- Cross-channel switching for a single inquiry breaks seamless experience

- One-third of shoppers use AI, increasing switching likelihood

- Only 58% of customers fully understand auto policy coverage today

TROY, Mich.: 9 June 2026 — As the auto insurance market continues to soften, customers are holding more of the power—and they’re using it, according to the JD Power 2026 U.S. Auto Insurance Study,SM released today. Separate JD Power data1 indicates that approximately one‑third of auto insurance shoppers now turn to artificial intelligence (AI) tools when comparing coverage, and those who do are significantly more likely to switch insurers. Yet even as competition intensifies and prices ease, an increase in overall customer satisfaction is being held back by insurers’ inability to deliver truly seamless interactions across channels.

“The market has clearly shifted from a pricing crisis to an experience challenge,” said Stephen Crewdson, managing director of insurance business intelligence at JD Power. “Rates are stabilizing, but many customers still say their interactions aren’t seamless—especially when they must switch channels to resolve a single inquiry—even as a seamless cross-channel experience has become the single-most impactful driver of satisfaction in the study. At the same time, JD Power is seeing customers increasingly turn to AI tools to help compare coverage and make decisions, which underscores the growing gap between how insurers communicate and how customers now expect to engage. In a soft market, that friction will separate insurers that earn long-term loyalty from those that struggle to keep pace with rising expectations.”

Following are some key findings of the 2026 study:

- Overall auto insurance satisfaction holds steady while price satisfaction improves modestly: Overall customer satisfaction with auto insurers is unchanged year over year at 644 (on a 1,000-point scale), while satisfaction with price for coverage improves 3 points as fewer (30%) customers report insurer-initiated premium increases and more say they received multiple discounts, useful policy information and avoided payment fees. When customers experience an insurer-initiated premium increase, satisfaction with price for coverage falls by 155 points to 486 compared with those customers whose premiums stayed the same or decreased.

