited maintenance as a clear example, outlining Geotab’s analysis of data from 5.8 million vehicles. The aim was to understand breakdown patterns and engine faults, providing an actionable risk model for fleets.

‘So, we quantify the risk of breakdown, such as 50%, then a fleet can use those predictions. Some fleets are more risk averse then others. For example, maybe in December, a delivery fleet takes the risk of a 50% breakdown to get as many parcels out as possible. We cannot drive the decision, but we can quantify the risk and explain it using contextual data,’ he explained.

Another use case presented was a video-based AI coach. Observing driver behaviour, the coach could give instructions in real-time. For example, it can suggest removing a distraction or taking a break.

Goldmine of fleet data

Some experts argued that a major issue commercial fleets face is getting concrete value from multiple data points.

‘Every fleet is sitting on a goldmine of data. The issue we have across the industry is getting the value out. That data is a challenge for us, because the industry keeps calling what we call faster clipboards,’ said Danielle Walsh, founder and CEO of Clearly.

‘Back in the day, we held a physical clipboard and wrote down what was wrong with our fleet and how it could be managed. We then moved to the electronic age, putting data into a spreadsheet or an electronic form,’ she said.

‘That moved into the connected age, with a lot of connectivity, and we created dashboards or spreadsheets in the cloud. Now, we are in the intelligence era, and we are stuck,’ Walsh stated.

She highlighted that on paper, a vehicle may appear to be in an acceptable condition. Yet, once maintenance, fuel, and finance data are combined, the story can change. Perhaps the vehicle needed servicing, not replacement, for example.

‘You can do three things when you connect your data. First, you can see what drives your cost. Is it across driver behaviour, the maintenance or the asset? Second, you know when to replace the asset, not when the lease says so. Instead, drive the decision by data. Third, make decisions on data, not policy,’ said Walsh.

Ultimately, better fleet data should not just confirm prior assumptions but inform what decisions are made.

Tactical fleet electrification

After fleet managers discover the recommended outcomes, the next step is to act. However, when it comes to electrification, there are barriers to overcome in building confidence in these decisions.

‘The fleets responsible for ordering the vehicles have environmental, social and governance (ESG) targets, net-zero targets, or regulations asking them to electrify faster,’ outlined Alfred Richard, co-founder and CEO of Nelson.

Alfred Richard, co-founder and CEO of Nelson

‘However, you have an operations manager slowing down the entire process because they are afraid of the productivity loss. How do you convince managers at the head office level and site level?’ he questioned.

The solution may be connected fleet software. With more transparency and openness, the gap between aspirational fleet managers and hesitant site teams could be bridged.

Before making decisions, Richard argued that fleets need to simulate real-world scenarios using a digital twin. Driver profiles, charging needs and route patterns all matter.

‘Simulation is a powerful thing. When you know what is happening, when you can control your current usage, you may anticipate what comes next. Thanks to all the existing data layers, you can build a digital twin of your fleet and simulate scenarios,’ he said.

This can also help avoid oversimplified fleet strategies. Richard warned that when talking about the transition to electric LCVs, there is no one-size-fits-all solution.

‘You can run scenarios on the digital twin and see what the priority is. The goal is to know your fleet’s EV suitability at a global scale, but also have information driver by driver. It is not about electrifying everyone. It is about electrifying the suitable drivers,’ he said.

Connected fleets are moving into a more active and autonomous phase. Fleet managers still want control, but less clutter. Accessing actionable insights coming from one unified source will be key. Those who can achieve this will have a distinct advantage over others.

In February, the battery-electric vehicle (BEV) share of the UK’s new-car market fell for the second consecutive month. Meanwhile, petrol saw a rare increase. But are there underlying factors playing a part in these performances? Autovista24 special content editor Phil Curry examines the figures.

Last month, the UK new-car market saw its best February performance since 2004. In total, 90,100 passenger cars were registered, a 7.2% year-on-year increase, data from the SMMT shows.

February is often considered one of the UK’s slower months, as buyers wait for the traditional plate-change period in March. But it was not all plain sailing.

Nearly every powertrain saw registrations increase in the month, except diesel-powered cars and BEVs. While the internal-combustion engine (ICE) has been sliding for a while, the all-electric drop raises concerns about the electrification push.

Demand across the market was driven by private registrations, which increased by 17.6% to 35,227 units. Fleet uptake improved by only 1.8%, although it held the largest overall volume of 53,506 units.

BEV struggle continues

The UK’s BEV market appears to be struggling. In February, 21,840 all-electric models left showrooms, a rise of 2.8% compared to the same period last year.

The technology took a 24.2% market share, dropping by 1.1 percentage points (pp) as other fuel types outpaced the powertrain. It was the second consecutive decline in market share, at a time when mandated requirements are rising.

However, it is too early to suggest that the market is going to struggle in 2026. Results in the first quarter of last year were influenced by the addition of vehicle excise duty (VED) from 1 April 2025. This makes for an uneven comparison, as many drivers likely pulled forward their purchasing plans to avoid the additional fees.

There was also likely some push from carmakers to get models out. There will have been pressure to boost end-of-year figures and meet the UK’s zero-emission vehicle (ZEV) mandate requirements.

February’s result means that across the first two months of 2026, 51,494 BEVs were delivered to customers, a 1.2% increase. However, the 22% market share was down by 0.8pp.

For 2026, the ZEV mandate requires a fleet-sales target of 33%. This was already an ambitious requirement, given the country’s overall BEV sector failed to reach the 2025 28% requirement.

Regulatory BEV impact

Currently, the UK government is pushing hard for BEV uptake. Its Electric Car Grant incentive scheme provides discounts on certain all-electric models. A new advertising campaign, championing the benefits of BEV driving, is also running across the country.

At the end of February, a charging point grant boost was announced by the government. This provided installation support to renters, flat owners, those without off-street parking and businesses. Up to £500 (€576) can be saved when buying a domestic charger, with the plans running until March 2027.

This comes at a time when the cost of public charging, especially on rapid and ultra-rapid chargers, is increasing. According to data from the RAC, ultra-rapid chargers increased from an average of 78.06p per kW in January 2025 to 83.20p per KW in January 2026. Prices for rapid chargers rose from 79.75p per kW to 82.10p in the same period.

BEVs have also been impacted by government regulatory changes. Alongside the VED implementation in April, there was the announcement of a ‘pay-per-mile’ scheme, known as eVED. Set to start in 2028, this news has done little to champion the technology’s affordability.

‘With year-to-date BEV market share at 22%, two-thirds of the 33% share mandated for 2026, March is set to be a pivotal month. Manufacturers have already invested billions in new models and discounts to drive demand, now with support from government’s Electric Car Grant, but circumstances have changed beyond expectation since the regulation was set,’ the SMMT outlined.

‘A holistic review of the transition is needed, and must be completed urgently as buyer confidence is anticipated to be weakened further amid plans to introduce eVED from 2028,’ it continued.

Petrol powers forward

For the first time since September 2025, registrations of new petrol cars enjoyed a year-on-year improvement. In February, 41,935 units were delivered, a rise of 5.2%. However, given the month’s low volumes, this equated to an increase of just 2,070 models.

This meant the fuel type took a market share of 46.5%, down by 0.9pp compared to February 2025. This was a marginally lower drop than seen by BEVs.

The strong month means that across January and February, petrol registrations increased by 0.7% to 110,692 units. This was enough for a 47.3% share of the entire market, down 2.1pp.

