Lending Intelligence Report

October 2024

With AI-Powered Chatbots Coming to Customer Service, Are Mortgage Customers Ready?

Artificial intelligence (AI) is here to stay. Three-fourths of business leaders say they are planning to escalate their AI investments, as they see its potential to redefine customer service and many other business functions. That includes the lending industry, in which AI-powered customer service has already started to establish a foothold and is poised to grow. Are customers ready for the future of AI-driven customer service?

This Lending Intelligence Report dives further into one aspect of the JD Power 2024 U.S. Mortgage Servicer Satisfaction Study. It highlights the prevailing sentiment and emerging trends in AI-powered customer service, and how that may change with the continued uptick in servicer adoption.

AI Can Be a Problem-Solver

Arguably one of the biggest barriers to adoption of AI-powered customer service solutions is customers’ perception of online chat. Early iterations of chatbots left many customers feeling like they were simply wasting their time. But that may be changing.

Overall, 21% of mortgage servicing customers have experienced a problem in the past 12 months. Just 9% of those customers used online chat as their first point of contact. That pales in comparison with the 48% that called customer service, but customers from Generation Y1 and Z are three times more likely to use online chat than older generations so this channel will become increasingly important.

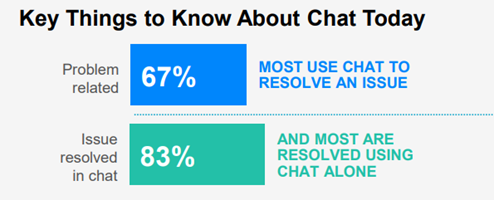

The good news is that the majority of customers who use chat found it to be useful. Two-thirds (67%) of customers using chat said it was to try to solve a problem. Of that group, 83% of those said that their problem was resolved on that chat. Unsurprisingly, those who were able to solve their problem via chat had an overall customer satisfaction rating of 702 (on a 1,000-point scale) vs. 482 for those who could not solve their problem.

An Opportunity for AI

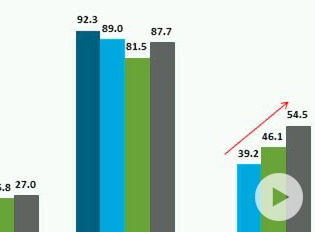

Nearly three-fourths (73%) of customers who used chat say they interreacted with a live representative, while just 10% thought it was a chat bot, and 17% were not sure. Those who said they interacted with a human had a better experience than those who thought it was a machine on the other side. Further, 63% of chat users working with a human felt the chat rep used a script, while 37% did not.

That’s important for a few reasons. Customer satisfaction for those who felt no script was used was 699, considerably higher than the average satisfaction score (636) among customers who thought a script was used. Nearly three-fourths (73%) of those customers who felt no script was used said that the process was extremely easy vs. 27% among those who felt a script was used. As AI evolves and becomes more widely adopted in the servicing industry, firms are going to need to keep a close eye on potential negative impacts to consumer perceptions. A key point for servicers to consider is that customers are usually fine with a technological improvement, provided it adds value.

That poses a challenge to lenders: An investment in AI needs to represent a clear understanding of what the customer wants in terms of service and problem resolution, and how they interact with their customer service channels. Without that, customers may simply refuse to engage, leaving lenders on the hook for the time and resources spent on underutilized technology. Those who can thread this needle will see higher customer satisfaction scores, improved processes, and streamlined costs.

Find out More

This Lending Intelligence Report is based on responses from the JD Power 2024 Mortgage Servicer Satisfaction Study, which included 11,565 responses and was fielded from May 2023 through February 2024. It is authored by Bruce Gehrke, Senior Director, Lending Intelligence. Please contact us at the numbers below to connect with Bruce or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]

[1] JD Power defines generational groups as Pre-Boomers (born before 1946); Boomers (1946-1964); Gen X (1965-1976); Gen Y (1977-1994); and Gen Z (1995-2006). Millennials (1982-1994) are a subset of Gen Y.