Fleets flocked to Flotte in Germany, with industry experts taking to the stage to share vital insights. Autovista24 editor Tom Geggus finds out what happened at the event in the latest Automotive Update podcast.

In this episode, Dr Christof Engelskirchen, chief economist and director of professional services, Europe, JD Power, shared his Flotte insights. This includes electrification, the role of fleets, and the opportunities and risks for these businesses.

Taking place between 25 and 26 March in Düsseldorf, Germany, Flotte welcomes Germany’s fleet industry experts and decision makers.

Among them was a team from JD Power, including Dr Christof Engelskirchen, who gave a presentation at Flotte. His session was titled ‘E-mobility in the headwinds – fleets as a beacon of hope and risk factor’. Speaking with Autovista24 editor Tom Geggus, he outlined some of the major points from this presentation.

Of all the topics that could be presented to a room full of fleet professionals, one stood out: electrification. Fleets play an important role in the push towards electric vehicles, while the technology presents big risks and opportunities.

Fleets behind the steering wheel

In major EU new-car markets, electrification continues to be a subject in the headlights. Battery-electric vehicles (BEVs) currently make up under 30% of new-car registrations in each of Germany, France, Italy and Spain, according to ACEA.

‘That is a long way to go when you consider what the EU has been prescribing, which used to be a 100% tailpipe CO2 emission reduction by 2035 and is now becoming a 90% reduction,’ Engelskirchen said. ‘So, we have that gap that needs to be bridged.’

One of the biggest markets in the region, contributing heavily to the powertrain development, is Germany. With a large fleet industry making a significant proportion of registrations, these businesses will be vital to electrification.

Weighing things up at Flotte

There are sizeable opportunities for fleets within this transformation. Engelskirchen outlined that one of the biggest opportunities is the additional volume that is running through leasing companies and banks.

Other buyers, such as private consumers and other companies, may not want to hold BEV asset risks. But this is not a result of disliking the powertrain. It is because it is not their core business to manage asset risks. Instead, this is the business of banks and leasing companies, Engelskirchen outlined.

Leasing companies are now shifting their portfolios from what was 95% internal-combustion engine vehicles towards a greater balance. By 2035, it is conceivable that these fleets will have changed massively in favour of BEVs. However, this transition brings about its own risks.

‘You do need to get your head around the different residual value and depreciation profiles of electric vehicles. It is very dynamic,’ said Engelskirchen. ‘It certainly requires additional variables to consider in your risk management.’

Car manufacturers have experienced contrasting fortunes in the EU’s new-car market so far this year. As Stellantis deliveries soared, other players saw sliding registrations. Tom Hooker, Autovista24 journalist, reviews the data.

Within a stagnant EU new-car market, competition between carmakers continues to intensify. While some brands are gaining ground, others are seeing declines. This inconsistency is also apparent when looking at the biggest manufacturers, such as Stellantis.

According to ACEA, the group enjoyed a 9.5% year-on-year delivery increase to 304,251 units between January and February. This equated to an additional 26,478 registrations. In turn, its share surged by 1.8 percentage points (pp) to 18.3%.

Fiat and Opel registrations soar

Stellantis’ growth in the EU was driven by Fiat and Opel. Compared to the first two months of 2025, the carmakers contributed a further 29,216 units to the group’s total.

Between January and February, Fiat saw registrations surge by 42.1% year on year to 63,004 units. Consequently, its share rose by 1.2pp to 3.8%. Fiat was one of only two marques in the EU’s top 10 best-selling new-car brands to grow in this period.

Opel’s slice of the EU new-car market widened to 3.2% from 2.5%. Volumes improved by 25.1% to 52,531 deliveries. A solid Citroën result also helped Stellantis achieve growth. The marque recorded an 8.3% rise to 60,345 registrations. Its share also notched up by 0.3pp to 3.6%.

Peugeot plummets

However, the manufacturer group’s highest volume brand counteracted these performances. Peugeot suffered a 5.2% delivery drop after two months of the year to 92,704 units. The carmaker still accounted for 30.5% of Stellantis’ overall registrations.

With such a high share within the group, any decline from the French brand has a big impact. Peugeot represented 5.6% of the total EU new-car market, down from 5.8% at the same point in 2025.

Meanwhile, Jeep saw stable registrations in the first two months of 2026, with a 0.8% delivery increase. However, this was to a lower volume of 20,866 units.

Based on smaller volumes, Alfa Romeo and DS suffered double-digit declines across January and February. Alfa Romeo struggled with a 16.3% drop, while DS saw deliveries fall by 21.5%. However, combined registrations of Lancia and Chrysler models rose by 15.9%.

Renault Group’s downbeat result

Renault Group endured a steep decline in the year to date. Deliveries slumped by 16.1% to 161,262 units. Its share also fell from 11.4% to 9.7%. Dacia appeared to drive this trend. A 30.9% drop for the brand translated to 63,579 units, as its market hold dropped by 1.7pp to 3.8%.

This meant Dacia trailed the Renault brand by 32,818 registrations across the first two months of 2026. In comparison, the gap between the two brands stood at just 7,018 units during the same period of 2025.

The Renault brand suffered a 2.7% drop to 96,397 deliveries in the year to date. Its share remained relatively stable at 5.8%, down just 0.1pp year on year. Conversely, Alpine recorded a 10.3% increase in registrations on significantly lower volumes of 1,286 units.

Stagnant VW Group registrations

As Stellantis surged and Renault Group slipped, Volkswagen (VW) Group’s registrations were down only slightly. Volumes dropped 0.7% between January and February to 449,294 units. However, as many carmakers suffered declining deliveries, the manufacturer’s share improved by 0.1pp to 27%.

VW Group’s stagnation was the result of contrasting performances from its two highest volume marques.

The VW brand witnessed a 7% decline after two months of 2026, with 176,570 deliveries. It accounted for 10.6% of overall registrations, down from 11.3% during the same period of last year. Meanwhile, Skoda saw a 14.5% surge to 116,650 units. In turn, its share jumped by 1pp to 7%.

Audi volumes were nearly unchanged year on year. The brand’s 81,804 deliveries across January and February represented a 0.1% dip, as it kept its 4.9% market hold. SEAT had a slightly better performance, with a 1.8% uptick to 30,782 registrations. This gave the carmaker a 1.8% share, stable from 2025.

However, Cupra and Porsche counteracted these results. The former faced an 11.4% fall to 32,151 units after two months of 2026. Cupra accounted for 1.9% of overall volumes, down 0.3pp year on year. Porsche posted an 10.6% slump to 10,159 registrations, with a 0.1pp drop in share to 0.6%.

BYD continues triple-digit growth

While some struggled, BYD maintained its strong upward trajectory in the EU during January and February. It maintained triple-digit delivery growth, with a 179.2% surge to 29,291 units. The brand captured 1.8% of the EU’s new car market, up 1.2pp year on year.

Tesla also enjoyed growth, with deliveries up 16.7% compared to the first two months of 2025. The brand’s 20,941 registrations ensured a 1.3% share, up 0.2pp. Honda achieved a double-digit delivery increase, as well. However, this was based on a lower figure of 7,888 units, as its market share rose by 0.1pp to 0.5%.

SAIC Motor managed a 6.6% growth between January and February, with 32,214 new models taking to EU roads. It made up 1.9% of overall volumes, up 0.1pp year on year. Meanwhile, registrations of new Mazda models improved by 0.5%. With 17,757 deliveries, it took a 1.1% market share, up from 1% during the same period of 2025.

Mitsubishi’s registrations woes

However, these examples of growth were few and far between. On the other end of the spectrum, Mitsubishi suffered a 43.3% slump in the first two months of 2026. The brand’s 3,828-unit total translated to a 0.2% share, down from 0.4%.

Ford endured a tough result as well, with volumes dropping 21.5% between January and February to 41,039 units. The marque captured 2.5% of overall registrations in the EU, down from 3.1% in the first two months of 2025.

JLR posted a 14.3% slump year on year to 8,376 units. Its slice of the new-car market thinned by 0.1pp to 0.5%.

Within the group, Land Rover recorded a less severe decline of 10.2%. However, this was compounded by Jaguar’s absence, down from 446 registrations between January and February 2025.

Another double-digit drop was recorded for Suzuki. Deliveries slid 14% year on year to 22,957 units, while its share fell by 0.2pp to 1.4%. A similar trend occurred at Volvo Cars, with its 33,143-unit total representing a 12.8% decline. It captured 2% of overall volumes, down from 2.3%.