The UK reports petrol powertrain figures differently from other major markets and the European industry body ACEA. It merges mild-hybrid (MHEV) volumes with their equivalent ICE counterparts. This can skew the results, with the market appearing to perform much better than other countries.

In January this year, SMMT recorded 68,757 new petrol car sales, including MHEVs. Compared with ACEA’s pure petrol ICE total of 37,109 units, MHEVs made up 46% of the SMMT’s figures. Back in January 2025, this share was only 33.5%, the lowest percentage of that year.

It does appear that the UK’s petrol market is reliant on MHEVs to prevent numbers dropping further. Yet it is still performing well compared to other markets. This is once again cause for concern, with the 2030 ban just four years away.

PHEVs perform best

The standout performance in February came from the plug-in hybrid (PHEV) market. With 10,438 deliveries, volumes rose by 43.5% compared to the second month of 2025. This was the 13th consecutive month of double-digit improvement, and the second to see improvement over 40%.

This is a level of consistency that no other powertrain in the UK has matched during the same time. These results have allowed PHEVs to close on the full-hybrid (HEV) market in the UK.

In February 2025, the gap between the two was 4,158 units. Last month, this was 1,369 units. However, it has been closer at times, as the powertrains compete. With its impressive volume jump, PHEVs took an 11.6% market share, up 2.9pp year on year.

Across 2026 so far, the technology has seen a rise of 45.9%, with 28,995 units delivered. It is the only powertrain in the year-to-date chart to see a double-digit increase. Meanwhile, its 12.4% share jumped by 3.5pp.

HEVs also saw growth. Registrations rose by 3.3%, with 11,807 deliveries made in the month. This equated to a 13.1% market share, down by 0.5pp. Between January and February, 31,104 HEVs left showrooms, a 4.2% increase. The technology’s market share remained stable, dipping 0.1pp.

Diesel drags down ICE

ICE registrations, bringing together petrol, diesel, and their respective MHEV powertrains, increased by 4.3% in February. This allowed the technology to take a 51.1% market share, a drop of 1.4pp. This was not helped by diesel’s decline in the month, as the powertrain posted a 3.8% drop, with 4,080 registrations.

Meanwhile, electric vehicles (EVs), made up of BEVs and PHEVs, experienced a 13.2% improvement, driven by plug-in hybrids. Their share of 35.8% was up 1.9pp. However, it was also 15.3pp away from ICE.

Towards the end of 2025, EVs had overtaken ICE deliveries, pulling ahead by 0.2pp in December. With BEV deliveries recently stagnating, lower PHEV volumes, and an apparent resurgence for petrol, EVs have a lot of work to do to catch up again.

The same can be said for the electrified market. Adding HEVs to the EV mix, deliveries were up 10.4% in the month, with a share of 48.9%. This is the second month in a row that electrified volumes have fallen below ICE. The grouping beat the traditional powertrain grouping between September and December 2025.

In the first two months of 2026, EV registrations were up 13.8% with a 34.4% market share. Electrified deliveries increased by 10.9%, with a 47.6% hold of the overall total. However, ICE deliveries continue to lead, with a 52.4% share, despite a 0.1% decrease in volumes.

What can be expected from the much-anticipated Industrial Accelerator Act (IAA)? Plus, an exclusive report from the Commercial Fleets Summit. Tom Geggus, Autovista24 editor, presents the Automotive Update podcast.

This episode takes a look at the recently unveiled IAA and what it could mean for the European automotive industry. Also, Autovista24 journalist Tom Hooker dials in from the Commercial Fleets Summit, hosted in Brussels.

The European Commission has proposed the long-anticipated Industrial Accelerator Act. Central to the legislation is the enhancement of localised EU industrial competitiveness and promotion of low-carbon production methods.

The IAA aims to increase local value creation and strengthen the region’s industrial base. This comes amid perceived unfair global competition and dependencies on non-EU suppliers. The act will look to boost manufacturing’s share of EU GDP to 20% by 2035. However, the IAA also outlines that the EU should remain open to outside investment.

A Q&A published by the European Commission highlighted that low-carbon requirements will be created for steel and aluminium used by the automotive industry. ‘Made in the EU’ standards will also apply to aluminium. Provisions will also apply to electric vehicles and their components.

The proposal builds on previous EU legislation, further streamlining the deployment of clean technologies across numerous European industries. For the automotive sector, the proposal follows last year’s Automotive Package announcement.

The IAA will be negotiated by the European Parliament, and the Council of the European Union, before its adoption.

Commercial Fleets Summit reveals

The Commercial Fleets Summit is a two-day international event held in Brussels. It focuses on a wide range of key issues and trends impacting the global commercial vehicle sector.

Several key themes have already emerged at this year’s event, centred specifically on light-commercial vehicles. These included environmental regulation, fleet electrification, plus the incorporation of connected vehicles and use of artificial intelligence (AI). In terms of electrification, discussions centred on issues surrounding charging infrastructure efficiency.

‘There is less talk about if fleets are going to electrify. Instead, it is more about how fast, and how they are actually going to achieve that,’ stated Autovista24 journalist Tom Hooker, from the event.

‘Charging infrastructure is being seen as both a bottleneck and an opportunity. You then obviously have the interaction with the electricity grid, and this is certainly emerging as a new consideration,’ he added.

The event also touched upon the future for commercial fleets. Looking ahead, these could be further integrated with digital ecosystems, with brand loyalty becoming less of a factor. Instead, digital-led frameworks could become increasingly important when selecting vehicle type and brand. Additionally, technology and AI will play an increasingly crucial role.

‘I think one of the first AI use cases will be helping fleet operators to manage and reduce fuel costs,’ Hooker said. ‘This, in turn, is having a high return on investments in some other areas. One thing I think I will hear more about later, is route optimisation and energy efficiency gains.’

February provided plenty of positives for Spain’s new-car market. But as the nation’s market continues to grow, is electrification progressing as planned? Autovista24 web editor James Roberts examines the latest numbers.

February saw a second consecutive month of growth for the buoyant Spanish new-car market. In total, 97,082 new vehicles took to the country’s roads, 6,755 more than 12 months prior. This ensured a 7.5% year-on-year increase, according to the latest ANFAC data.

With only December 2025 blotting an unbroken streak of year-on-year gains for Spain’s new-car market, February resumed a familiar trend. Industry body ANFAC highlighted that all channels achieved growth in the month, particularly the rental sector, which saw a 22.6% uptick.

‘After a hesitant start in January, February is once again a positive month for vehicle sales,’ stated Félix García, director of communication and marketing at ANFAC.‘Last month, the rental car channel was the one that grew the most, accounting for almost one in five sales of passenger cars. It is a logical increase to renew the fleet for the Easter period. Without these sales, the growth of individuals and companies is flatter compared to February 2025.’

This ‘good pace,’ as highlighted by ANFAC, prevailed when assessing the first two months of 2026. Combined January and February totals amounted to 170,185 passenger cars. This ensured a unit upswing of 7,542 compared with the same period in 2025, a healthy 4.6% boost.

Hybrids remain top new-car choice

Hybrids, made up of both full and mild hybrid powertrains, remained the top seller in February. In total, 46,592 new hybrids joined Spain’s car parc in the month, according to ANFAC.

This robust total returned a 17.1% year-on-year increase and a 48% market share. This was just 0.6 percentage points (pp) down on January’s record, suggesting hybrid popularity is not ebbing. It was even up by 3.9pp year on year.