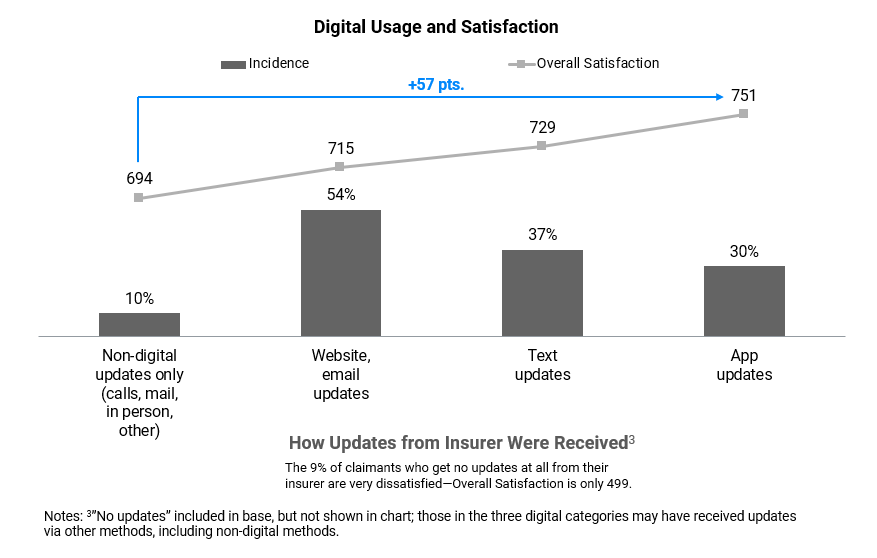

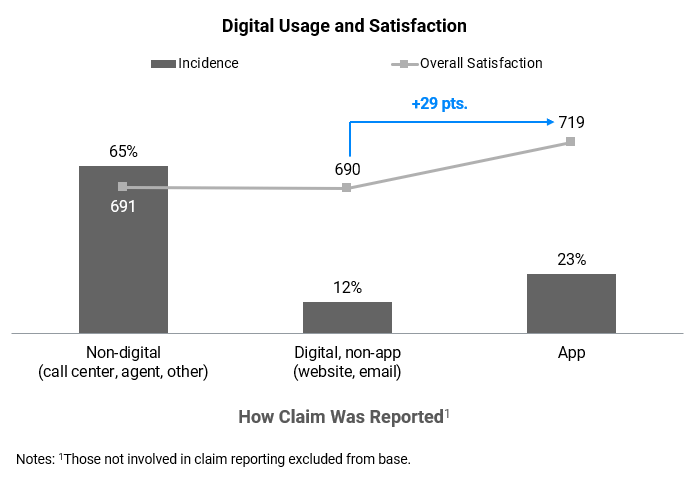

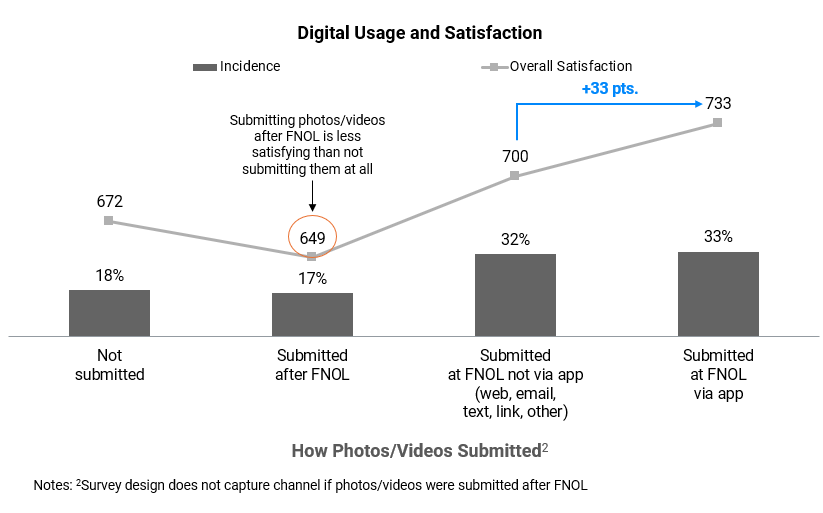

- Seamless experience breaks when customers must switch channels for a single inquiry: Insurers continue to struggle to deliver a seamless customer experience, particularly when customers are forced to switch channels for a single inquiry. Nearly half (46%) of customers used multiple interaction channels in the past 12 months, but that user experience is only meaningfully disrupted when channel switching is required to resolve a single inquiry. Those who cross channels are significantly less satisfied and less likely to renew, with 21% reporting a forced cross-channel interaction and a corresponding drop in perceived seamlessness, especially if the inquiry still does not get resolved. While agents resolve 91% of cross-channel inquiries once engaged, resolution is lowest when these inquiries go to the website (66%).

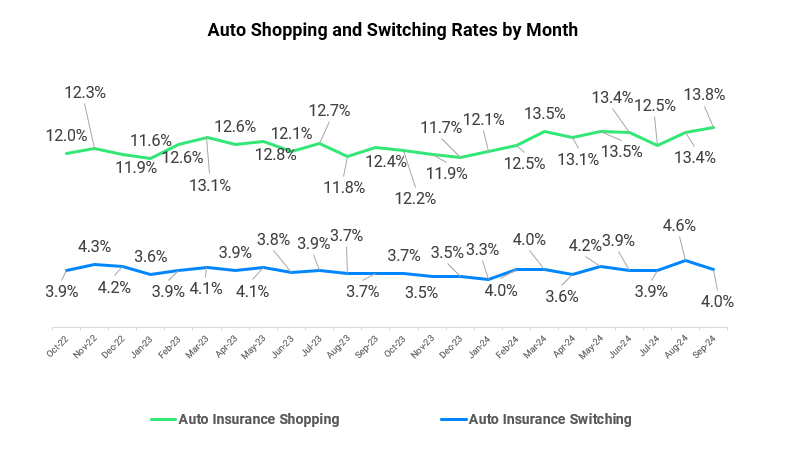

- Information gaps push customers toward AI and higher switching: According to JD Power data,2 nearly one-third (32%) of auto insurance shoppers used AI tools during their search, even as a similar share (33%) found the content unhelpful. These shoppers most often used AI for general questions, quotes, policy comparisons and decision-making. Notably, those who use AI are more than 1.3 times as likely to switch insurers compared with non-AI users, highlighting that when insurers fail to clearly explain coverage, customers turn to AI to fill knowledge gaps and shift control of information away from carriers.

