When it comes to P2P (person-to-person) transfers, bank customers are fiercely loyal to the brand they prefer. However, according to new JD Power data, network effects, security and ease of use play a large role in determining which “additional” brands consumers are using.

This Payments Intelligence Report dives into the findings of the JD Power 2025 U.S. P2P Transfers Satisfaction Study to spotlight the prevailing sentiment and emerging trends in P2P transfer customer experience.

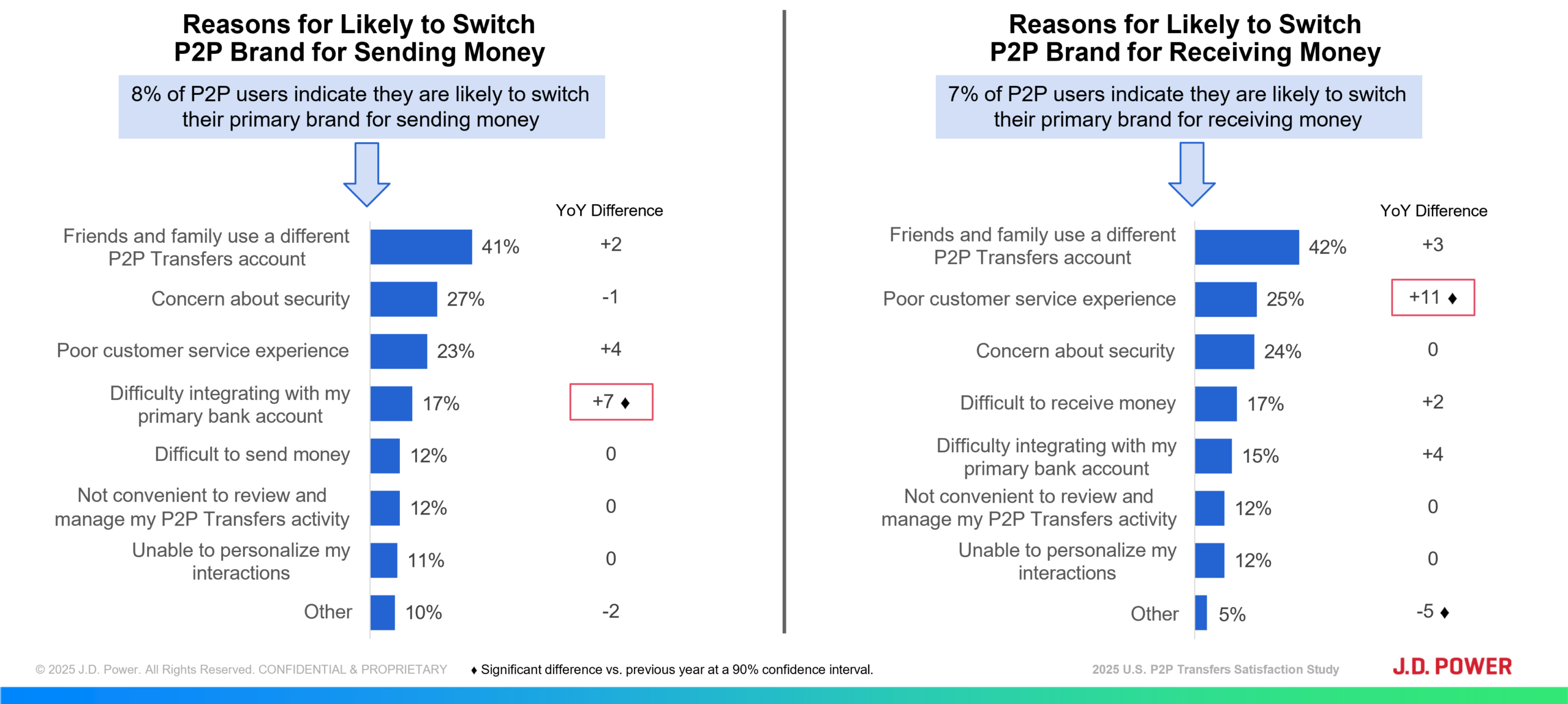

Customers Prefer Adding Over Switching

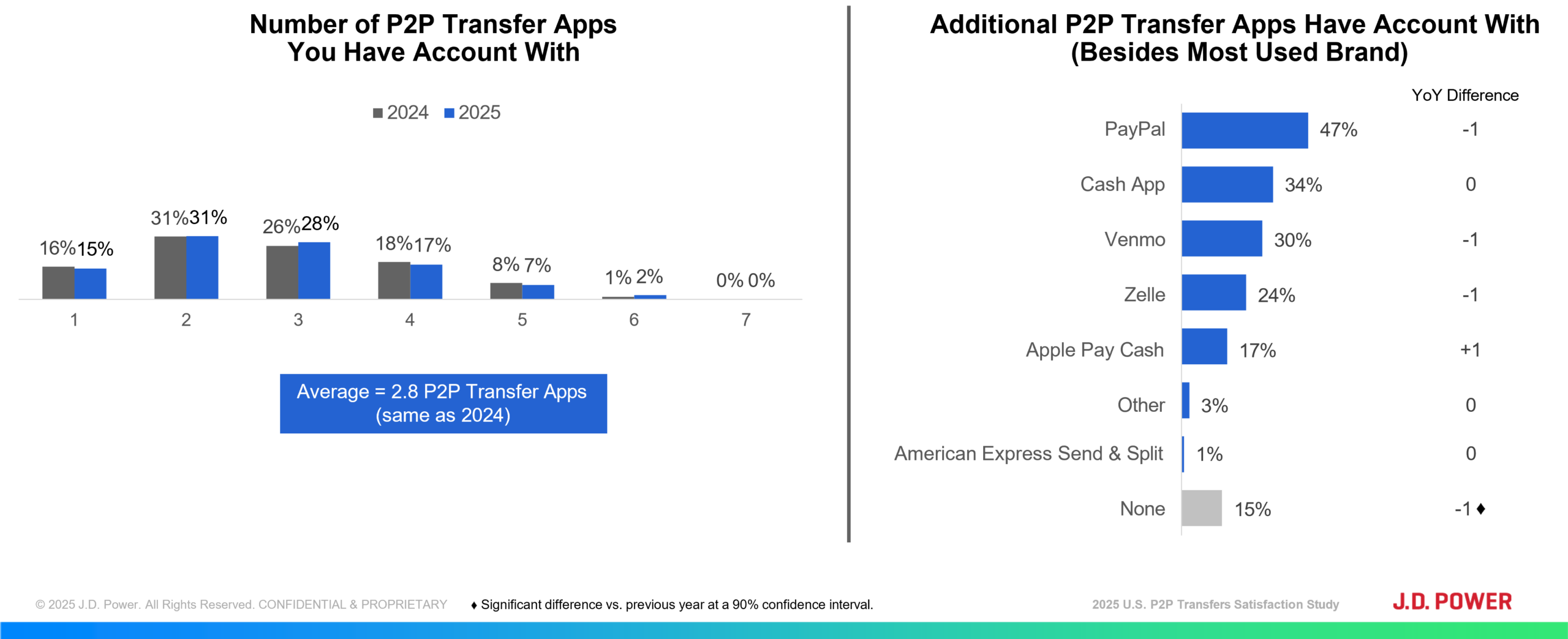

Most customers say they do not intend to switch using their primary P2P brand, but most also use more than one brand, indicating openings exist for providers to grab more market share. The average P2P user has accounts with 2.8 brands, with PayPal being the most common additional brand. Overall, 47% of P2P users have a secondary account with PayPal.

Customers Want Ease of Use, Security

Customers say the most likely reason to switch P2P brands for both sending and receiving money is family and friends using a different P2P transfer account (41%). Security concerns (27% for sending money, 25% for receiving) were also among the top reasons.

Brands using the Zelle network continue their dominance over industry peers. For a second consecutive year, among the top eight performing brands in the study, seven are part of the Zelle network. They are (in alphabetical order): Bank of America, Capital One, Chase, PNC, Truist, U.S. Bank and Wells Fargo.

That said, how banks integrate Zelle into their mobile and electronic platforms has a large effect on satisfaction. Zelle integration is largely customizable, so how and where Zelle’s features appear in each bank’s tool vary.

Capital One’s P2P customer experience, for example, is enhanced by strong discoverability from the home screen, a pay/move screen featuring a Zelle-centric money movement experience, and a final send screen that displays the recipient’s information to reconfirm money is being sent to the right person.

Breaking Through

While P2P users are steadfastly loyal to their primary brand, competing providers have a real opportunity to expand their customer base by turning existing users into advocates. Many users are receptive to opening secondary accounts to ensure they can send money across their entire social network. This means an incumbent—or even a new disruptor—doesn’t need to break brand loyalty to make meaningful gains. Sometimes, all it takes is one friend or family member requesting a transfer via another service, and suddenly, that competitor has gained a new user.

As brands build out their platforms, it is incumbent on them to understand what differentiates the top performers.

Find out More

This Payments Intelligence Report is based on responses from the JD Power 2025 U.S. P2P Transfers Servicer Satisfaction Study, which included 6,105 responses and was fielded from January to March 2025. It is authored by Sean Gelles, Senior Director, Payments Intelligence. Please contact us at the numbers below to connect with Mr. Gelles or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]