Spanning the opening two months of 2026, hybrid cars held a dominant 48.3% market share, up 3.7pp year on year. Across January and February, 82,189 new hybrids made their way to customers in Spain.

Spain’s BEV market share issue

Amid this preference for hybrids, ANFAC highlighted that EVs, including battery-electric vehicles (BEVs) and plug-in hybrid vehicles (PHEVs), continue to be a ‘key segment.’ However, is this consistently strong sector in danger of stagnating, especially when it comes to BEV uptake?

February saw 8,889 new BEVs take to Spain’s roads. This equated to a 45.4% volume increase, carving out a 9.2% market share, up 2.4pp.

After two months of the year, the BEV market share stood at 9%, 2.2pp up year on year. This comes as volumes reached 15,361 units, establishing a 38.1% year-on-year upswing.

One reason for new-BEV buying reticence could be uncertainty. Spain’s relatively successful trend of EV adoption had been enabled by a long-standing incentive framework, the MOVES plan. This was introduced in 2019, funded by the EU’s NextGenerationEU recovery funds, and managed in conjunction with Spain’s regional governments.

The issue with incentives

The last iteration, MOVES III, came to an end on 31 December 2025. Its replacement, the Auto 2030 Plan (Auto+), announced at the beginning of December, aims to centralise and simplify EV incentives.

It will mobilise up to €400 million in public and private investment between 2026 and 2030 to increase electrification in Spain. It will offer varying discounts on BEVs and PHEVs, spanning direct purchases, leasing and renting arrangements.

The subsidies will be applied retroactively to vehicles purchased since 1 January in Spain. However, the government website has not yet confirmed publication. According to Carwow, Full implementation of the Auto 2030 Plan is not expected until at least May this year.

In late January, the Ministry of Economy, Trade and Business proposed amendments to the Auto 2030 Plan, according to La Tribuna. Addressing industry concerns, the change reportedly re-centres the scheme around cars manufactured within the EU. This would make the plan more closely aligned with the system used in France, as reported by electrive.

One result of the amendments could be the discouragement of some models made in China from eligibility. This could bring additional uncertainty into the market. An added complication relates to Chinese carmakers investing in Spanish manufacturing, such as Chery and BYD.

Spain’s need for clarity

‘Although the Auto+ plan has already been announced, and there are brands that have committed to bringing forward the discounts, there is no doubt that the official publication of clear and agile regulatory bases is essential to increase confidence,’ stated Tania Puche, GANVAM’s director of communication.

Raúl Morales, communications director of FACONAUTO, added: ‘For another month, electrification has driven the market, once again exceeding 20% market share in new registrations. This is partly due to the announcement of the retroactive application of the Auto+ Plan, which provides aid to electric vehicles.

‘What we need now is for the regulatory framework for this plan to be published as soon as possible, so that buyers continue to have certainty and electrification can continue to increase its registration numbers,’ he continued.

Whatever the outcome, industry bodies are urging further clarity around electrification uptake measures to boost sales in the country.

‘It is urgent to reactivate the tax deduction in personal income tax for the purchase of electric vehicles and the bonus for the installation of charging points, measures that have been overturned in congress for the second time in two months,’ Puche stated.

PHEVs still proving popular

As BEV uptake looks to push through to new heights, PHEV popularity has helped lift Spain’s overall plug-in sector.

Since a notable triple-digit percentage volume surge in May 2025, the powertrain has continued to sell well. In February, 12,092 new PHEVs left forecourts in Spain, equating to a 75.2% year-on-year increase.

Across the first two months of this year, PHEVs have seen 20,832 registrations and a 71.6% volume lift. This has ensured a 12.2% market share, up 4.7pp year on year. This strong start to 2026 and the enduring appeal of the powertrain have boosted overall plug-in deliveries.

Spanning January and February, combined BEV and PHEV registrations reached 36,193 units. This marked a significant year-on-year climb of 55.6%. This also brought some meaningful market share capture, with the powertrains accounting for 21.3% of overall registrations, up 7.2pp.

The combination of electrified registrations, including hybrids, BEVs and PHEVs, took the dominant slice of the Spanish new-car market. Across the opening two months of 2026, a total of 118,382 new electrified vehicles were registered in the country. This 23.7% upswing ensured a market share of 69.6%, a new high, and a 10.7pp increase.

Petrol remains a key player

With many headlines surrounding EV volume growth, it is easy to ignore the prevailing appeal of petrol within Spain.

At first glance, sales have taken a year-on-year nosedive. Fewer new petrol-powered options are available as the industry moves towards net-zero. However, when it comes to market share, the fuel type is clinging on in Spain.

In February, 22,534 new petrol vehicles reached customers, a 19.5% year-on-year dip. Although this continued the trend of double-digit monthly declines, the reality is more nuanced.

Combining January and February’s new-car registration totals, petrol accounted for 23% of the market, with 39,067 registrations. Although volumes were down 20.8% year on year, the fuel type commanded the second-highest market share after hybrids. Petrol was 14pp higher than BEVs, and 10.8pp above PHEVs.

While petrol retained influence in Spain’s new-car market, diesel continued its descent. The fuel type saw just 7,226 new vehicles registered across January and February. This underlined a significant 28.6% year-on-year drop and a meagre 4.2% market share, down 2pp.

Total internal-combustion engine (ICE) new-vehicle registrations, including petrol and diesel, totalled 46,293 in January and February. This provided a 27.2% market share, down 9.3pp year on year, but still 5.9pp above EVs. One of the big questions now is whether plug-in sales will overtake ICE volumes in Spain this year.

Event Webinar

Webinar. Europe’s Auto Forecast 2026: Technology, Policy, and EV Adoption

This webinar delivers a clear market forecast for Europe, grounded in authoritative vehicle data, while also explaining emerging trends and how EV adoption trajectories differ across regions.

Europe’s automotive market is being shaped by structural shifts, and the outlook for 2026 is becoming increasingly complex. In this session, our experts examined the key forces shaping the sector, including how electrification, incentives, and new technologies are influencing demand and forecasts.

Accelerating or Stalling? Europe’s 2026 Auto Market and Powertrain Shifts

Emissions regulations, incentive structures, charging infrastructure, and model availability are pulling European automotive markets in different directions.

Meanwhile, the “EU Automotive Package” is reshaping compliance costs, OEM behaviour, and registration expectations.

This session brings together automotive intelligence, vehicle market research, and electric vehicle market forecasting to uncover what is happening beneath the surface and what will define the next 12–24 months.

We discussed what trends are changing the pace of market growth, including:

BEV growth is now expected to slow as hybrid, PHEV, and ICE sales extend beyond 2035.

UK ZEV targets face growing pressure, as rising oil and gas prices add inflationary strain to the wider market.

EV adoption is powered by clear policy and strong incentives, as well as hidden drivers such as culture and history, environmental awareness plus natural resources.

New technological developments, such as faster charging and improved driving range, are boosting EV adoption.

Webinar recap: what you missed

The full webinar recap is now available. Watch the recording below.

Turning EV Trends into Strategic Advantage

Knowing how adoption, policy, and technology are shaping the EV market allows you to act proactively and stay ahead of the curve.

Forecast adoption curves - As hybrid, PHEV, and ICE sales extend past 2035, use EV Volumes to plan for slower BEV growth and adjust production and inventory strategies accordingly.

Monitor regulatory and market pressures – With EV Volumes, you can benchmark scenarios to stress-test your forecasts and plan for policy-driven risks.