- Fewer customers fully understand their auto policy: Only 58% of customers say they completely understand their auto policy and what it covers, down 4 percentage points from the 2025 study. Among customers who fully understand their policy, overall satisfaction is 127 points higher than among those who do not understand their policy, with a greater likelihood to recommend and renew with their insurer, and a higher likelihood of saying they “definitely will not” shop for auto insurance in the next 12 months. The largest impact of policy understanding is seen in satisfaction with price for coverage (+141), the second-most impactful dimension in the study and the lowest-performing area for insurers.

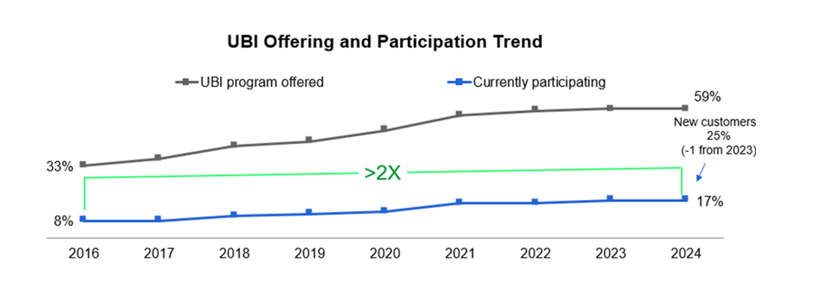

The study measures customer satisfaction with auto insurance in 11 geographic regions. A separate category addresses usage-based insurance (UBI), along with diagnostics that influence UBI participants’ experience with their insurer’s usage-based auto products. Highest-ranking auto insurers and scores by region are as follows:

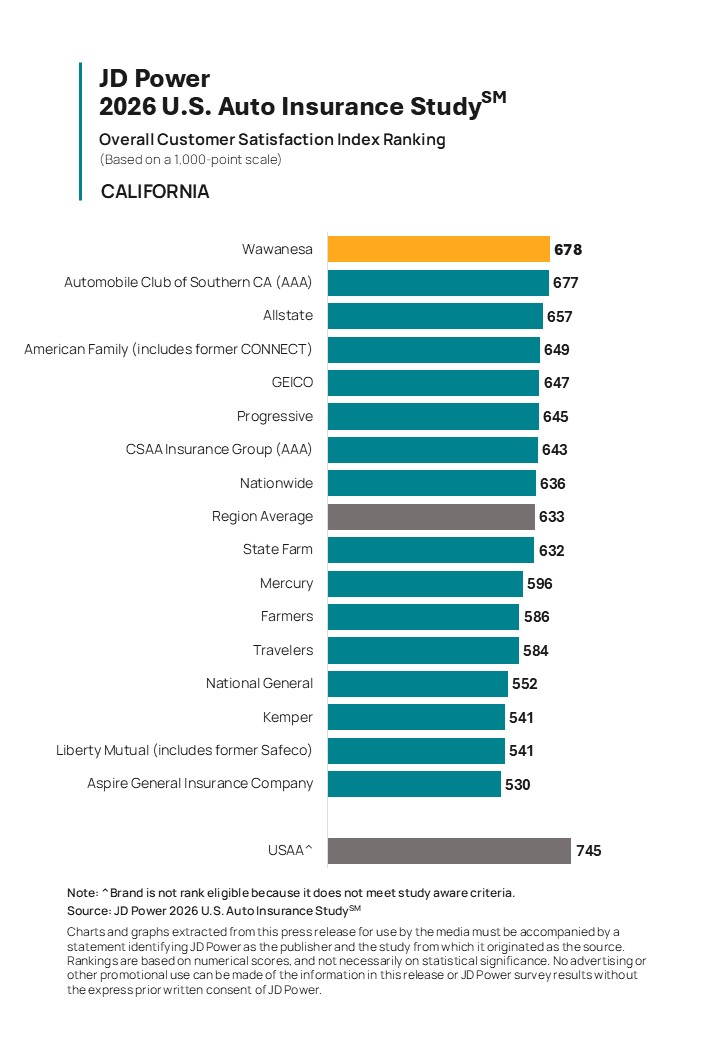

California: Wawanesa (678)

