Insights

Vehicle Configuration Complexity and Strong Used-Vehicle Market Wreak Havoc on Auto Insurance Valuation Models and Carrier Profitability

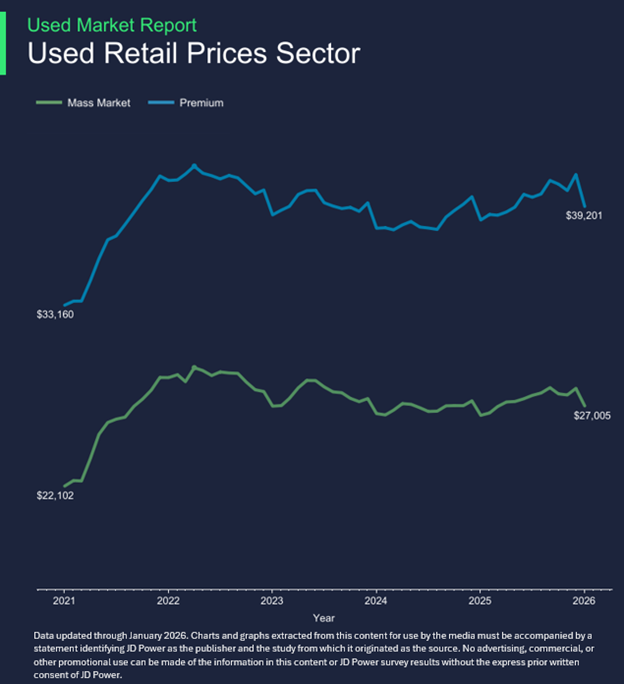

Vehicle configuration complexity has increased exponentially over the last 10 years, primarily driven by a shift from mechanical systems to "software-defined" architectures, with over 600,000 unique vehicle configurations sold in North America in the 2025 model yearAverage used-vehicle retail prices have risen 20% in the past five yearsAuto insurance actuarial models built on incomplete vehicle identification data could be off by upwards of $15,000 per vehicle Henry Ford famously said that customers “could have a Model T in any color they want—so long as it was black.” Today’s automotive market could not be more different. Vehicle customization has exploded over the past decade as automakers compete to meet increasingly specific consumer preferences. For example, in the large pickup truck segment, the Ford F-150 currently has upwards of 100,000 unique build configurations and, market-wide, more than 600,000 unique vehicle configurations were sold in the United States in the last year alone, according to JD Power data.While this level of customization has benefited consumers and automakers, it has created a growing challenge for auto insurers. Many actuarial models used to price and underwrite policies still rely on simplified vehicle identification data that cannot fully capture the configuration and replacement value of modern vehicles. At the same time, volatility in used-vehicle pricing and rising repair costs are further complicating valuation models that were built for a far more predictable market.This combination of vehicle complexity and market volatility is creating a widening gap between the values insurers assume during underwriting and the costs they ultimately face when repairing or replacing vehicles after a claim.This Insurance Intelligence Report explores key data points gathered from JD Power studies and proprietary market data to offer a data-driven perspective on the current state of insurance industry vehicle valuations. Widespread MSRP Variability Within the Same TrimOne of the most significant challenges insurers face today is the dramatic variability in vehicle pricing—even among vehicles that appear nearly identical on the surface. Automakers now offer a wide range of factory-installed options, packages and custom features that can dramatically affect a vehicle’s price. From advanced driver assistance systems (ADAS) and upgraded powertrains to premium interiors and specialty paint packages, two vehicles with the same year, make, model and trim can have vastly different original values.For example, a 2024 Ford F-150 Lariat 4WD SuperCrew with a 5.5-foot bed could have been sold for approximately $69,630 with standard options, while a fully optioned version of the same vehicle could reach $84,465, according to JD Power data. For insurers, this creates a consequential underwriting blind spot. Unless they have access to the full 17-digit vehicle identification number (VIN) and the corresponding OEM build data tied to that VIN, they may not know which configuration they are actually insuring—creating up to $14,835 in unknown price variability.Many insurers rely on a shortened VIN identifier—often referred to as a “squish VIN”—when building underwriting models or quoting policies. While this truncated VIN provides basic information such as year, make, model, and sometimes trim level, it lacks the detailed configuration data needed to accurately assess a vehicle’s full replacement value.As vehicle configuration complexity continues to increase, reliance on simplified vehicle identification methods can introduce significant pricing inaccuracies into underwriting models.The Great Used Vehicle Price ResetVehicle complexity is only part of the challenge. The used-vehicle market has also undergone significant structural changes over the past several years.The average used-vehicle retail price is now $29,488, reflecting a more than 20% increase over the past five years, according to JD Power data. Much of this increase can be traced to supply shortages caused by pandemic-era production disruptions, which limited the availability of late-model used vehicles entering the market. For insurers, this volatility creates another modeling challenge. Traditional valuation models have long relied on the assumption that most mass-market vehicles depreciate roughly 20% per year. However, recent market dynamics have disrupted those historical depreciation patterns.Take the earlier example of the 2024 Ford F-150. Today, that vehicle is worth approximately $50,965, representing a 28% decline from its original MSRP. Under traditional