Stay ahead of policy and technology trends – Monitor and track signals with EV Volumes to identify which markets and segments will gain traction first.

With BEV growth slowing, diverging adoption rates across Europe, new technologies and brands entering the market, staying ahead requires more than intuition.

Get the right market intelligence to benchmark trends, anticipate regional differences, and plan strategies that align with how Europe’s EV transition is unfolding.

Ready to power what’s next?

Whether you’re launching a new model, optimizing your dealer network, or rethinking lending and insurance, we’ll help you turn customer truth into performance.

The new-car market in France endured a slow start to 2026, as February saw a dramatic drop in registrations. But which powertrains caused the market to sink, and could this trend continue? Autovista24 special content editor Phil Curry examines the data.

In total, 120,764 new passenger cars were registered in February, figures reported by the PFA and AAA Data show. This was a drop of 14.7% compared to the same period in 2025.

This was the steepest slide in volumes since the 24.3% decline recorded in August 2024. It is also the fourth consecutive month of registration decreases. February’s result means that after just two months of 2026, deliveries were down 11.1% in the year to date.

Are BEVs running out of momentum?

Volumes of electric vehicles (EVs), incorporating plug-in hybrids (PHEVs) and battery-electric vehicles (BEVs), kept the French market from sinking further. However, natural market demand for these powertrains was obscured by the country’s incentive and social leasing programmes.

EV orders using the social leasing scheme began on 30 September 2025. Meanwhile, the country’s ecological bonus incentive scheme was restructured in July 2025, with a change in funding provision.

Both schemes had an impact on a struggling BEV market. It recorded double-digit growth since July, after wavering in its consistency beforehand.

With the launch of social leasing in October, BEV volumes have increased, after a rollercoaster period of results. In that month, deliveries rose by over 60%, following increases exceeding 40% in both November and December. This year started with an improvement of over 50%.

However, there were signs that the incentive momentum may be slowing. In February, 32,372 new BEVs were registered, according to Autovista24 analysis of PFA and ACEA data. This was a 27.8% increase year on year, the smallest volume improvement since September 2025.

The all-electric powertrain took a 26.8% market share in February, a jump of 8.9 percentage points (pp). Despite the lower growth, momentum remains with the technology in the French new-car market. After two months, BEVs have established themselves as the country’s second-best-selling powertrain, after hybrids.

So far in 2026, a total of 62,679 all-electric models have been delivered to customers, up 38.5% year on year. This means the powertrain accounted for 27.5% of all registrations in the country, up 9.8pp.

PHEVs see growth in France

While BEVs flew, PHEVs also helped the French new-car market from sinking further. In February, 6,655 new plug-in hybrids made their way to the country’s roads, a 3.2% rise.

The result gave PHEVs a 5.5% market share, up 0.9pp compared to the same month last year. This was also the first time since December 2024 that the powertrain recorded an improvement in volumes. Yet rather than an increased interest, the result may have more to do with last year’s poor performance.

In February 2025, PHEV volumes were down 45%, as the market struggled. Double-digit declines were recorded across the first half of 2025 and during the final quarter of the year.

This appears to have reset the plug-in hybrid market. January 2026 saw a stable result, with volumes down only 0.6% year on year. February’s figures may give hope that PHEVs can help reduce overall losses seen elsewhere.

Across the first two months of the year, France’s PHEV market was up by 1.5%, with 11,476 units delivered. This equated to a 5% share, up 0.6pp.

Combining BEV and PHEV figures, France’s EV market rose by 22.8% in February, with 39,027 deliveries, according to Autovista24 calculations. The 32.3% share was up 9.8pp, and almost doubled that achieved by internal-combustion engine (ICE) models. After two months, EV deliveries were up 31.1%, with a 10.4pp increase in market share to 32.5%.

Petrol providing headache for France

The incentive-aided improvement in the EV market was not enough to make up for the shortfall in ICE registrations, which are pulling the French market down. For the second month in a row, deliveries of petrol-powered passenger cars fell by nearly half year on year. February saw registrations collapse by 48.1%.

February’s petrol result meant the powertrain represented 15.1% of total deliveries in the month. This was a drop of 9.7pp compared to the same month in 2025. Between January and February, petrol deliveries were down 48.5%. This left the fuel type with a market share of 14.7%, down by 10.7pp.

Diesel fared no better with registrations down 53.8%, although with lower volumes, as 3,098 units were delivered in the month. With a 2.6% market share, the powertrain is floundering below other major technologies.

Just 5,619 units were registered in the first two months of the year, a 51.8% decline. This gave diesel a 2.5% market share, dropping 2.1pp compared to the first two months of 2025.

Combining petrol and diesel deliveries highlights the issues that France is facing in its new-car market. With 21,304 registrations, volumes dropped 49.1% during February. That figure gave the grouping a 17.6% market share, falling 11.9pp.

After two months of 2025, ICE volumes declined 49%, with 39,151 units leaving dealer forecourts. The 17.2% share of total registrations was down 12.8pp.

Hybrid slowdown in France

While petrol and diesel declines had a debilitating effect on the French new-car market, hybrids also struggled. In February, 56,538 new hybrids were registered, including full and mild versions, according to Autovista24 analysis of PFA data. This was a drop of 9% year on year. The market appears to have slowed, following rapid rises seen across 2025.

February’s result was the first decline in the market for quite some time. This suggests that the market may have peaked. Yet it still dominated French registration figures, with a 46.8% market share in the month. This was up, but only by 2.9pp, as results elsewhere declined.

Two months into 2026, hybrids recorded 108,061 registrations, according to PFA data. This was a drop of 4.9%, compared to the same period in 2025. Yet their market share of 47.4% was up 3.1pp, and considerably higher than any other powertrain.

ICE powertrains are acting like a weight, pulling the overall performance of the French new-car market down. Without the powertrain, the market would still have declined, but by a marginal 0.3% in February, according to Autovista24 analysis.

Residual values (RVs), presented as a percentage of retained new-car list price (%RV), kept sliding in Europe during February. But is this descent slowing, and what comes next? Autovista24 editor Tom Geggus unpacks the data with regional experts.

The average retained value of a 36-month-old car at 60,000km dipped again across many European used-car markets. In February, Austria, Germany and Switzerland saw new lows compared with the last 12 months.

Meanwhile, France and Spain saw lower value retention rates in January. At the start of 2026, Italy and the UK saw %RVs above rates recorded in December and August 2025, respectively.

Both France and Spain saw a marginal month-on-month %RV improvement. Meanwhile, Austria, Germany, Italy, Switzerland and the UK recorded declines compared with January 2026.

The downward trend is much more visible when comparing February 2026 with February 2025. All markets saw %RVs decline, with Italy performing the worst. Values dropped to 45.5%, down by 4.1 percentage points (pp) in the country.

While this appears drastic, trade values are still undergoing a process of normalisation following inflation during the COVID-19 pandemic. Compared with 2021, all markets continue to see higher levels of value retention.

Switzerland was the closest to its position five years ago, with values only 1.1pp higher. Three-year-old used cars in Germany continue to see higher levels, 4.5pp above where they were in 2021.

%RVs are expected to keep falling across these markets in the next three years. Italy is the only exception, which is forecast to see a marginal increase by the end of 2028. By the same point, France and the UK are expected to see the largest %RV declines of the seven markets.

Austria’s subdued market

Austria’s sales‑volume index (SVI) for two‑to‑four‑year‑old passenger cars recovered significantly in February. After a traditionally weak January, the SVI increased by 52.9% month on month. However, the SVI remained down compared to February 2025, with the index dropping 7.6% year on year.