Adding to the list of carmakers with falling registrations, Nissan felt a 12.2% downturn after two months of the year. It represented 1.9% of the EU’s new-car market with 31,884 registrations.

More registrations declines

Hyundai Group, made up of Kia and Hyundai, posted a 9.2% fall year on year to 115,614 registrations. The group captured 6.9% of total volumes in the first two months of 2026, down 0.7pp.

Kia experienced a more marginal drop of 1.8%, with 60,044 registrations giving it a 3.6% share, stable year on year. However, Hyundai fuelled the group’s slump, after a 16% decline to 55,570 deliveries. In turn, its share fell 0.6pp to 3.3%.

Toyota Group posted a similar headline figure and decline. The brand recorded 126,354 units after two months of 2026, down 7.7% year on year. Unsurprisingly, its grip on the new-car market loosened by 0.5pp to 7.6%.

Lexus saw a significant drop of 20.9% compared to the same period of 2025, while Toyota brand registrations slipped by 6.5%. The latter’s 117,510-unit total translated to a 7.1% share, down 0.4pp year on year.

BMW Group also entered six-digit figures after two months of deliveries. Yet the manufacturer still suffered a 3.6% decline to 109,790 units. It made up 6.6% of overall volumes, down from 6.8%.

This came despite Mini’s 5% increase to 17,628 units, which helped boost its share by 0.1pp to 1.1%. However, a 5.1% drop for the BMW brand ensured the group’s negative result. A total of 92,162 new models from the carmaker were delivered, as its share went from 5.8% to 5.5%.

Mercedes-Benz also endured falling volumes after two months of 2026. The marque recorded a 1.2% decline to 74,422 units. This ensured a 4.5% share, stable from the same period one year prior.

A challenging start to the year for the EU’s new-car market was tempered in February. However, a return to growth was offset by a wider slowdown. So, which countries and powertrains enjoyed growth? Autovista24 web editor James Roberts investigates the latest data.

In February, the EU’s new-car market returned to growth. According to ACEA, a total of 865,437 new passenger cars were registered. This equated to a volume rise of 1.4%, following on from January’s 3.9% decline. Two months into 2026, the EU new-car market fell by 1.2% overall. A total of 1,664,680 new units were registered across member states.

Regional new-car market growth

In total, 20 nations witnessed new-car market growth in February. Of the big four EU markets, Italy enjoyed the most significant improvement at 14%. This was underpinned by a significant electric vehicle (EV) volume increase, including battery-electric vehicles (BEVs) and plug-in hybrids (PHEVs). The latent impact of 2025’s incentives played a sizeable part in this trend.

Spain’s new-car demand continued to prove positive, albeit slightly muted compared with previous months. Buoyed by continued strong EV demand, overall volumes increased by 7.5% year on year. Meanwhile, the bloc’s largest market, Germany, returned a solid 3.8% market growth in February.

France continued a distinctly negative trend. Despite relatively strong increases in BEV deliveries, registrations fell across hybrid, petrol and diesel variants. This dragged the market to a sizeable 14.7% decline.

Poland continued its EV-driven trend of prosperity. The EU’s fifth-largest market enjoyed a 6% upswing. In percentage terms, Estonia has rebounded from significant declines in 2025 to an 82.4% lift in its new-car market fortunes. This meant 1,138 new cars were delivered in February.

Other notable slumps occurred in the Netherlands, which witnessed a 19% dive in new-car deliveries. This was triggered by a double-digit drop in petrol and BEV figures, as hybrid registrations also dipped. However, this can be skewed by the country’s relatively large company car market.

Neighbouring Belgium saw deliveries fall across all powertrains except petrol. This resulted in a 7.7% year-on-year slide as the country’s market continued to decline.

PHEVs proving popular in EV push

Total new EV registrations, combining BEV and PHEV volumes, amounted to 242,052 in February. This ensured a 28% share of the overall EU market, up 5.2 percentage points (pp), according to Autovista24 calculations.

BEV registrations in the EU increased by 20.6% with 158,280 units leaving dealerships in the month. In total, 22 nations saw all-electric registration increases. This resulted in all-electric cars accounting for 18.3% of all new-car deliveries in the EU, an increase of 2.9pp year on year.

Meanwhile, PHEVs accounted for 9.7% of the overall EU new-car market. This was enabled by a sizeable 32.1% volume increase compared with February 2025. ACEA stated that the powertrain’s popularity underlines ‘the importance of a technology-neutral pathway to decarbonisation.’

In some of the EU’s largest markets, PHEV demand helped boost overall plug-in totals. Italy led the way in February with triple-digit PHEV increases amounting to 101.7%. This was coupled with a healthy 81.3% surge in year-on-year BEV demand.

This trend was echoed in Spain. Amid a new national incentive framework, PHEV popularity increased 75.2%, while BEVs improved by 45.4%. However, local industry bodies exercised caution when considering the longer-term impact as new legislation takes shape.

New purchase incentives in Germany seemingly boosted the overall market in February. The EU’s bellwether market saw BEV and PHEV volumes grow by 28.7% and 24.5% respectively.

EV uptake in France exposed the nation’s wider new-car market contradictions. Despite a 27.8% increase in BEV volumes and a 3.2% lift for PHEVs, the wider market fell thanks to lower internal-combustion engine (ICE) deliveries.

Denmark’s new-car market BEV boost

February saw Denmark consolidate its position as an EU BEV market leader. The country saw 9,736 new BEVs take to the country’s roads, according to ACEA.

Conversely, its PHEV volumes declined by 60.9%. Hybrids, made up of mild and full-hybrid powertrains, took at 19.8% tumble, and petrol plummeted by 72%. Despite this, the overall new-car market grew by 2.8%, suggesting that, unlike other markets, BEV growth can support wider market prosperity.

Poland continued to return impressive EV numbers in February. BEV volumes increased 12.9% year on year, while PHEVs improved by 90.3%.

The country’s NaszEauto incentives programme has boosted registrations since 2024. The sustained growth of the sector explains the relatively low double-digit year-on-year increases in February, after triple-digit monthly trends.

Despite being a smaller EU new-car market, Croatia recorded notable EV growth in February. The country’s BEV sector witnessed a 217.7% surge, while PHEV popularity increased 140%. Overall, the country saw year-on-year gains of 14.7% with 4,869 units registered.

EU hybrid hegemony continues in February

In the month, 334,791 new hybrid vehicles took to the EU’s roads. This marked a 10.1% year-on-year upswing, plus a dominant 38.7% market share, up 3pp. Adding hybrid volumes to BEV and PHEV registrations provided a total electrified vehicle figure of 576,843 passenger cars. This secured 66.7% of the EU new-car market in February, an increase of 8.2pp

Germany, Italy and Spain all saw hybrid delivery growth in February. Most notable was Italy, where 81,799 new passenger cars underpinned a year-on-year uplift of 33.9%. In the year to date, Italy boasts the highest number of new hybrid registrations at 156,215 units.

In France, a lacklustre month for hybrids added to overall new-car market volume woes. Despite the EV volume rise, the nation’s hybrid market contracted by 7.2% with 57,670 deliveries. Aligned with significant falls in ICE uptake, this is harming overall growth.

ICE versus EVs

In February, total new ICE registrations, combining petrol and diesel models, reached 270,276 units. This continued a trend of decline with a volume drop of 16.6%. Accordingly, a year-on-year market share fall of 6.8pp to 31.2% followed.

Two months into 2026, the overall petrol and diesel market share stood at 30.6%. This was 1.9pp above the EV share. At the end of January, the gap was just 1pp, suggesting the electric market will have to push hard to overtake ICE this year.

In February, petrol remained a resilient new-car choice. The fuel type held on to a 23.1% market share, albeit down 5.4pp. This was despite a sizeable 17.9% volume decline. This was still the second-best-selling powertrain in the EU, with 199,910 deliveries. In total, 10 nations saw year-on-year increases in new petrol car registrations.

Meanwhile, new diesel registrations in February amounted to 70,366 passenger cars across the EU. This signalled a 12.8% fall, securing an 8.1% market share, down 1.3pp. The fuel type saw year-on-year declines in all but 11 member states.