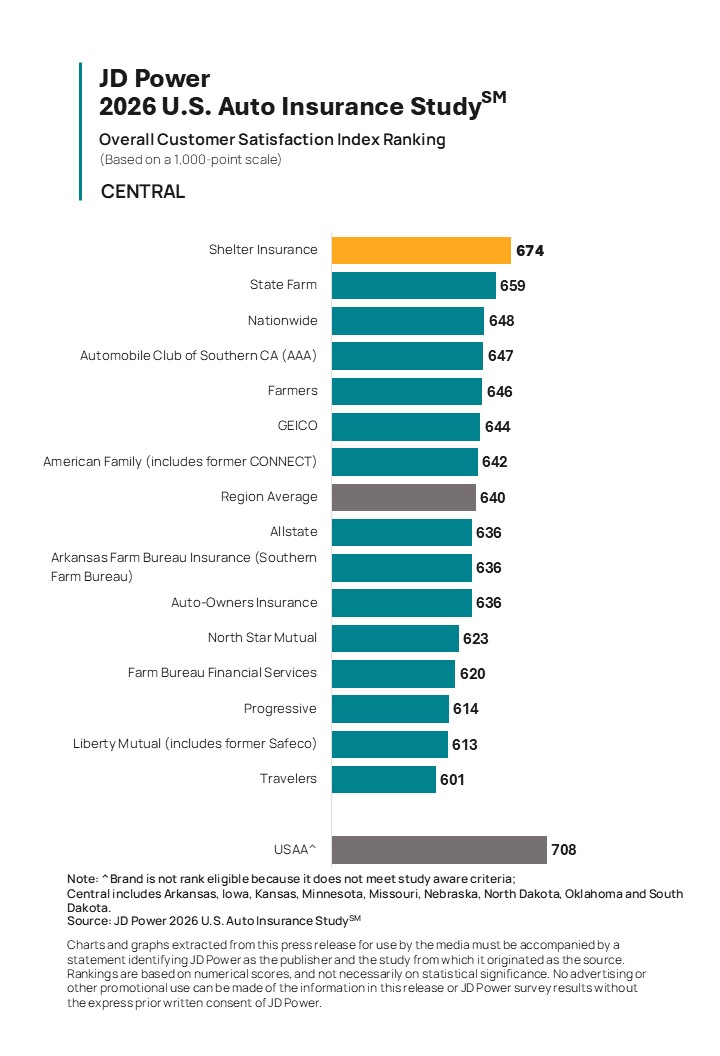

Central: Shelter Insurance (674) (for a sixth consecutive year)

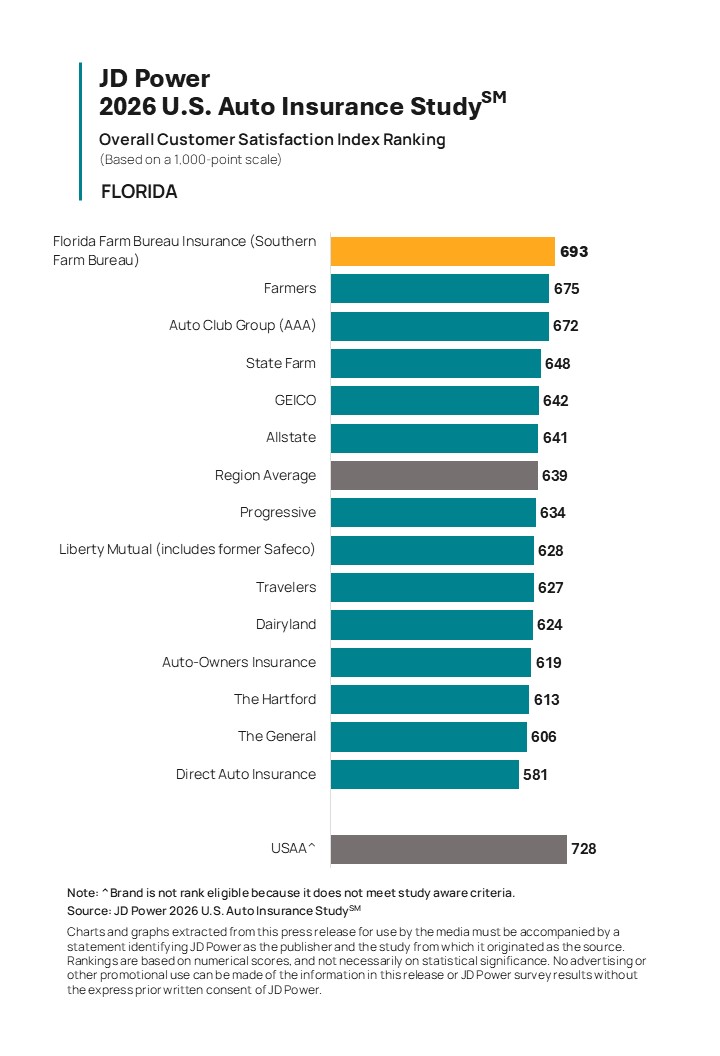

Florida: Florida Farm Bureau Insurance (693)