The active‑market volume index (AMVI) also witnessed a slight bounce back. It rose by 1.4% month on month, while stock levels were 4% higher year on year. This indicates a well‑supplied market and a modest build‑up compared to 2025.

‘Turnover slowed again in February,’ stated Robert Madas, regional head of valuations. ‘The average time needed to sell a used car increased to 76.7 days. This marks a three‑day deterioration compared with January and a year-on-year increase of 1.5 days. This underlined subdued retail activity, despite improved sales volumes.’

Diesel models took the lead in turnover speed, taking an average of 71.5 days to sell. This was followed by petrol cars taking an average of 74.4 days to sell. Then came full hybrids (HEVs) at 78.3 and plug-in hybrids (PHEVs) at 87.9 days. Battery-electric vehicles (BEVs) continued to take the longest time to sell at 88.7 days.

RVs soften in February

Looking at pricing, the average RV of a 36‑month‑old car at 60,000km softened in February. The average trade RV reached €22,623, down 0.6% month on month.

%RVs in Austria declined to 47.1%, down 0.7 percentage points (pp) compared to January. Year on year, %RVs decreased by 1.4pp, reflecting continued downward pressure on used‑car values amid rising supply and normalising demand. List prices remained high, averaging €47,987 in February, a slight 0.8% increase month on month.

HEVs retained the highest trade value at 50.2%, followed by petrol cars at 49.3%. Then came diesel models with 48% and PHEVs with 43.9%. BEVs held the lowest %RV once again, at 38.8%. However, this was a slight improvement of 0.2pp month on month.

‘Looking ahead, %RVs are expected to decline slightly in the next few years,’ said Madas. ‘In December 2026, a 0.6% year-on-year decline is forecast. A 0.7% decrease in 2027 is expected to follow.

‘This points to a slow but persistent downward %RV trend in the coming years. This is consistent with a rebalancing market environment and ongoing supply normalisation,’ he highlighted.

France sees stability

RVs continued to be stable in France during February. Some powertrains saw slight month-on-month increases, although this was mainly due to a value drop in January. However, February’s results were stable compared with December 2025.

Petrol saw %RVs after 36 months and 60,000km increase compared with January. Yet they fell compared with December. Recent %RV declines for petrol have been minor as the fuel type holds its value better than other powertrains.

‘Many manufacturers offer petrol variants while diesel has become rarer,’ commented Ludovic Percier, senior RV analyst for France. ‘However, diesel has seen less impact, even managing to record %RV increases compared with January.’

HEVs saw stability in February, but their %RVs were below December’s results. This continues a declining value retention trend seen in recent months. This can be attributed to the increasing number of HEVs offered in France, most of which are from mainstream brands.

These models do hold value as well as Toyota’s HEVs. Three of the top five fastest-selling HEVs came from the Japanese brand. Used HEVs are in demand, but carmakers cannot risk adding big price premiums at the expense of RVs.

Supporting EV RVs

Used BEVs and PHEVs took the longest time to sell in France. However, RVs can be supported by newer models with increased ranges. While %RVs increased month on month for both powertrains, they fell compared with December.

PHEV demand and supply remain imbalanced. In previous years, many of these vehicles were sold to fleets on the back of fiscal advantages. They came with excessive new-car market list prices, explaining the lower RVs. Models offering an electric-only range of below 60km have been the most affected.

Higher-priced BEVs with longer driving range have seen larger absolute RVs and more stable %RVs. Lower segments with lower list prices and smaller ranges have been impacted by the environmental bonus and social leasing scheme.

‘Meanwhile, upper segments have not yet been impacted by fiscal fleet advantages,’ Percier added. ‘Those vehicles will come to the used-car market in early 2028.’

BEVs spent 85.5 days in stock on average, compared with the market average of 67.2, which is also high. The Tesla Model 3 was still the quickest to sell, while the Model Y was the third-fastest-selling used BEV. They remain in demand as their new prices drop once again.

Demand rebounds in Germany

Used‑car demand in Germany rebounded significantly in February after the seasonal downturn seen at the start of the year. The SVI jumped to 143, representing a 43% month‑on‑month increase. Despite this strong recovery, the SVI was down 13.7% year-on-year, as demand remained below last year’s level.

Supply conditions also improved. The AMVI rose slightly by 1.1% from January. Year on year, stock availability was 22.6% higher, confirming a continued and substantial rebuild of used‑car supply.

‘The average number of days needed to sell a used car increased to 68.3 days. This was a noticeable deterioration of 3.3 days month on month and year on year,’ highlighted Madas.

Looking at powertrain performance, BEVs were the fastest-selling technology, taking 61.6 days to leave forecourts. Then came PHEVs at 62.4 days. HEVs followed at 63.2 days, while diesel-powered vehicles took 69.9 days to sell. Petrol-powered cars sold the slowest, at 70.9 days.

Renewed pressure on RVs

RVs came under renewed pressure in February. The average %RV of 36‑month‑old cars at 60,000km declined slightly to 46.8%. This was down 0.1pp month on month and 0.9pp year on year.

In contrast, absolute trade values increased slightly to €21,855, a 1% improvement from January. This was supported by the continued rise in list prices, which climbed to €46,664. This was up 1.1% compared to January and up 4.2% year on year.

By powertrain, petrol-powered cars continued to lead with a %RV of 48.3%, followed closely by diesel at 48.2% and HEVs at 47.5%. PHEVs held on to 44.1% of their value, while BEVs remained the lowest at 37.1%, maintaining the gap observed throughout 2025.

Looking ahead, RVs are expected to remain under pressure, in line with previous forecasts. By the end of 2026, %RVs are projected to decline by 1.4% compared with December 2025.

‘Pressure is predicted to ease somewhat in 2027, with a smaller decline of 0.9% expected. This indicates ongoing RV strain, driven by recovering supply, normalising demand, and elevated list prices,’ Madas outlined.

Values fall in Italy

‘As expected, RVs continued to decline in Italy during February, in line with the trend observed in 2025,’ said Marco Pasquetti, cluster head of forecasting for Spain and Italy.

%RVs after 36 months and 60,000km stood at 45.5%. This corresponds to a decrease of 0.7pp compared to January and a drop of 4.1pp year on year. There are no signs of this trend reversing, with the downward trajectory likely to persist throughout 2026. By December, %RVs can be expected to decline by 6.2% overall.

There were no surprises across the various powertrains. All of them saw proportionally consistent declines in line with the overall market trend. Diesel, although declining, remained the technology with the best retention of list price value at 50.1%.

In terms of volume, it also continues to be in high demand on the used‑car market. This is likely due to signals from some manufacturers that they are considering reinvesting in these engines, including Stellantis.

The average time required to sell a used vehicle on major online marketplaces improved compared to January 2026 and February 2025. In particular, the year-on-year improvement is notably positive for BEV and PHEV vehicles. If this trend continues, it could indicate a slowdown in the decline of RVs for these powertrains.

Bad start for Spain’s used-car market

New-car sales in Spain began 2026 with a slight increase of 1% compared to January 2025. Electric vehicles (EVs), including BEVs and PHEVs, showed strong momentum.

Sales of these powertrains increased by nearly 50% as they represented over a fifth of the new-car market. By channel, private buyers and companies recorded significant declines. Only rental companies saw their registrations increase, up by 63.5%.

