Key Insights

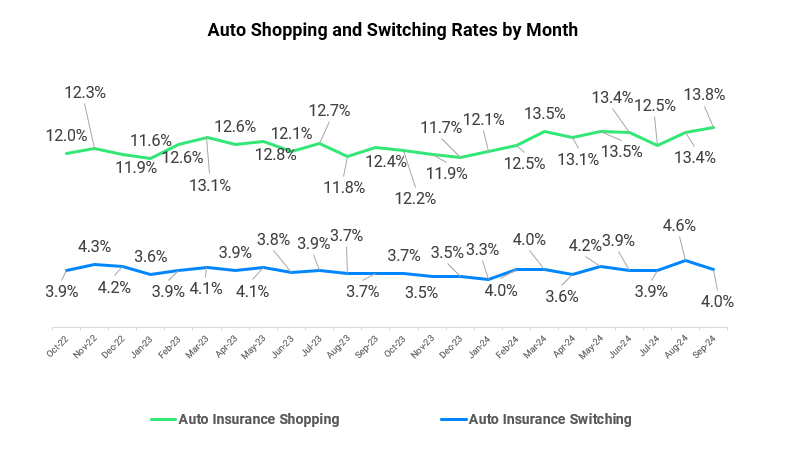

- Effects of rate increases hit critical mass: The percentage of customers who shopped for auto insurance hit record-high levels at 57% in 2025, up from 49% in 2024. However, unlike past years – when switching lagged shopping – customers are finding better prices in the market, which will put further pressure on insurers in 2026.

- High-value customer retention a top priority: Driven by premium hikes, insurers are starting to finally see customer attrition among their most valuable customers – those who are more likely to bundle products and have high rates of loyalty. With price volatility likely to remain a factor in 2026, insurers must find ways to focus their efforts on retaining these customers.

- Digital channels and technology offer key insights: Use of digital channels and technology are vital to customer satisfaction. Overall, 47% of all insurance policy buyers now purchase through digital channels, and customers are forming new habits and opinions in their use of tech, which provides an opportunity for insurers to tailor their offerings.

Executive Summary

Sky-high policy rates have finally changed the game. After five years of unprecedented volatility, insurers are beginning to see the consequences of gradual, but consistent premium hikes. Faced with bigger bills, customers have come to expect more from their insurers. Now more than ever, insurers that fail to provide compelling offers to customers will send them rushing into the waiting arms of a company that will.

This Insurance Intelligence Report dives into key data points gathered from JD Power Insurance Intelligence studies and proprietary market data to offer a data-driven perspective on the biggest issues confronting insurers as we head into 2026.

Premiums Drive Satisfaction, Even Among High-Value Customers

Insurers likely knew that rate hikes were building toward a tipping point. For years, the number of customers who were shopping for new policies continued to climb, but those who were actually willing to make the switch lagged. The reasons for this varied. All insurers were raising rates, so customers couldn’t find a lower premium when they were shopping. In fact, some insurers were not actively seeking new customers. But now that insurers are getting more aggressive, customers are on the move.

Even as customer satisfaction has held steady, 29% of insurance customers switched their insurer in 2025. Of particular note, customers who had high rates of loyalty in the past – those who insurers deem “high-value” customers due to their loyalty and willingness to bundle multiple products –now say they are the least likely to renew with their insurer. In fact, just 51% of high-value customers say they will definitely renew with their insurer. Lack of understanding in pricing is key to this change in behavior. In fact, when customers understand why the price of their premiums is increasing, they are typically far more satisfied with their premium.

It’s important that insurers fill this information vacuum. In the absence of insurers explaining hikes, some customers are turning to artificial intelligence. In fact, AI is playing a heavy role in the shopping process by helping customers understand the nuances of the industry, learn the insurance lexicon and even shop quotes. This could spark the evolution of new customer habits and drive a wedge between customers and insurers. In 2026, companies need to find the best way to proactively deliver personalized customer information about their premiums.