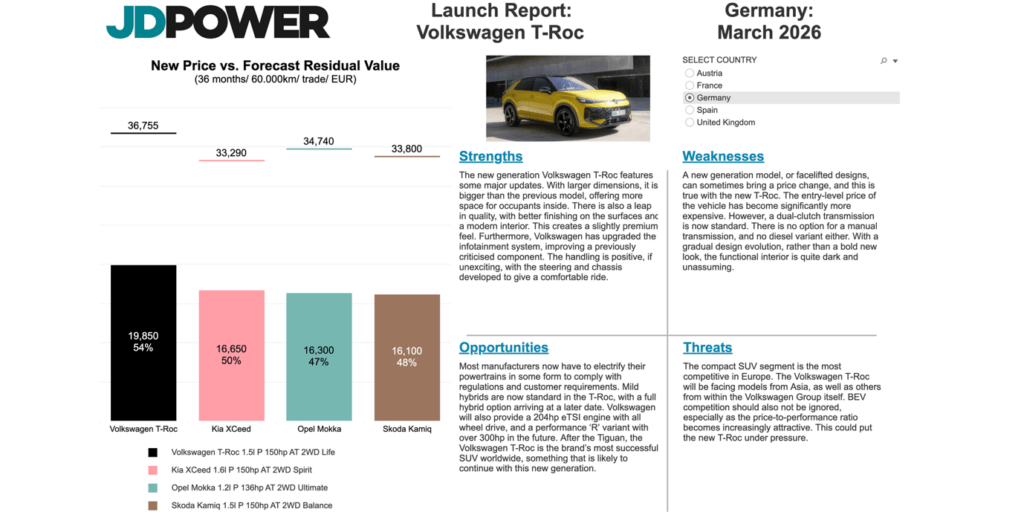

The second generation of the Volkswagen (VW) T-Roc has been long-awaited. But do improvements to the SUV make it more appealing? Autovista24 special content editor Phil Curry reviews the model alongside regional experts.

The VW T-Roc sits between the Tiguan and the T-Cross in the carmaker’s SUV lineup. Now the second generation aims to maintain the momentum of the first.

To do this, the manufacturer appears to have listened to drivers. VW has updated what already worked and changed what did not in the first generation. In doing this, they have created a new model that is expected to appeal instantly.

Autovista24’s latest Launch Report benchmarks the VW T-Roc against its key competitors in Austria, France, Germany, Spain and the UK. Regional experts also provide a breakdown of the car’s strengths, weaknesses, opportunities and threats.

Evolution of the T-Roc

VW has adopted an evolutionary design philosophy for the new T-Roc. However, it is bold enough to work. Sometimes transitional styling options can make a new model feel old or unappealing. Yet the carmaker has created something which stands out, making it attractive to new and old buyers.

The new T-Roc links into VW’s current design language. It features a lower grill and a sweeping LED light bar across the front end, between the narrow headlights. There is also an illuminated badge to show the branding even at night. This does make it look reminiscent of the ID. range, but with no battery-electric option, this could prove polarising.

Source: VW Press UKSource: VW Press UKSource: VW Press UK

The rear also features a full-length light bar and an illuminated badge. With a sweeping diffuser, its angular look provides a dynamic profile. The R-Line model leans into its sporty design credentials, with bigger wheels and a bigger grill. It also gets a floating roof, to add to the dynamism.

But the new design also provides the new VW T-Roc with larger dimensions than its predecessor. On the outside, this makes it look bigger and safer, giving it a larger stance. Inside, this means more room for occupants.

A quality interior

While the exterior styling is evolutionary, VW has taken the interior to another level. Inside, the previous generation was rather safe and unassuming. In the new generation, a lot of thought has gone into providing a comfortable, high-quality feel.

Yet it is also not a bold design. A large centre console runs down the middle, separating the driver and passenger while giving a sense of comfortable confinement. The steering wheel is practical, with numerous physical buttons for various vehicle systems. VW has moved away from the ‘slider’ buttons, which proved divisive on other models.

Source: VW Press UKSource: VW Press UKSource: VW Press UK

A display behind the steering wheel provides plenty of driver information, while the 12.9-inch infotainment screen is responsive and clear. The lowest-trim model has a 10.3-inch screen, but it is still a decent size.

The dashboard is large, but the materials used provide a sense of quality. This does not feel like a cheap car. Instead, it feels more premium moving through VW’s SUV range to the top-level Tiguan.

Rear-seat passengers also get plenty of legroom, and headroom is good too. There are plenty of storage areas, while the 475-litre boot provides ample space.

T-Roc on the road

The new T-Roc comes with a complement of 1.5-litre petrol mild-hybrid powertrains, in either 110hp or 150hp offerings. Further engine specs are planned for a future launch, as well as hybrid options. However, there is no pure battery-electric variant currently available.

The carmaker has developed the T-Roc well. It provides a smooth driving experience, with precise steering and effective brakes. However, the ride can get a little bumpy on more imperfect roads. This is particularly pronounced in models with the larger specification alloy wheels.

Source: VW Press UK

Acceleration is effortless and is aided by a dual-clutch system, allowing the seven-speed automatic gearbox to change seamlessly. It all adds up to make driving the T-Roc easy, despite its size.

Overall, VW has re-engineered the T-Roc into a car that drivers want. It provides a quality feel and a better design than its predecessor. However, it has not strayed too far from the popular first model.

In a continually growing automotive segment, with many new players appearing, the T-Roc achieves something different. It does not stand out because it is new, but because it is familiar.

View the interactive dashboard, which benchmarks the VW T-Roc in Austria, France, Germany, Spain and the UK. The interactive dashboard presents new prices, forecast RVs, and SWOT (strengths, weaknesses, opportunities, and threats) analysis.

BYD kicked off 2026 at the peak of an expanding Australian electric vehicle (EV) market. But as both battery-electric vehicle (BEV) and plug-in hybrid (PHEV) demand soared year-on-year in January, is a new challenger emerging? James Roberts, Autovista24 web editor, finds out.

January saw 10,335 new BEVs and PHEVs sold in Australia, according to the latest data from EV Volumes. This ensured a year-on-year increase of 94.1%.

BEVs remained the most popular electrified powertrain in the country, making up 71.6% of total sales. Overall, 7,404 vehicles made their way to customers in January. A 91.3% year-on-year upswing ensured the best start to a year for all-electric vehicle sales.

Although commanding a smaller slice of Australia’s EV market, PHEV popularity is proving strong. January confirmed this trend, as 2,931 units were registered. This marked a 101.6% year-on-year increase, amounting to an additional 1,477 models.

Some of the growth in the Australian EV market is due to the entries of BYD and Geely, and Kia, to flourish. January saw new models from both carmakers occupy the top slots. This has been fostered by an increase in vehicle options. Aggressive pricing strategies from these incoming manufacturers has also increased competition, as reported by CarExpert and CarsGuide.

Meanwhile, previously dominant BEV players, such as Tesla, and PHEV providers, like Mitsubishi and Mazda, have seen their market share eroded.

BYD best of the BEVs

January saw BYD models occupy six positions in the top 10 best-selling BEVs. This top-end-of-the-market eclipse was achieved through a combination of established and newer models.

The BYD Sealion 7 marked 12 months on the Australian EV market as the most popular BEV in January. The fully electric mid-sized SUV shifted an impressive 1,171 units in the month. This meant it held a 15.8% BEV market share.

The BYD Atto 2 followed in second place. In just its third month on the market, the B-segment SUV has enjoyed an auspicious start in Australia. During January, 562 vehicles were delivered, securing a 7.6% market share. Cumulative sales of the Atto 2, since its launch in November 2025, stood at an impressive 1,458 units, according to EV Volumes.

A third Australian market newcomer from BYD made a notable impact in 9th place. Debuting in December 2025, the BYD Atto 1 made a splash in January with 245 deliveries and a 3.3% market share. Competitively priced and aimed at urban driving, the fortunes of this small BEV’s appeal will be something to watch in 2026.

Familiar BYD models succeed in Australia

The BYD Seal, a relative Australian market veteran, claimed fifth spot in January’s BEV rankings. A total of 295 sales underpinned a 467.3% year-on-year boost in volumes, plus a 2.7 percentage point (pp) rise in market share to 4%.

Meanwhile, in eighth, the established BYD Dolphin secured a 3.7% market share, up 1.5pp, with272 sales. This marked a 220% surge in sales compared to 12 months prior.

The BYD Atto 3 rounded out the top 10. First introduced to Australian customers in November 2022, the Chinese carmaker’s first venture into Australasia has proved enduringly popular. In January, this pioneering entry-level EV sold 234 units, marking a 122.9% volume upswing year on year.