These rent-a-car renewals have returned a significant volume of young used vehicles to the market. This made it the only channel to record positive results compared with January 2025.

‘Overall, the start of the year has not been good for used-car sales, which fell by 9%,’ noted Ana Azofra, head of valuations and insights for Spain.

‘BEVs and PHEVs continue to gain share, benefitting from growing demand for electrified alternatives,’ she added. ‘This increased interest is reflected in the evolution of average transaction prices, with increases across all electrified powertrains.’

Average absolute RVs of 36-month-old BEVs and PHEVs at 60,000km saw month-on-month increases of 5.3% and 8%, respectively. Only petrol vehicles suffered a slight month-on-month decrease in their average absolute RV, down 0.5%.

Although the overall situation is positive, used cars saw a longer turnover rate compared with January 2026 and February 2025. The only exception was BEVs, which sold 13.3 days faster than 12 months ago. Despite this, the powertrain still took the longest time to sell.

The model with the best rotation times in February was the Dacia Sandero, with an average rotation of 42.4 days. Then came the Volkswagen T-Roc with 51.2 days, and the Toyota Corolla with 53.5 days.

Switzerland sees weaker RVs

Used‑car demand in Switzerland made a good recovery in February. The SVI surged by 48.5% month on month. Despite this rebound, demand remained 2.1% lower year on year, indicating continued pressure compared to early 2025.

Supply conditions softened slightly. The AMVI fell by 2.3% month on month but remained 5% above last year’s level. This confirms that stock availability is still higher than in early 2025 despite the temporary dip.

‘%RVs weakened in February,’ Madas commented. ‘The average %RV of a 36‑month‑old car at 60,000km dropped to 41.7%, down 0.8pp month on month and 2.9pp year on year. This underlines the ongoing depreciation pressure in the Swiss used‑car market.’

In absolute terms, trade RVs decreased slightly to CHF 26,501 (€29,062), a 0.9% month‑on‑month decline. Yet, this was still 0.9% higher year on year.

List prices continued to rise, averaging CHF 63,610, representing a 1.2% increase month on month and an 8.1% rise year on year. This ongoing inflation in list prices helps support absolute used‑car values, even with falling %RVs.

HEVs still on a high

HEVs retained the most value of any powertrain in February by far at 46.7%. Then came petrol-powered cars at 43.2%, diesel-powered models at 41.5% and PHEVs at 39.7%. BEVs continued to be the worst-performing technology, holding only 35.5% of their original list price.

The average time to sell a used car increased marginally in February, rising to 77.9 days. This was 0.4 days slower month on month, but still a strong 4.3‑day improvement year on year. This reflects better turnover conditions than in early 2025.

HEVs sold fastest at 69.4 days, followed by BEVs at 75 days. This was followed by diesel cars at 77.2 days and petrol-powered models at 78.6 days. PHEVs which took 82 days to leave forecourts.

Looking ahead, %RVs are forecast to decrease further in the coming years, but at a slower pace. By the end of 2026, %RVs are expected to fall by 1.4% compared to December 2025. A further 0.5% drop is anticipated in 2027.

UK sees strong growth

‘The UK’s used-car market recorded strong growth in February 2026,’ commented Jayson Whittington, regional head of valuations for the UK. ‘Overall, there was a clear upswing in sales momentum, led by electrified powertrains. However, pricing pressures remained evident across most fuel types.’

All fuel types posted positive month-on-month SVI gains. On average, the metric was up by 25% across all powertrains, highlighting broad demand.

BEVs led the market with a 29.8% rise, closely followed by PHEVs at 29.6%. HEVs recorded a 26.3% increase, reflecting strong consumer interest in electrified choices.

Petrol models performed well with a 24.8% month-on-month increase, driven by continued affordability and availability. Diesel, while posting the lowest rise at 16.1%, still demonstrated strong growth for a fuel type facing long-term declines.

Despite the uplift in retail activity, the overall time taken to sell a used vehicle increased by 2.7 days to 46 days. BEVs once again led the way, taking an average of 37.4 days to sell. They were supported by fast-turning models, including the Tesla Model Y at 22.6 days and the Volvo C40 at 23.7 days.

%RVs of 36-month-old cars at 60,000km were more mixed. Month on month, the overall %RVs slipped 0.8pp to 49.1%. The value retention of petrol-powered cars fell by 0.8pp as well, to 50.5%. Meanwhile, PHEV %RVs softened by 1.1pp to 46.2%. HEVs declined marginally by 0.2pp to 53.2%. BEVs saw the steepest drop, by 1.6pp to 35.2%. Diesel was the only segment to improve, rising by 1.7pp to 57.4%.

Not every automotive recall requires a workshop visit. Some fixes can now be delivered over the air while the vehicle is parked. So, what actually is a recall, and why do they happen? Autovista24 journalist Tom Hooker investigates.

An automotive recall is a formal safety action. It is used when a vehicle, a component, or a piece of software, is found to create an unacceptable safety risk. A recall may also be issued if a vehicle does not comply with safety requirements.

For owners, the key point is straightforward. The manufacturer must provide a remedy, which is normally free of charge. That fix might be a physical repair, a replacement part, or a software update.

Why do recalls happen?

Recalls usually arise due to evidence from the field. This includes customer complaints, internal testing or an investigation by a safety authority. Causes can range from defective parts fitted during production to a design weakness that only appears after a certain amount of mileage.

Recall terminology can also vary by region. Some markets separate safety recalls from voluntary service campaigns. These are fixes that improve a vehicle’s quality or compliance but are not classed as an immediate safety risk.

The recall process is relatively similar across the world. First, manufacturers identify the affected vehicles. This is often done using the vehicle identification number (VIN). Production dates and factory records may also be used.

Then, carmakers will notify the relevant transport authority before contacting the vehicle’s owner with instructions.

A recall involves many moving parts. Dealers and manufacturers must manage component supply, workshop capacity, customer communication, and completion rates.

Dealership recalls and virtual recalls

Traditionally, recalls have been carried out in a workshop. In this procedure, an appointment is booked, the repair is carried out, and the job is logged as completed.

However, as vehicles become more software-defined, the shape of a recall is evolving, from workshop fixes to remote updates. These are known as over-the-air (OTA) updates, and are delivered wirelessly, without any physical connection to the vehicle. This can reduce inconvenience for drivers.

If the defect is purely software-based, the remedy can sometimes be deployed remotely. In some cases, an OTA update can be offered alongside dealer repair for vehicles that also need hardware work.

Commercial recall importance

For consumers, recalls are about safety, time, and trust. However, for businesses, it is a matter of time and resources. Fleets and rental operators may need to pull vehicles from service. Meanwhile, dealers need to absorb extra workshop demand, sometimes alongside parts constraints.

For manufacturers, recalls not only create direct costs but can also cause undesirable longer-term effects. This includes reputational damage and weaker used-car confidence. In turn, this can put pressure on residual values.

So, a recall is not just a repair notice. It is a structured intervention intended to improve vehicle safety and prevent breakdowns or accidents before they happen.

The balance of physical and virtual recalls may continue to shift in the years ahead. Yet the objective remains the same. Identify the risk, notify the customer, and remove the hazard.

How did Europe’s biggest used-car markets perform in 2025? Is a slow start to the EU’s new-car registrations cause for concern? Plus, an important autonomous vehicle partnership takes shape. Autovista24 special content editor Phil Curry presents The Automotive Update podcast.