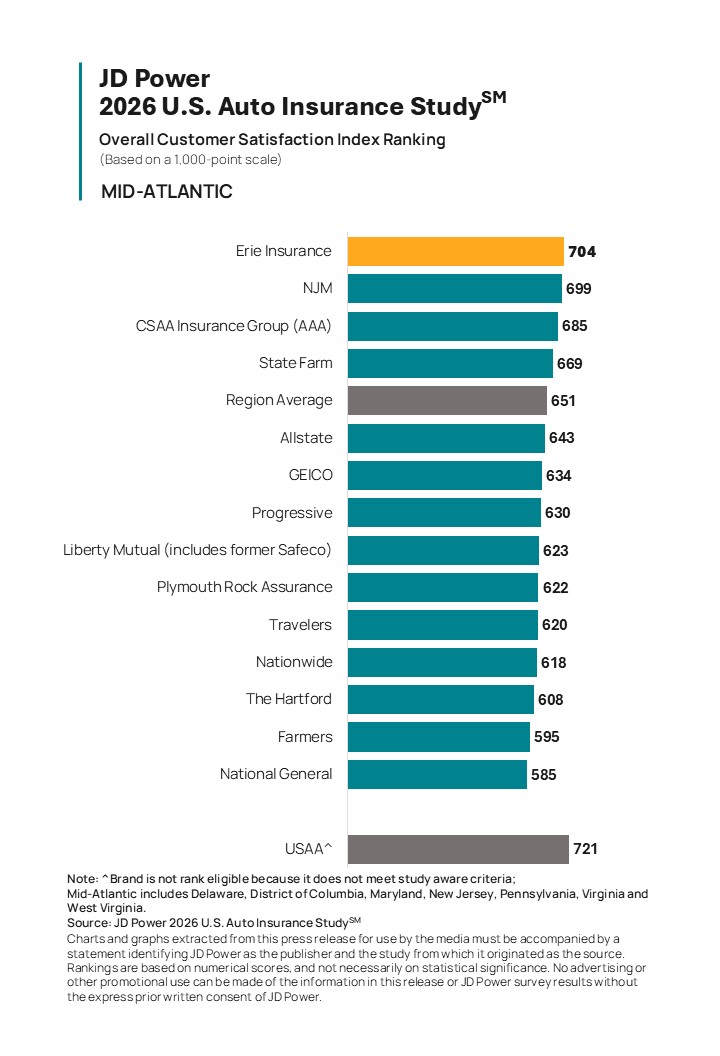

Mid-Atlantic: Erie Insurance (704)