In total, BYD sold 2,779 new BEVs in Australia during January, giving the Chinese brand an impressive 37.5% market share. This was an impressive 1,048.3% increase year-on-year, highlighting the brand’s growth in the country.

Who is battling BYD in Australia?

Behind the leading two BYD models, the Geely EX5 emerged as a robust challenger in January, placing third.

Available in Australia since March 2025, one month after BYD’s Sealion 7. the mid-size SUV has enjoyed consecutive monthly triple-digit sales. It kicked off 2026 with 418 deliveries and a 6.6% BEV market share.

Geely-owned EV brand Zeekr followed in fourth with its 7X. Launched in September 2025, its appeal could further grow this year. Launched in September 2025, the all-electric SUV has disrupted the established order. As a faster-charging alternative to both the Tesla Model Y and the BYD Sealion 7, its appeal could grow this year.

Sales strategies of Geely and Zeekr models are aligned under the ‘One Geely’ global framework. January’s strong performance in Australia from Geely-adjacent models chimed with plans to expand its global automotive market footprint.

Core aims include becoming a top-five player in the global automotive market, with 75 % of all vehicles produced heading to export markets.

Additionally, the company is looking to focus on new-energy vehicles, spanning A-to E-model segments. Like BYD, Geely currently offer both BEVs and PHEVs in Australia, suggesting this EV market competition could heat up in 2026.

Tesla’s shaky start to 2026

Mirroring many global EV markets, Tesla’s EV market share in Australia has declined notably. Amid increased competition, this was reflected in January’s overall BEV sales.

The US manufacturer’s Model Y witnessed a 38.1% year-on-year volume slide. In total 288 units reached customers in Australia, carving out a 3.9% market share, a sizeable 8.1pp fall compared to 12 months prior. Similarly, the Tesla Model 3 ended up 12th in the BEV best-sellers rankings with 213 sales.

Korean carmaker Kia also saw its leading BEV ebb in popularity. With 281 deliveries, the Kia EV5 saw a 2.8% year-on-year volume drop. This resulted in an overall BEV market share of 3.8%, down 3.7pp compared with 12 months prior.

Despite this, Kia has refreshed its BEV catalogue for 2026. Since starting deliveries in March 2025, the Kia EV3 has enjoyed monthly triple-digit sales, ending up 14th in January. After one month on the market, the Kia EV4 shifted 58 units.

Geely breaks up BYD’s PHEV party

As with Australia’s BEV market, BYD provided the best-selling PHEVs in January. However, Geely disrupted a top-four clean sweep for the Chinese carmaker.

The BYD Shark continued an unbroken span of 12 months at the sales summit. A dominant presence was underpinned by consistent four-digit monthly volumes.

In January, the dual-cab pickup sold 1,108 units, according to EV Volumes. This ensured a healthy 37.8% share of the market.

A more established BYD model in the shape of the BYD Seal U, locally named the BYD Sealion 6*, claimed second . A total of 706 sales in January signalled a 63% increase in volumes year on year. This also ensured a 24.1% market share, down from 29.8%.

Mirroring the BEV table, Geely secured third place in the PHEV table. Sandwiched by four rival BYD models, the Geely Starray EM-i moved 305 units in January, securing a 10.4% market share.

The C-segment SUV has recorded strong monthly totals since it began recording volumes in Australia in September 2025.

Two BYD models, which only debuted in January, followed Geely’s Starray EM-i. In fourth place, the seven-seat BYD Sealion 8 recorded 247 sales, capturing 8.4% of the market. This was followed by the smaller Sealion 5 finished fifth, touted as the cheapest PHEV SUV available domestically, according to Driving Enthusiast. It accounted for 161 units and a 5.5% market share.

Established names lose market traction

BYD’s attractive price options are continuing to erode the appeal of more established carmakers in the Australian PHEV market.

The second most popular PHEV in 2024, the Mazda CX-60, ended up seventh in January. It saw a year-on-year volume dive of 52.3% with 62 units sold. Coupled with this, a market share of 2.1% resulted in a 7.8pp decline.

Similarly, 2023’s best-selling PHEV, the Mitsubishi Outlander, ended up sixth, with 64 new units sold. This ensured a sobering year-on-year volume drop of 59.7%, plus a dive in market share fell from 10.9% in January 2025 to just 2.2% one year later.

Rounding out the top 10, previously strong PHEV performers struggled in January. In eighth place, a 62.8% year-on-year sales decline for the MG eHS saw a market share slide of 8.3pp to just 1.9%. Meanwhile, the Lexus NX and Mitsubishi Eclipse Cross captured 0.6% of the market, respectively.

*Editor’s note: This article has been corrected since publication, with the BYD Sealion 6 the second best-selling PHEV in Australia, not the Seal 6 as previously stated.

How did the Chinese and European electric vehicle (EV) markets perform at the start of 2026? Plus, which manufacturers are speeding up plug-in vehicle charging? Tom Hooker, Autovista24 journalist, presents the latest episode of the Automotive Update.

In this episode, Autovista24 looks at the varying performances of the Chinese and European EV markets. Plus, how are carmakers speeding up EV charging? Also, an insight into which manufacturers are turning to robotics and AI for use in their production lines.

China’s EV market recorded a decline of 27.1% in January, according to the latest data from EV Volumes. Both the plug-in hybrid (PHEV) and battery-electric vehicle (BEV) sectors saw sales decline year on year.

The results were reflected in the best-seller tables, where mainstream models struggled. The Xiaomi YU7 was the leading BEV in January, with a dominant display. It was some way ahead of the second-placed Nio ES8. The Tesla Model Y finished third.

Meanwhile, the PHEV table saw BYD dominance slip away. Leading the charge was the Fang Chen Bao Tai 7, a BYD sub-brand and model. It was ahead of the Aito M7, while the BYD Song Pro finished third in the month.

Europe’s EV market on a high

Conversely, Europe’s EV sales grew, according to EV Volumes data. Sales were up 19.2% overall in January, with both BEVs and PHEVs seeing increases. PHEVs posted a 33.5% rise, while BEV deliveries increased by 12.7%.

The Skoda Elroq was Europe’s best-selling BEV in January. It was followed by the combined results of the Renault 5 and Alpine A290, with the Tesla Model Y in third.

In the PHEV market, two Chinese models led the way. The BYD Seal U came first, ahead of the Jaecoo J7. Both PHEVs were well ahead of the Volvo XC60 in third place.

Even faster battery charging

The Denza Z9GT, a model from BYD’s premium marque, is set to arrive in Europe later this year. It could enable quicker charging times of up to 12 minutes.

According to Denza, the Z9GT delivers a 10% to 70% charge in only five minutes, and a 10% to 97% refill in just nine minutes. The carmaker also quoted a 20% to 97% recharge in 12 minutes, even in temperatures around -30°C.

Meanwhile, Chery has revealed its all-solid-state battery that can achieve a range of over 1,500km, Electrek reported.

A robotic future?

Renault is using an AI-trained humanoid robot, called Calvin, to help it build cars. It was developed by French robotic firm Wandercraft. Renault plans to roll out a further 350 humanoid robots over the next 18 months, according to Auto Express.

This comes as carmakers increasingly identify automation and robotics investment as a key response to rising costs and competitive pressures. A recent survey by ABB robotics revealed that 31% of vehicle manufacturers and suppliers felt this way.

Electric vehicle (EV) sales in China dropped dramatically in January, as the market started 2026 with a struggle. But how did different brands influence this result? Autovista24 special content editor Phil Curry examines the numbers.

China’s EV market started 2026 in disarray. Battery-electric vehicle (BEV) and plug-in hybrid (PHEV) sales were down compared to January 2025, according to EV Volumes’ latest data. Additionally, the top 10 best-selling models for both markets were mixed, with newcomers spread throughout.

BEV deliveries fell by 20.4% in January, with 346,798 units reaching customers. This was the lowest total for the technology since February 2024. Meanwhile, PHEVs suffered an even steeper drop of 35.6% to 220,867 sales.

The country’s PHEV decline was a recurring theme throughout the last half of 2025. However, the drop in BEV volumes is new. This comes after sales growth slowed towards the end of 2025. The country’s market will be hoping January’s drop is not the start of an ongoing trend.

Mixed BEV results

The top 10 best-selling BEVs in China included five models that were not on sale in January 2025. To highlight the diverse mix, only one model from Tesla and BYD featured, respectively. Both brands appeared to struggle at the start of the year.

Even last year’s best-selling BEV in China, the Geely Geome Xingyuan, dropped deliveries compared to 12 months prior. Instead, a slew of newer models took advantage of the BEV market’s slowdown, entering the top 10.