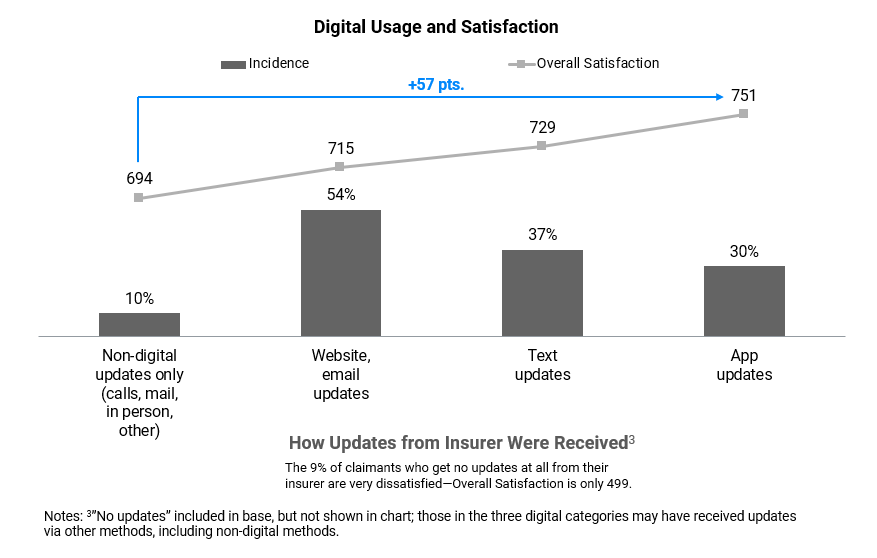

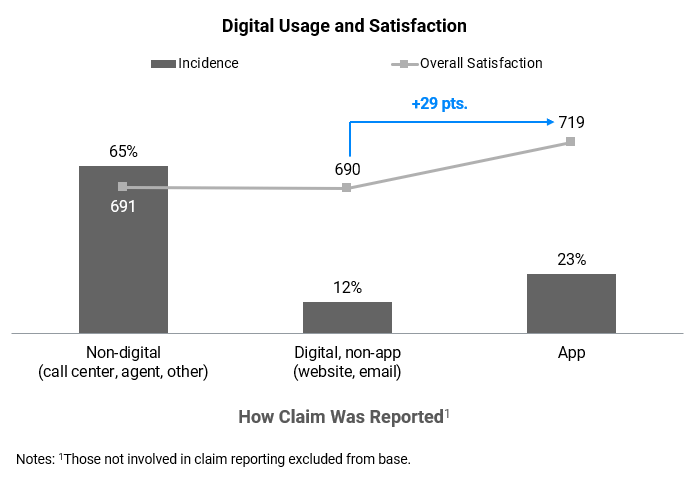

Digital Channels Take Center Stage

One way to achieve this level of personalized communication is through digital channels. Customers want a comprehensive digital experience. According to the JD Power 2025 U.S. Auto Insurance Study,SM the KPI that most drives overall customer satisfaction is providing a seamless cross-channel experience.). In fact, among customers who start their interaction through an insurer’s app, 46% are more likely to say they had a seamless cross-channel experience than those who inquire via phone or through an agent.

What’s more, 47% of all insurance policy buyers now purchase through digital channels, significantly more than through agents (35%) and more than double that of call centers (17%). The better digital experience customers have with their insurer, the more likely they are to keep using digital channels. When customers have an excellent digital experience (overall satisfaction score of 801 or higher on a 1,000-point scale), 92% say they definitely will use digital channels in the future. When customers have a poor digital experience (overall satisfaction score of 500 or less), only 40% say they are likely to use digital channels in the future.

With more customers willing to not just start a claim or speak with an agent, but also purchase policies through an app, it will be vital for insurers to create a cohesive experience between their digital channels and the rest of their business in 2026.