depreciation models, insurers might have estimated the vehicle’s current replacement value at roughly $55,165, resulting in a $4,200 gap between projected and actual value. EV’s are further complicating traditional valuation models as EVs are projected to lose 59% of their value over five years, compared to an industry average of 46% for all vehicle types, according to JD Power data.Across millions of insured vehicles, valuation discrepancies like this can meaningfully impact claims severity and insurer profitability. More Tech, More ProblemsAnother major factor complicating insurance valuation models is the rapid expansion of vehicle technology. Modern vehicles increasingly include ADAS such as automatic emergency braking, adaptive cruise control, lane-keeping assistance and collision avoidance technologies. While these features improve safety and help reduce the likelihood of severe accidents, they can significantly increase repair costs when collisions occur.Sensors, cameras and radar modules are often embedded in bumpers, mirrors, windshields and body panels. Even minor accidents can require expensive sensor replacements and complex recalibration procedures.Accurately modeling this risk requires insurers to know precisely which safety technologies are installed on each vehicle they insure. Without accurate, detailed VIN-level configuration data, insurers may not have visibility into which vehicles contain these systems and which do not—introducing further uncertainty into repair cost projections. AI TransformationAs insurers increasingly adopt AI-driven underwriting, claims automation and pricing optimization tools, the importance of accurate foundational data becomes even greater. Artificial intelligence models are only as effective as the data used to train them. Without precise vehicle configuration and valuation inputs, AI systems risk amplifying inaccuracies rather than improving decision-making.Insurers that modernize their vehicle data infrastructure will be better positioned to price risk accurately, control claims severity and maintain profitability in an increasingly complex automotive landscape. Cracking the CodeWith the average new-vehicle transaction price now exceeding $46,000, insurers should expect continued upward pressure on vehicle repair and replacement costs. However, rising costs do not necessarily mean insurers must accept greater pricing uncertainty.Insurance has always been about accurately measuring and pricing risk. In today’s competitive environment, doing so requires more precise data about the vehicles being insured.As vehicle complexity has accelerated, insurers need to be able to track more detail than what’s currently available in “squish vin” datasets. Access to full 17-digit VIN configuration data, OEM build information, real-time vehicle valuation insights and feature-level vehicle attributes can help insurers build more accurate underwriting models, improve claims severity forecasting and better align pricing with actual risk. What Lies AheadFor an insurer, moving from generic VIN decoding to precise, configuration-level data transforms the business from reactive to surgical. As vehicles have become "computers on wheels," with significant price variations, knowing the exact build data—not just the year, make, and model—is the difference between profitability and a loss ratio spike.After years of record rate increases and now that pricing issues have been resolved, auto insurance carriers are pulling out all the stops to grow. By shifting from broad vehicle categories to precise, VIN-level configuration data, insurers are gaining the pricing confidence needed to aggressively target new growth opportunities by selling to a broader set of consumers with varying degrees of risk. Find out MoreThis Insurance Intelligence Report was authored by James Vecchio, Head of VIN Products at JD Power. The analysis draws on JD Power studies, proprietary market data, and VIN‑level configuration and valuation intelligence, including insights derived from the JD Power StudyPrice 2.0 tool, which decodes the full 17‑digit VIN to reflect a vehicle’s exact build profile.JD Power Specialty Vehicles provides P&C insurance carriers with advanced decoding and valuation products for powersports, marine, recreational vehicles, classic cars, commercial trucks, and manufactured housing. Available via subscription, our data is the most accurate and robust in these industries—trusted by more than 90% of the market.To learn more about the research, underlying methodology, or vehicle valuation capabilities available to insurers, please contact the JD Power Insurance Intelligence team.Media ContactsBrian Jaklitsch; East Coast; 631-584-2200; [email protected] LaMuraglia, JD Power; East Coast; 714-621-6224; [email protected]