In this latest episode, a look at the biggest used and new-car markets across Europe. Also, an expert-led overview of the new award-winning Mercedes-Benz CLA. Plus, news on a delay to the EU’s Industrial Accelerator Act.

Subscribe to the Autovista24 podcast and listen to previous episodes on Spotify, Apple and Amazon Music.

Europe’s used-car markets in 2025

While seeing overall volume increases, Europe’s major used-car markets experienced mixed fortunes in 2025.

Spain enjoyed a largely positive year. The market was up by 4.4% compared to 2024, based on Autovista24 analysis of available data from industry body GANVAM.

Italy followed in terms of volume growth, in contrast to the performance of its new-car market. It emerged as the most stable of Europe’s largest markets, with May posting the only monthly decline in the year.

The UK market signalled a 2.2% increase in transactions across the 12-month period, according to data from the SMMT.

The French used-car market struggled after a strong start to the year, but still recorded a positive result, in contrast to its new-car registrations. Meanwhile, Germany provided the least favourable performance of the big five markets in 2025.

Slow start to 2026 for EU new-car market

For the second consecutive year, the EU saw a fall in new-car registrations during January.

In total, just 10 EU member states saw year-on-year increases in new-car registrations during the month. This result brought an end to six months of consecutive growth.

The figures from ACEA suggest that the popularity of hybrids, including both full and mild hybrids, may have peaked. The powertrain group secured 38.6% of the market, a new high, with volumes rising 6.2% in the month.

Meanwhile, registrations of battery-electric vehicles and plug-in hybrid volumes increased. Conversely, the trend of new petrol and diesel registration declines continued.

Which brands thrived in the EU during January?

Chinese-brand BYD began 2026 with strong sales in the EU’s new-car market. The relative newcomer saw deliveries surge by 175.3% year on year. Meanwhile, other carmakers faced varying degrees of success.

Volkswagen Group (VW) took the top two best-seller spots, with the VW and Skoda marques. However, VW registrations fell by 10.6% in the month, while Skoda saw a 10.7% uplift in deliveries, according to ACEA data.

Stellantis posted year on year growth of 9.1% in the first month of 2026. Conversely, Renault Group endured a delivery decline of 16.7%, with the brand’s total down 36.7% year on year.

The new battery-electric variant took the title of European Car of the Year 2026 at the Brussels Motor Show, giving the German carmaker its first win in 52 years.

Highlights include its sleek design and impressive interior, alongside an electric drive system that can provide a 777km (483 miles) of driving range. Together with an 800-volt architecture, using a rapid charger, it can recharge around 300km of range in 10 minutes.

Delay to crucial new policy announcement

The European Commission has delayed its announcement to prioritise industrial parts and products made in Europe by a week. This follows disagreements over the geographic scope of the scheme.

The Industrial Accelerator Act aims to set minimum thresholds for locally made parts in projects using public funds in strategic sectors. This includes batteries, solar and wind energy, and nuclear power. It will now be unveiled on 4 March, Reuters reported.

Wayve closer to UK robotaxi launch

UK self-driving start-up Wayve has raised $1.2 billion (€1 billion) in new funding from investors, including Mercedes-Benz, Stellantis, and Nissan. The brand is gearing up to launch its first robotaxi service in London later this year, the Financial Times reported.

The company has said that Mercedes-Benz and Stellantis are exploring using Wayve’s autonomous driving systems. These can be used for both robotaxis, and privately owned vehicles.

Existing investors Eclipse, Balderton and SoftBank Vision Fund 2 led Wayve’s latest round, alongside US tech groups Nvidia, Microsoft and Uber, bringing its total capital raised to $2.5 billion.

As BYD began 2026 with soaring sales in the EU’s new-car market, other carmakers faced mixed fortunes. This came as the region saw declining registration results. Tom Hooker, Autovista24 journalist, takes a look at January’s winners and losers.

As new-car sales dropped in the EU during January, the picture for carmakers proved more nuanced. As some established brands recorded losses, other newer entrants enjoyed success, shaking up the established order.

BYD certainly bucked the overall trend. The Chinese marque saw deliveries surge by 175.3% year on year to 13,982 units, according to ACEA. This gave the carmaker a 1.7% share of the EU new-car market, up by 1.1 percentage points (pp) compared to January 2025.

The brand is looking to double its points of sale in Europe to 2,000 this year, according to Reuters. BYD is targeting 350 distribution partners in Germany by the end of 2026, Handelsblatt wrote.

BYD also recorded higher volumes than the likes of Mini, Mazda, Honda, Lancia and Alpine. While claiming smaller market shares than BYD, these brands all enjoyed growth in January as well. However, none of them recorded triple-digit growth.

Mercedes-Benz also recorded improvements. It managed a 4% boost to 36,074 units. Its hold of the new-car market grew by 0.3 percentage points (pp) to 4.5%.

Strong start for Stellantis brands

As a group, Stellantis posted year-on-year growth, recording 145,750 sales last month. This ensured a 9.1% increase on 12 months prior, while its market share rose from 16.1% to 18.2%. The carmaker recently announced that it is reintroducing diesel versions of some of its models in Europe, Reuters reported.

Fiat, including the Abarth brand, recorded the group’s highest growth rate. The Italian marque witnessed a 31.3% uptick in volumes to 28,992 units. Combined Opel and Vauxhall figures grew by 17% year on year to 24,575 units. Citroen and Peugeot recorded rises of 9.6% and 0.5% respectively.

The combined deliveries of Lancia and Chrysler saw a significant rise compared to January 2025. However, the 21.9% surge was based on a much smaller total of 1,282 units. Alfa Romeo and DS weighed on the overall group’s performance. Both brands suffered a 13.8% decline in January.

Brands struggling in the EU

On the other side of the coin, Renault Group endured a sales fall of 16.7% to 75,243 units. The carmaker accounted for 9.4% of overall volumes, down 1.5pp year on year.

This was mostly due to a decline in Dacia deliveries, with the carmaker’s 29,165-unit total down 36.7% year-on-year. The marque trailed the Renault brand by 16,319 sales. This compares to a 2,309-unit lead over the OEM’s namesake brand at the same point last year.

Conversely, the Renault brand posted a 3.9% improvement to 45,484 sales. Renault Group’s figure was further boosted by a 34.4% surge in deliveries of Alpine models. However, this was based on a smaller volume of 594 units.

Kia and Hyundai contributed relatively evenly to their group’s result in January, shifting 28,393 units and 26,562 units, respectively. However, their performance compared to 12 months ago was vastly different. While Kia’s total equated to a 5.9% fall, sales of Hyundai models plummeted by 22.4%.

Japanese carmakers fall behind

Toyota and Lexus were also unable to escape declines last month. Their wider manufacturing group posted a 14.3% slump, with 61,572 deliveries. The OEM represented 7.7% of overall volumes, down 0.9pp year on year.

Suzuki faced a 14.6% delivery drop to 10,876 units, as its share slipped from 1.5% to 1.4%. Nissan suffered a 16.2% drop to 14,399 units, as its share fell by 0.3pp to 1.8%.

Meanwhile, Volvo Cars suffered a 13.6% drop to 15,877 units. Yet its market share fell by only 0.2pp to 2%. Jaguar Land Rover (JLR) felt a 12.5% decline in January. However, its total was based on lower volumes relative to other OEMs. Its hold on the new-car market went from 0.6% to 0.5%.

Deliveries of Land Rover models decreased by 9.1% year-on-year, but the group’s poor performance was mostly due to Jaguar. According to ACEA, the brand recorded no sales in January. The marque’s first model since its polarising rebrand in 2024 is expected to be revealed this year, ABC News reported.