The Xiaomi YU7 headed the Chinese BEV table in January. This model began recording sales volumes in June 2025. It achieved 37,924 deliveries in the month and gained a 10.9% market share. The YU7’s delivery figure was a record for a single BEV in January. Although the model itself achieved higher sales in December 2025.

The Nio ES8 achieved second with 18,513 units sold. The carmaker has ramped up deliveries, and January represented its third consecutive month of five-digit figures. Its market share jumped to 5.3%, up from just 0.1% a year prior.

Rounding out the top three was the Tesla Model Y. With 18,072 units, its sales declined by 29.7% compared to January 2025. This was also reflected in its market share, which dropped 0.7 percentage points (pp) to 5.2%.

Newcomers storm BEV chart

Since first recording sales in September 2025, the Li Auto I6 ended January in fourth with 16,876 sales. This equated to a 4.9% market share, a positive performance for a newcomer.

Last year’s best-selling Chinese BEV, the Geely Geome Xingyuan, ended January in fifth, with 14,887 deliveries. This was a 47.1% year-on-year decline, and the model’s lowest monthly sales since it started recording sales in September 2024.

Sixth went to the Aito M7, with 13,129 sales. This was a record amount and the model’s first foray into five digits since its launch in September last year.

With 6,772 deliveries, the combined total of the MG4 and MG4 Urban took seventh. These models were relaunched in the second half of 205 in China and achieved a 2% market share in January.

The only BYD model in the top 10 was the Dolphin, which saw sales increase by 25.9% to 5,859 units. Its 1.7% market share was up 0.6pp. Eighth went to the Wuling Bingo Plus with 5,632 deliveries, a 103.5% rise compared to January 2025. It achieved a 1.6% hold of the market, a full percentage point increase.

Rounding out the top 10 was the Toyota bZ3X. The Japanese model made its top 10 debut, just nine units behind the Wuling BEV. With 5,623 deliveries, it achieved an equal 1.6% market share.

Struggles for BYD and Tesla

Both Tesla and BYD have been staples of China’s BEV market, but January’s figures could suggest a difficult year ahead.

Although the Tesla Model Y placed well, its sales decline was the second successive January drop. Meanwhile, the US brand’s Model 3 ended the first month of 2026 in 43rd place, with just 2,030 units making their way to customers.

For BYD, its Seagull model, a constant BEV top 10 finisher last year, ended January 2026 in 11th. With just 5,525 sales, this was its worst monthly total since its first appearance in the Chinese market in April 2023. Meanwhile, the Yuan Up was 14th with 5,495 units. This also marked its worst volume since debuting in March 2024.

Looking at both brands’ EV sales, January was a poor month. BYD saw a 61.6% decline to 77,209 plug-in units, compared to 201,017 deliveries a year prior. Tesla saw 20,116 deliveries, all of which took place in the BEV market. This was a drop of 40.4% compared to the same period in 2025.

Fang Cheng Bao leads the way

BYD’s woes continued in the PHEV market, a sector it dominated in 2025. Last year, seven of the best-selling top 10 came from the Chinese carmaker. In January, however, just three made it to the chart, and none saw sales growth.

Instead, it was the carmaker’s sub-brand, Fang Cheng Bao, that took the top spot with the Tai 7. The SUV, which began mass deliveries in September 2025, has been slowly climbing the PHEV table. It dominated January’s chart with 17,553 units and a 7.9% market share.

Second went to the Aito M7, with 11,901 deliveries, a 41% rise year on year. This meant a 5.4% share of PHEV sales in China, up by 2.9pp.

The BYD Song Pro led PHEV sales for the brand in January. Its share sank by 0.7pp to 3.9% as it took third with 8,650 units. This was the model’s worst monthly total since July 2021.

The BYD Qin Plus was next, with 7,527 deliveries putting it fourth, with volumes down 49.8% year on year. This too was a new low, with deliveries not hitting these depths since January 2023.

Another new model, the Zeekr 9X, took fifth with 6,594 units and a 3% market share. The model started deliveries in September 2025.

Mixed results for PHEVs

The Aito M8 was the sixth-best-selling PHEV in China during January, with 5,316 units delivered. The model first recorded sales in April 2025.

Coming in behind was the Li Auto L6, with 5,030 sales. This was a year-on-year drop of 64%. The figure was the model’s lowest since it hit the market in April 2024. It was good enough for a 2.3% market share, down by 1.8pp compared to the same point last year.

The Aito M9 took eighth, the brand’s second appearance in the January top 10. However, its 4,821-unit tally was 47.5% down compared to January 2025. This meant its market share slipped by 0.5pp, to end the month at 2.2%.

The Wey Gaoshan came ninth. Having previously moved lower numbers, the model had a stronger end to 2025. It appears to have continued this run into 2026. With 4,813 sales, it managed a market share of 2.2%, up by 2.1pp.

Rounding out the top 10 was the BYD Seal 6 with 4,666 sales. This was a drop of 67.8% and was the model’s second consecutive month of four-digit deliveries. It was also its lowest volume since it first recorded sales in May 2024. Compared to 12 months prior, its share of the market was cut in half to 2.1%.

Europe’s electric vehicle (EV) market continued a trend of double-digit growth at the start of 2026. As plug-in hybrid (PHEV) sales soared, two Chinese brands enjoyed success in the region. Tom Hooker, Autovista24 journalist, breaks down the figures.

Both battery-electric vehicle (BEV) and PHEV sales enjoyed a strong start to 2026 in Europe, following a record-breaking 2025.

PHEVs recorded a 33.5% increase to 101,548 deliveries in January, according to EV Volumes. This was the first time the technology surpassed six-digit sales figures in the first month of the year. The result was in stark contrast to the PHEV market’s global performance, as it endured a 20.6% decline in the same period.

Yet this was still some way behind the 188,752-unit total accrued by BEVs. However, this did represent smaller growth of 12.7%. Combining the two technologies, overall EV sales in Europe grew by 19.2% in January to 290,300 units.

PHEVs’ share of Europe’s EV market increased to 35% in the month, up 3.8 percentage points (pp) year on year. In turn, BEVs took a 65% hold, down from 68.8%.

BYD and Jaecoo’s PHEV success

Two Chinese models shot out of the starting blocks in January, topping Europe’s PHEV market. First was the BYD Seal U, the continent’s 2025 best-seller. Second was the Jaecoo J7, which placed ninth in last year’s PHEV rankings.

The BYD SUV recorded 6,713 sales, giving it its third consecutive monthly first-place finish. Its total was up 261.9% from 12 months earlier, as its share rose 4.2pp to 6.6%.

Jaecoo’s J7 followed with 4,166 deliveries. The model has become a strong contender in the European PHEV market after deliveries began taking off in February 2025. Its share stood at 4.1% in January 2026, 0.5pp ahead of the nearest challenger.

Contrasting European PHEV fortunes

The Volvo XC60 was the first of three European models vying to shine domestically. The SUV led the sector 12 months ago, however, it started 2026 with a 26.4% sales decline. This equated to 3,619 units, handing it a 3.6% share, down from 6.5%.

Behind was the Volkswagen (VW) Tiguan, which took second place behind the BYD Seal U last year. Yet the Tiguan started 2026 with a 1.2% drop to 3,547 deliveries. Amid increasing competition, the PHEV’s share of overall volumes fell by 1.2 pp to 3.5%.

However, not all European PHEVs suffered a decline in January. The Mercedes-Benz GLC saw sales rise 75.9% to 3,475 units, securing fifth. It captured 3.4% of the market, up 0.8pp year on year.

PHEV shares slip

The Ford Kuga landed sixth with 3,089 sales. This represented a 4.6% increase on 12 months prior. Even so, its share slipped by 0.9pp to 3%. Seventh was the Hyundai Tucson after a 18% improvement to 2,806 deliveries. The SUV also suffered from increased competition, with its share falling by 0.3pp to 2.8%.

A similar story could be seen in eighth. The Toyota C-HR saw its slice of the PHEV market drop from 3.6% to 2.7%. Its volumes were stagnant from January 2025, down 1.3% to 2,726 units. Conversely, sales of the BMW X3 soared by 47.2%, ensuring a ninth-place finish. Its 2,697-unit total translated to a 2.7% share, up 0.3pp year on year.

The VW Golf came 10th, with an even greater increase of 81.2% to 2,558 sales. It made up 2.5% of total PHEV volumes, up 0.6pp from January 2025. The hatchback was the only non-SUV present in the PHEV top 10.