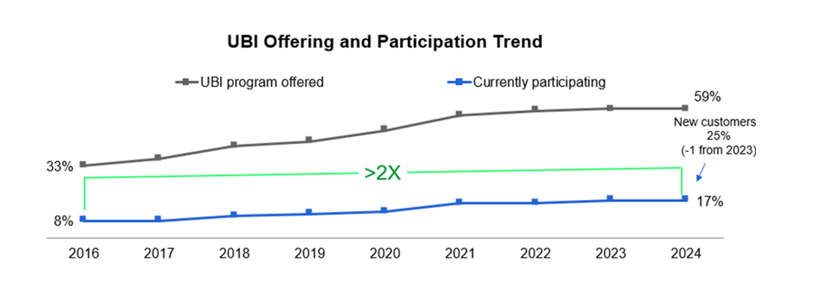

The Evolution of UBI

Usage Based Insurance (UBI), which uses telematics software to monitor an insured customers driving style and assign rates based on safety and mileage metrics, is increasingly important to shoppers, and insurers are responding in kind. This past year, 17% of insurers offered UBI programs to shoppers, up from 15% in 2024, but still down from 22% in 2023.

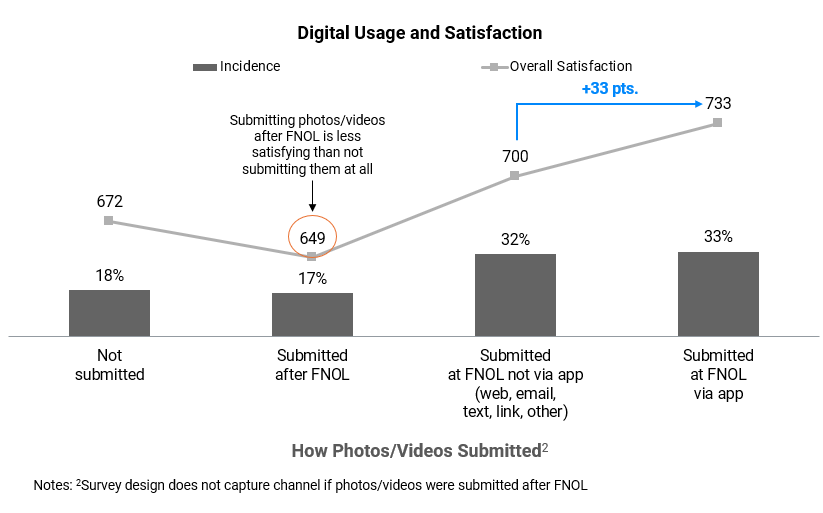

While the trend toward UBI appears to be heating up again, the drop-off from two years ago reflects challenges insurers are still dealing with as they try to get the UBI formula right. Using a mobile app to collect driving info is the most common form of data collection in UBI programs, but it also correlates with the lowest levels of customer satisfaction among those who use these apps. Insurance app (628) trails vehicle system or an onboard computer (703), a device installed in the customer’s vehicle (656), or self-reported data (640).

UBI is often used to entice customers to save money on their premiums, and with so many customers shopping their policies, this is an easy way to offer a reduced price. But customers will only find this attractive if they trust the data that is collected. Done properly, insurers can use UBI to bring down premiums, attract and retain clientele and build loyalty in the process.

Controlling the Controllables

To a degree, pricing will always create some level of attrition. But in times like these, insurers need to find ways to insulate themselves from the ebbs and flows of premium changes. To do that, companies will need to offer more personalized interactions across all channels of their customer-facing business.

With so many customers up for grabs, particularly those high-value customers who are more likely to bundle products and are almost impossible to recapture, it will be the insurers that can unlock the most streamlined interactions and proactively communicate that will succeed in 2026.

Find out More

This Insurance Intelligence Report is based on data and insights gathered across all JD Power Insurance Intelligence studies conducted during 2025. It was authored by Craig Martin, executive director; Stephen Crewdson, managing director; and Tony Soloman, director, insurance intelligence at JD Power.

Please contact us at the numbers below to connect with the team or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Joe LaMuraglia, JD Power; East Coast; 714-621-6224; [email protected]