VW’s stagnant EU sales

VW Group faced a 3.7% sales decline in January to 219,708 units. Despite this, the OEM continued to lead Europe’s new-car market, with a 27.5% share, up 0.1pp year on year.

The drop was softened by Skoda’s 10.7% uptick to 57,619 deliveries during the month. However, this was not enough to make up for significant losses endured by the VW brand and Cupra. The group’s namesake saw sales fall by 10.6% to 85,841 units, while Cupra endured an 11.6% slump to 15,746 sales.

The latter’s Tavascan model has been exempted from EU import duties, in line with an accepted minimum import price. It was the first car to be approved following the publication of the European Commission’s guidelines.

Audi and SEAT did not help matters, with 1.9% and 1.5% declines, respectively. However, it was Porsche that felt the biggest drop in the VW Group. The premium carmaker recorded a 14.6% slide on a relatively lower total of 5,285 deliveries.

BMW Group saw sales slip by 3.3% last month. Its 53,456-unit total translates to a 6.7% market share. The group’s namesake brand alone suffered a 6.4% fall to 45,031 deliveries. Meanwhile, Mini enjoyed a 17.4% surge in volumes, albeit on a smaller 8,425-unit total.

Tesla saw a minimal drop in January. The electric-only brand posted a 1.6% decline to 7,187 deliveries, as its 0.9% share remained stable from January 2025. Additionally, SAIC Motor had an even smaller drop of 0.8%, with 13,790 units and a 1.7% share.

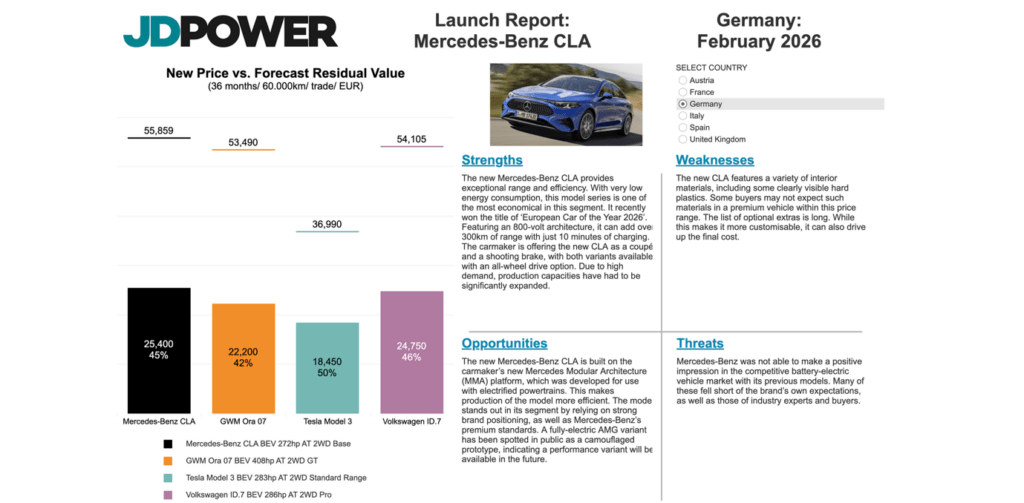

As an award-winning car, the Mercedes-Benz CLA is already proving itself on the European stage. But how does this translate into expected residual value (RV) performance? Autovista24 special content editor, Phil Curry, reviews the model alongside regional experts.

The new Mercedes-Benz CLA battery-electric vehicle (BEV) is providing the German carmaker with headlines. At the Brussels Motor Show, the model was presented with the European Car of the Year title for 2026.

The success of the model, voted for by motoring journalists across Europe, highlights the prowess of the CLA. With an impressive design, comfortable handling and strong driving range, it offers much to buyers.

Autovista24’s latest Launch Report benchmarks the Mercedes-Benz CLA against its key competitors in Austria, France, Germany, Italy, Spain and the UK. Regional experts also provide a breakdown of the car’s strengths, weaknesses, opportunities and threats.

A bright start for design

The new model cuts an impressive figure in either a coupé or shooting-brake body style. This gives the CLA sleek lines and a low profile that provides a premium look. Although this comes at the cost of practicality.

Source: Mercedes-Benz

At the front, the false grill features 142 stars, which illuminate at night, providing a striking visual component. This is not the only use of the three-pointed star. Alongside the traditional Mercedes-Benz logo, the pattern is used in the headlights.

The LED light bar extends across the front above the grill, continuing a trend seen on other Mercedes-Benz electric models. However, it looks slightly out of place, sitting high up above the grill, impacting the clean lines. On the plus side, the bar does provide increased visibility at night.

The sweeping side profile and simple rear styling provide a sporty look but remain reminiscent of internal-combustion engine (ICE) models. Carmakers can develop BEVs with an outlandish design, but this runs the risk of alienating some buyers. In this guise, the CLA will appeal to a broader range of drivers.

Inside the Mercedes-Benz CLA

Inside, the Mercedes-Benz CLA is comfortable, with a low seating position up front contributing to the sporty feeling. For the most part, material quality is good, although some hard plastics point away from the overall premium feel.

The new CLA utilises the Mercedes-Benz Operating System (MB.OS). This provides an AI-enhanced experience, capable of adapting to the driver’s mood and providing quicker responses to queries. The infotainment system is also quick and intuitive. On-board navigation uses Google data, providing accurate information on travel and road conditions.

Source: Mercedes-Benz

Sweeping around the dashboard are a pair of screens, including the central 14-inch touchscreen, which houses the infotainment system. Behind the steering wheel is a 10.25-inch driver display. The carmaker offers the MBUX Superscreen setup, which places a third, 14-inch screen in front of the passenger. This allows them to stream videos and have their own display separate from the driver.

Questionable controls

The German carmaker has embraced the touchscreen control culture that others are starting to pedal back on. Many of the basic controls in the CLA are found within the infotainment system’s menus, rather than on physical buttons. These are easier to find than in some other models, but could prove distracting.

This includes the window demisters and heated seating controls. Drivers will also have to find the option to switch the window buttons from front to rear, with only two physical controls for these.

Source: Mercedes-Benz

Additionally, while the steering wheel is high quality, the touch-sensitive buttons can prove troublesome. These have been switched for physical components in other vehicles, but Mercedes-Benz has stayed the course.

Another questionable control option is the location of the regenerative braking settings. The CLA does not feature paddles behind the steering wheel. Instead, the driver flicks the gear selector lever located behind the steering wheel, making the control more awkward.

Source: Mercedes-Benz

The new CLA also struggles with practicality. While there is plenty of space in the front, rear-seat passengers are affected by the coupé-style roofline and high floor. Boot space is also at a premium, with just 405 litres available. However, the CLA does offer a 101-litre frunk, providing an alternative storage location.

Impressive range from Mercedes-Benz CLA

The new CLA features an 85kWh battery and a single 272hp electric motor. This provides an impressive 483-mile (777km) range. While the BMW iX3 offers 500 miles, it has a much larger battery.

Built on the new Mercedes-Benz Modular Architecture (MMA) platform, designed for both BEV and hybrid powertrains. The CLA also uses an 800-volt system. This allows the battery to charge at up to 320kW. This allows for over 190 miles of range to be added in 10 minutes.

However, the current system requires either rapid chargers or DC charging at home, and will not work with other charging systems. An optional convertor is planned for future models, according to Auto Express.