SUVs were not far off from filling out January’s top 10. Just seven units behind the VW Golf sat the BMW X1, followed by three further SUVs. This highlights how the body type is dominating PHEV sales in Europe.

Skoda’s strong start to 2026

Europe’s BEV best-sellers list featured a more diverse range of body types. Yet an SUV still led the way, as the Skoda Elroq returned to first place. 2025’s second-place finisher posted 8,146 sales in January. This gave the all-electric model a 4.3% share of Europe’s BEV market.

The combined deliveries of the Renault 5 and the Alpine A290 narrowly missed out on victory. Just 45 units behind the lead, the duo’s 8,101-unit total was up 75.5%, as its share soared from 2.8% to 4.3%.

Last year’s best-selling BEV in Europe, the Tesla Model Y, took third. Its 7,130 deliveries were up 21.2% compared to 12 months prior.

The crossover made up 3.8% of all-electric volumes, a 0.3pp improvement from January 2025. This was a good result considering its typical delivery pattern is weighted towards the end of the quarter.

Slowing sales for VW models

In fourth, the Skoda Enyaq was some way back from the leading trio. Its 5,475 deliveries were down 18.4% year on year, as its share slipped 1.1pp to 2.9%. The VW ID.3 was 70 units behind as its sales stagnated. The BEV recorded 5,405 units in January, down 0.3%. In turn, its hold fell by 0.3pp to 2.9%.

VW’s other ID models suffered poor results. The ID.7 managed sixth with 4,735 new models leaving dealerships. This translated to a 19.6% slump, while its share went from 3.5% to 2.5%.

The ID.4, which led the market 12 months previously, sat seventh in January 2026. It endured a 33.2% drop in sales to 4,541 units. The all-electric model took a 2.4% share, down 1.7pp year on year.

VW was not the only German brand to see declining deliveries. The BMW iX1 landed eighth after a 1.6% fall to 4,042 units. Meanwhile, the Audi Q4 e-tron suffered a greater drop of 12.1% to 4,002 sales. Both models recorded a 2.1% share, down from 2.5% and 2.7%, respectively.

The Citroen e-C3 took 10th with 3,671 deliveries. This was a 20.5% increase on 12 months prior, while its hold saw a marginal 0.1pp uptick to 1.9%. The Audi Q6 e-tron was 31 units back, narrowly missing out on making January’s top 10 table.

Global electric vehicle (EV) sales declined at the start of 2026. The plug-in hybrid vehicle (PHEV) market felt the largest drop, but did all models experience the same fall? Autovista24 editor Tom Geggus explores the numbers.

According to the latest data from EV Volumes, the global EV market fell by 9.5% year on year in January. In total, 1,156,731 PHEVs and battery-electric vehicles (BEVs) were sold in the new passenger car market.

Even with the inclusion of extended-range electric vehicles, PHEVs felt a sizeable drop, with 381,254 deliveries. This result was down by 20.6% from the figures recorded in January 2025. It marked a sizable downturn from the 1.6% growth recorded in December.

However, the powertrain only accounted for a third of the global EV market in January. BEVs made up the remaining 67%. The pure-electric powertrain recorded 775,477 sales, which equated to a year-on-year drop of 2.8%. This was the first BEV drop since February 2024, according to EV Volumes.

So, while the global PHEV market saw a larger fall, it made up a smaller proportion of the international EV market. However, in terms of units, there were 99,109 fewer PHEVs sold in January, but only 22,044 fewer BEVs. But did all models see similar declines?

Balanced fall of PHEV models

Of the top 10 best-selling PHEVs in January, five models recorded sales declines while the remainder enjoyed positive results. This confirms the rapidly changing face of the market, with new offerings challenging established players for dominance.

The Fang Cheng Bao Tai 7 saw sales first kick off in the third quarter of 2025. Since then, it has seen volumes accelerate, taking the lead of the global PHEV market. In total, the model recorded 17,553 deliveries, making up 4.6% of all the powertrain’s sales.

Exemplifying the market split, the BYD Song Plus, also known as the Seal U, saw its sales drop by 47.3%. These 13,293 units accounted for 3.5% of the global PHEV market, down from 5.2% in January 2025.

Another more established leader, the BYD Song Pro, recorded a delivery decline of 39.5%. Its 12,590 sales made up 3.3% of all PHEV sales, down from 4.3% in January 2025, putting it in third.

New PHEV challenge

The Aito M7 saw a sales uptick of 41% to 11,901 units in fourth. This meant its market share increased by 1.3 percentage points (pp) to 3.1%. Behind it, the BYD Qin Plus recorded a 47.4% sales drop, with 8,353 units moved. Its share fell by 1.1pp to 2.2%.

In sixth, the Zeekr 9X captured 1.7% of the global PHEV market with 6,602 units sold. With deliveries commencing in September last year, this confirms a steep upward curve in buyer interest.

Seventh went to the BYD Seal 06. Its 6,405 sales equated to a 57.3% decline from January 2025. This pushed its market share down from 3.1% to 1.7%. Behind it, the Jaecoo J7 saw its share grow by 1.1pp to 1.5%. This was thanks to a 208.8% increase in demand to 5,802 units.

Ninth went to the Volvo XC60 as its share only slid by 0.1pp to 1.4%. However, its sales slumped by 25.1% year on year to 5,362 units. With 5,316 sales, the Aito M8 was in hot pursuit, taking 1.4% of the market as well. The chief difference is that the M8 first recorded sales in April 2025, while the Volvo XC60 is a familiar market presence.

New BEVs racing to top

The global BEV market was led by a familiar model at the start of this year. The Tesla Model Y recorded 54,786 deliveries, down by 11.2% year on year. This meant its hold on the market weakened by 0.6pp to 7.1%.

The Xiaomi YU7, which first recorded sales in June 2025, saw 37,956 units delivered, equating to a 4.9% share. The Nio ES8, also known as the EL8, represented 2.4% of all BEV volumes with 18,558 units. Following the launch of its third generation in September last year, it has seen sales climb.

The BYD Seagull, also known as the Dolphin Surf, came fourth in the month with 17,448 sales. This was down 19.6% on January 2025 as its share hit 2.2%, down 0.5pp. After first recording sales in September last year, the Li Auto I6 finished fifth with 16,876 units moved. It accounted for 2.2% of all BEVs sold.

The Tesla Model 3 came next as it moved 16,535 units, down 35%. Its market share dropped to 2.1% from 3.2% a year ago. The Geely Geome Xingyuan, also known as the EX2, finished seventh. Its sales declined by 41.6% to 16,442 units, capturing 2.1% of the market, down 1.4pp.

The BYD Dolphin finished eighth with 15,812 sales, up 60.3%, allowing it to increase its stake to 2% from 1.2%. After first recording sales in September 2025, the Aito M7 reached 13,129 sales in January, equating to a 1.7% share.

The BYD Yuan Up, also known as the Atto 2, came 10th. Its sales fell by 29.1% year on year to 11,702 units. This gave it a 1.5% share, down from 2.1% a year earlier.

The UK’s zero-emission vehicle (ZEV) mandate is scheduled for review. But with other countries amending their policies, will the UK’s targets be amended sooner, or later? Autovista24 special content editor Phil Curry reports on SMMT Electrified 2026.

The UK automotive industry needs a review of the ZEV mandate, otherwise it could fall behind in the electrification race. That was the main message from the recent SMMT Electrified conference.

Held in London’s QEII Centre, the event brought together automotive industry executives, regulators and suppliers. They discussed the current state of the UK’s electric vehicle (EV) market.

The conference followed shifting emissions policies in Europe and the dropping of mandated targets in Canada. Meanwhile, the UK Government remains committed to the ZEV mandate. This is despite overall battery-electric vehicle (BEV) registrations failing to meet the 2024 or 2025 targets.

The cost of reaching targets

The ZEV mandate calls on carmakers to meet an increasing share target of zero-emission models in their annual registrations. It first came into effect in 2024, with a 22% requirement for passenger cars. This increased to 28% for 2025, while the target is 33% next year.

This increases annually, reaching 80% by 2030. However, the biggest jump in the requirement comes between 2027 and 2028, with a 14 percentage point rise in the target, to 52%.

The Department for Transport (DfT) released a report on the morning of the conference. It highlighted that all carmakers had complied with the ZEV mandate in 2024. Manufacturers had used conversion flexibility, while also borrowing future credits, with some banked for future years.