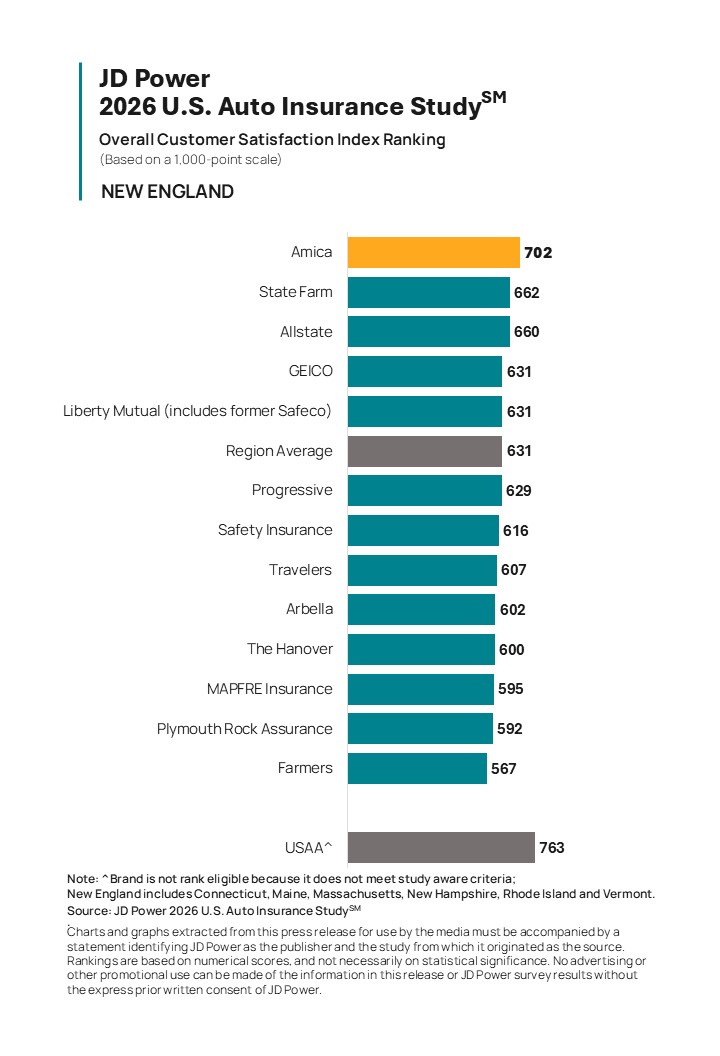

New England: Amica (702) (for a third consecutive year)

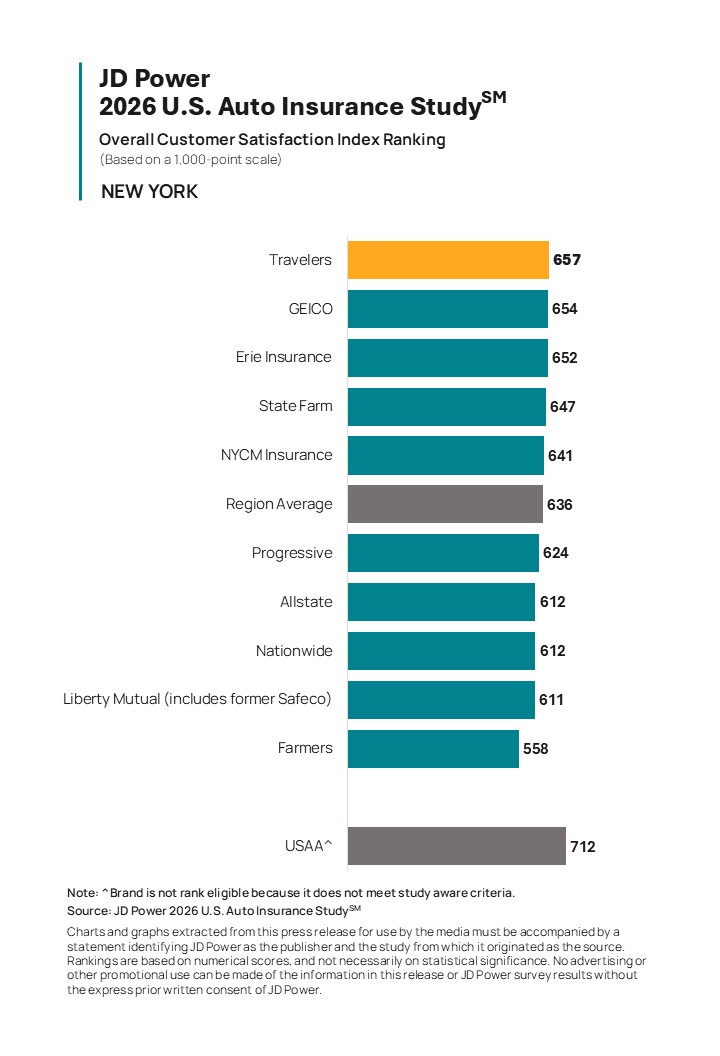

New York: Travelers (657)