However, SMMT chief executive Mike Hawes highlighted the costs that the industry faced in meeting ZEV mandate targets.

‘Non-compliance is not an option, but compliance comes at a massive cost,’ he told journalists, including Autovista24, during a press conference prior to the event. ‘In the first two years of the mandate, carmakers have spent up to £10 billion (€11.6 billion) in discounting on BEVs. That is in addition to the billions spent on new products, new technologies, and so forth.

SMMT chief executive Mike Hawes

‘In 2025, the average discount on a BEV model was £11,000. However, the payment for non-compliance to the ZEV mandate is £12,000 per model. Compliance comes with a tremendous cost, either in incentives, fines, or the need to purchase trading credits.

‘Therefore, while the DfT report shows that carmakers have met the requirements of the mandate in 2024, compliance does not necessarily mean that the mandate is deliverable,’ he stated.

Further ZEV mandate challenges

One issue impacting BEV uptake appears to be costs for consumers. The technology has long been touted as a more affordable alternative to petrol and diesel in terms of use.

However, there is often a cost difference between charging domestically and using public plug-in points. In addition, the implementation of vehicle excise duty (VED) last year increased costs.

A pay-per-mile scheme, known as eVED, for BEVs and plug-in hybrids was also announced in 2026. This is set to be introduced in 2028, at a point when the ZEV mandate target is set to jump. For carmakers, this could be a problem. The affordability of BEVs will be reduced, but the requirement for carmakers will leap forward.

‘Additionally, the flexibilities introduced last year will expire from 2029,’ added Hawes. ‘I do not know of anyone in the industry who thinks we will get to 80% of ZEVs by 2030. Beyond that, we still have a lack of clarity.

‘We have neither the regulation nor the certainty about exactly which technologies can be sold. But what we do know is the gap between ambition and demand is too great. The UK’s attractiveness, not just as a market, but as a manufacturing location, evaporates. De-carbonisation, if we get this wrong, can mean de-industrialisation.’

Good intentions of the ZEV mandate

Hawes stated that the UK’s automotive industry is committed to reducing emissions and working towards net-zero. ‘But sometimes, to reach a destination, you have to take a diversion. When the facts change, you have to adapt,’ he continued.

‘When the ZEV mandate was conceived, the world was a different place,’ Hawes stated. In line with statistics published by the SMMT during the event, he outlined that battery costs were 30% higher in 2025 than anticipated in 2021. Meanwhile, BEVs were 17% more expensive within the same timeframe.

In addition, industrial energy costs were 80% higher than expected, Hawes stated. The costs of public EV charging at 50kW points were 120% higher than thought when the ZEV mandate was first discussed, he added.

‘We need it reviewed now and resolved now. Without change, the sector, the economy, mobility and decarbonisation itself are in jeopardy. So, government needs to be bold enough to lead the change to make sure that we have a system that is fit for the future,’ he concluded.

Carmakers back early review

The ZEV mandate issue remained a constant throughout SMMT Electrified 2026. Carmakers in attendance also backed the need for a review of the current strategy.

‘The ZEV mandate needs to be more aligned to where consumer demand is. Investment is so heavy in the market, then some of the vehicles sold will be loss-making. If you are in that scenario, and you are forced to increase supply as the ZEV mandate does, then that calls investments into question,’ highlighted Eurig Druce, SVP, group managing director at Stellantis UK.

‘If you cannot make a return on investment in a country, then the ability of a company to invest and create the growth that the government is looking for is absent. Therefore, we need to make some quick decisions, and a review next year is too late. We need a review now, to help us make the right decisions on investments,’ he continued.

From left to right: Patrick McGillycuddy, managing director at JLR UK, Richard Finchett, deputy managing director at Toyota Manufacturing UK, Nicole Melillo Shaw, Managing Director at Volvo Car UK, Eurig Druce, SVP, group managing director at Stellantis UK

But while development of BEVs continues, the route of discounting is not one that carmakers want to be going down.

‘We put a lot of investment into developing and building the advanced technology in BEVs. The last thing anyone wants to do is bring out a car with that much investment, and then start discounting from the beginning. It is unsustainable. So I think we need to make sure that we are allowing for demand to catch up with supply,’ pointed out Nicole Melillo Shaw, managing director at Volvo Cars UK.

A different approach

Patrick McGillyCuddy, managing director at JLR UK, further underlined the issue of confusion among consumers. ‘We have a very ambitious ZEV mandate, and then we have the eVED, which is proposed to come at a critical time in that journey,’ he said.

‘This causes confusion, and consumers will hesitate. Then we hesitate, and you get an uncertain environment. We produce most of our vehicles in the UK for global export, therefore we have to recognise that different parts of the world are moving at a different pace,’ he added.

Ford Motor Company chair and managing director, Lisa Brankin, also brought up the issue during a candid fireside chat.

‘When it comes to a review, the government needs to consider the customer in two areas. They need to knock down the barriers to entry, but also understand and prevent confusing messages.

‘Last year, for example, we had the launch of the Electric Car Grant incentive scheme. That helped drive sales forward. But a few months later, there was the announcement of eVED. The two messages did not align, so the government really needs to be mindful of what it is saying if the end goal is electrification,’ she said.

Failure from success

Brankin also highlighted how the ZEV mandate directed focus away from Ford’s achievements in 2025. Instead, it suggested failure in the company’s performance, she explained.

From left to right: Lisa Brankin, chair and managing director, Ford Motor Company, Katie Derham, host and broadcaster

‘Our sales grew by 20% in 2025, which was a great success. But we count it as a failure as we got to just under 24% of the fleet being ZEVs, when the target in the mandate was 28%. We are moving in the right direction, but not meeting targets,’ she stated

‘We have invested heavily in our facilities in Europe to build EVs, but we are having to discount heavily to meet targets. We may also be forcing people into vehicles that maybe they do not necessarily want, or maybe are not appropriate for them,’ she said.

Brankin also pointed to the changes in other ZEV policies that have taken place around the world. ‘Canada has made a change, and our closest partners in the EU have already made adjustments. That was carried out in a matter of months rather than over a longer period. So, I would say to the UK government to get on with it, start the review, decide, and make the announcement this year,’ she continued.

Government committed to 2027 ZEV mandate review

Taking to the stage at SMMT Electrified 2026, Keir Mather MP, minister for Aviation, Maritime and Decarbonisation, spoke of the success of the UK’s EV market. He highlighted that the country had the largest BEV share of Europe’s major economies, as a result of ambition, partnership and investment.

Autovista24 analysis shows that in 2025, the UK saw its BEV share reach 23.9%, with 473,348 units. While this share was higher than the 19.1% achieved in the closest market, Germany, the volume of BEVs was lower. In 2025, the country saw 545,142 units delivered.

Mather also stated that the EV transition in the UK is being backed by tens of billions of pounds in public and private investment. But he acknowledged that the ZEV mandate is potentially a challenge for the industry.

‘Is [the ZEV mandate] ambitious? Yes, of course it is, and we as government are committed to giving you the tools you need to make it happen. The industry successfully complied with the 2024 target, using the flexibilities built into the mandate, and provisional 2025 data also looks promising,’ he commented.

‘We are committed to publish a review of the mandate early in 2027, and we are listening, and we are engaging with stakeholders across the industry.’

When asked about the potential for an early review, as called for throughout the conference, Mather stated: ‘Work on the review needs to begin this year. But early 2027, we feel, is the right point to make sure that we can see properly where the pressure points lie in this ZEV mandate and make sure that it continues to work for manufacturers.’

What were the key talking points from SMMT Electrified 2026? Plus, a look at Renault’s new strategy and major robotaxi collaborations. Autovista24 editor Tom Geggus presents the latest Automotive Update podcast.

Autovista24 special content editor Phil Curry joins the Automotive Update from SMMT Electrified 2026 in London. Plus, a dive into Renault Group’s plan to drive growth in the run up to 2030. Also, a look at which companies will work with Wayve on new autonomous vehicle technology.

SMMT Electrified 2026 focuses on the UK automotive industry’s transition to electric vehicles (EVs) and other zero-emission technologies.

Among a wide range of topics, this year’s event focused in on key policies that could shape EV production and demand in the UK. This included the ZEV mandate, which SMMT chief executive Mike Hawes said requires an ‘urgent review.’ This is due to the domestic EV market not reaching its full growth potential, he explained.

Subsequently, industry figures called for further ZEV mandate clarity at the event. Patrick McGillycuddy, managing director at JLR UK, highlighted customer confusion. This uncertainty has been exacerbated by the looming pay-per-mile EV charge. Meanwhile, Lisa Brankin, Ford UK chair and managing director, pointed out that carmakers are facing challenges in meeting the ZEV target.

Renault’s new era

Renault Group has announced ‘futuREady’, its new strategic plan. Central to the initiative is an aim to sell over two million cars by 2030. These targets will be enabled by the launch of 36 new models.

In Europe, the Renault brand will launch 12 models spanning the A and B segments, as well as new models in the C and D segments. International markets will see 14 new vehicles launched by the brand between now and 2030.

Elsewhere within Renault Group, Dacia plans to electrify two-thirds of its sales in 2030. The brand will also look to increase the number of EVs in its range from one to four. Meanwhile, Alpine will launch the next generation of its A110, as well as building on the A290 and the A390.

François Provost, CEO of Renault Group, stated: ‘futuREady, our new strategic plan, is a crucial step in the future of Renault Group. In an environment that is even more competitive, we can build on solid fundamentals: our brands, our products and our financial results.’

Wayve hello to new autonomous collaborations

UK-based autonomous driving company Wayve has announced a new robotaxi collaboration with Uber and Nissan. The trio hope to launch a pilot in Tokyo later this year. The project will integrate Wayve’s AI autonomous driving system into a Nissan base vehicle. This will then be connected with Uber’s ride-hailing platform.

Elsewhere, Wayve will also work with Qualcomm on a pre-integrated advanced driver-assistance and automated driving system for carmakers. This will provide support for entry-level hands-off driving assistance, as well as for eyes-off automated driving.

As increased carmaker competition starts to make waves in Italy’s new-car market, February’s data revealed a strong start to 2026. But which brands and powertrains are pushing things forward, and can this relative prosperity continue? James Roberts, Autovista24 web editor, finds out.

In February, 157,317 new cars were registered in Italy. This resulted in a year-on-year volume increase of 14.1%, according to ANFIA data. This ensured a third month of consecutive growth.

Across the first two months of 2026, a total of 299,308 new cars took to Italy’s roads. This marked a 10.2% lift, helped by a strong showing from electrified powertrains. Despite volumes remaining below pre-COVID-19 pandemic levels, the market shows promise following a difficult 2025.

EV sales prove strong in February

February saw 25,151 new EVs, including battery-electric vehicles (BEVs) and plug-in hybrids (PHEVs), registered in Italy. This resulted in a significant 91.5% year-on-year uptick.

There was little to split BEV and PHEV popularity in February. All-electric sales amounted to 12,541 units, while PHEVs accounted for 12,610 vehicles. Both powertrains captured 8% of the monthly market share, respectively.

It was PHEVs that saw the biggest year-on-year volume increase, with 102.8% compared to February 2025. However, BEVs were not far behind, with a volume improvement of 81.3%.

In the year to date, plug-in hybrids took a larger market share of 8.1%, up 4 percentage points (pp). This was accompanied by a 116.7% boost in registrations across January and February. BEVs, meanwhile, accounted for 7.3% of the market, a 2.3pp increase, with a 61.3% upswing.

Combined, EV registrations in Italy made up 16% of the market two months into the year, a 6.5pp improvement.

Italy’s EV popularity running on fumes?

On the face of it, the year-on-year EV volume gains appear satisfying. However, February’s figures continued to be raised by the incentive programme rolled out in late 2025. All funds were claimed within 24 hours of the scheme going live, with consumers needing to apply before purchase. This influenced January and February’s latent EV bounce.

For some industry observers, this is not enough to signal a meaningful tilt towards electrification targets. To continue EV market ascendency, and match larger European markets, wider, more sustained policy initiatives are being called for.

‘Electric [uptake] is growing, but we are still far from the averages of the large markets,’ outlined Roberto Pietrantonio, president of UNRAE. ‘Without a structural and stable strategy, Italy will lose competitiveness and appeal. Those who talk about the failure of the electric sector feed misinformation. The real challenge is to govern the transition with industrial vision and reform courage.’

UNRAE recommended three measures aimed at fostering a more robust path towards electrification. These included improving EV charging infrastructure network as well as hydrogen refuelling. Second, charging tariffs should be more consistent with wholesale energy prices. Third, structural reform of company fleet taxation, which is a major complicating factor for businesses.

Cost deductibility, VAT deductibility, and less favourable depreciation rules mean Italy lags behind other major European markets, according to UNRAE. The organisation claimed that reforming these tax policies could encourage companies to renew and electrify fleets. This in turn would speed up the adoption of low and zero-emission vehicles.

‘Clarity is needed,’ UNRAE added. ‘Decarbonisation remains the goal, what is missing is regulatory stability and a multi-year strategy, as in the main European countries, to offer families and businesses a credible horizon.’

Italy’s market disruption

Amid February’s relatively strong plug-in demand, one newcomer stormed into the top 10 best-selling model chart: the Leapmotor T03. This small urban BEV shook up the top 10 in February with 4,778 sales, confirmed by ANFIA data. Taking fourth in the month, the T03 sat just behind three top-selling models from the Stellantis stable.

Across the first two months of this year, the all-electric model saw 5,727 units delivered to customers. This pushed it to seventh in the overall top 10, ahead of the Renault Clio, the Renault Captur, and the Toyota Yaris.

More broadly, Leapmotor enjoyed a 2197.2% year-on-year registration increase in February. This meant that it jumped from 218 unit deliveries in February 2025 to 5,008 one year later. This year, the Chinese OEM‘s lineup in the country will include the T03, the C10 and the B10.

Last year, Leapmotor CEO Zhu Jiangming targeted global sales of one million units in 2026, Reuters reported. On top of this, he eyed four million annual transactions within a decade, with 60% coming from outside of China. It seems Italy is doing its bit to help achieve this goal.

Non-domestic brand disruption continues

As well as Leapmotor’s increased market influence, other non-European OEMs have started to make considerable waves in Italy.

Following a strong start to the year, BYD saw another month of Italian new-car market gains. The Chinese manufacturer recorded 4,110 registrations in February. This was up from 1,349 sales one year prior, ensuring a 204.7% boost.

Chery has emerged as a notable disruptor in Italy as well. Its Omoda brand enjoyed a 960.9% rise in registrations, leaping from 523 units in February 2025 to 2,960 one year later. Meanwhile, its sister brand, Jaecoo, saw deliveries increase by 266% with 893 cars sold.

Italy’s hybrid domination prevails

February saw hybrids account for over half the country’s new-car market. In all, 81,799 units, spanning full and mild versions, left forecourts. This considerable year-on-year volume increase of 33.9% as the powertrain took a 52% market share, up 7.6pp.

This dominance was reflected two months into 2026 with 156,215 hybrids joining Italy’s car parc, enabling a 52.2% share. This suggests that hybrid popularity remains prevalent, with EVs struggling to make a dent.

Continued hybrid appeal has pushed up the share of electrified registrations in Italy’s new-car market. Adding hybrid volumes to BEV and PHEV totals amounted to 202,427 vehicles across the first two months of the year. This underlined a year-on-year leap of 39.2%.

It also provided electrified vehicles with 67.6% of the overall Italian new-car market. This was a considerable 14pp lift compared with the first two months of 2025. Hybrid figures have been the vanguard of this seismic demand for electrified powertrains so far in 2026. Removing hybrids from the electrified figures drops the share to just 32.3%.

ICE drops but petrol still second best

Internal-combustion engine (ICE) deliveries, including petrol and diesel volumes, continued a pattern of double-digit declines in February. The 42,518 combined sales meant a 14.7% fall and a 27% market share, down 9.1pp. Across January and February, this was reflected in an 18.8% slump and a 36.2% market share. However, despite this continued slide, petrol preference remains a key market force.

Despite a 6.9pp year-on-year decline across January and February, petrol held the second-highest market share in Italy at 19.6%. The petrol share was 11.5pp ahead of PHEVs, and 12.3pp above BEVs, providing a further headache for electrification targets.

As petrol peters out, diesel continues to fall drastically. February saw 10,603 new diesel vehicles reach customers in Italy. This signalled a 22.5% year-on-year unit drop, leaving the fuel type with a 6.7% market share, down 3.2pp.

Including January and February’s figures, diesel sales reached 21,336. This returned a year-on-year volume slide of 19.5% and a market share of 7.1%, down 2.7pp. Despite this, cumulative diesel registrations trailed BEV sales by just 627 after the opening two months of 2026.