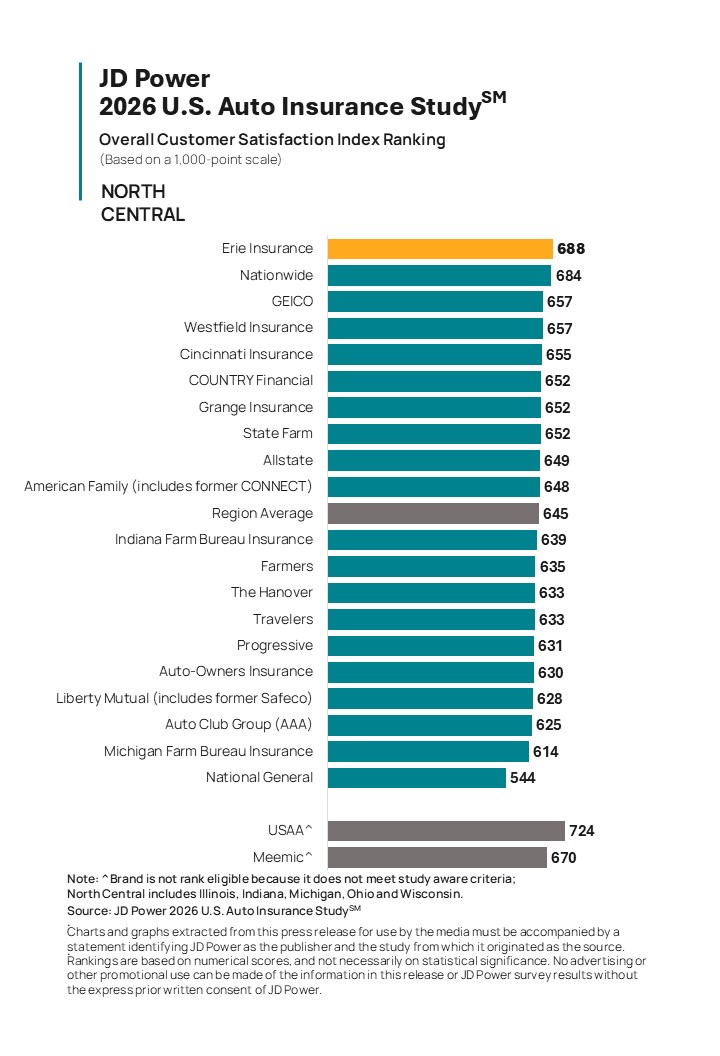

North Central: Erie Insurance (688) (for a sixth consecutive year)

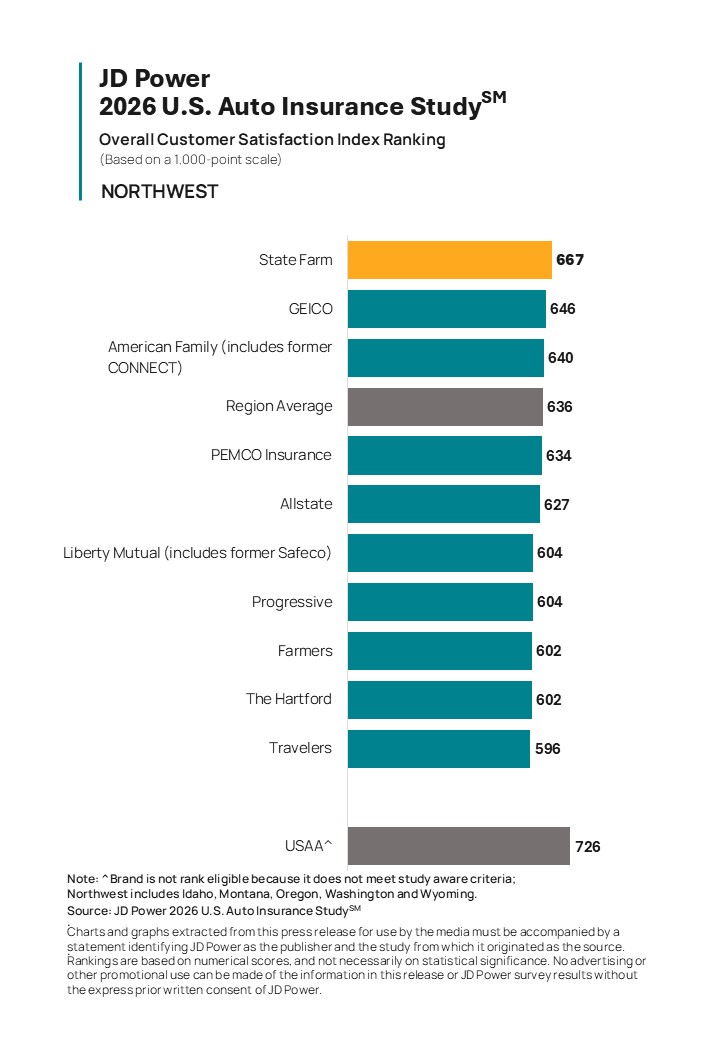

Northwest: State Farm (667) (for a second consecutive year)

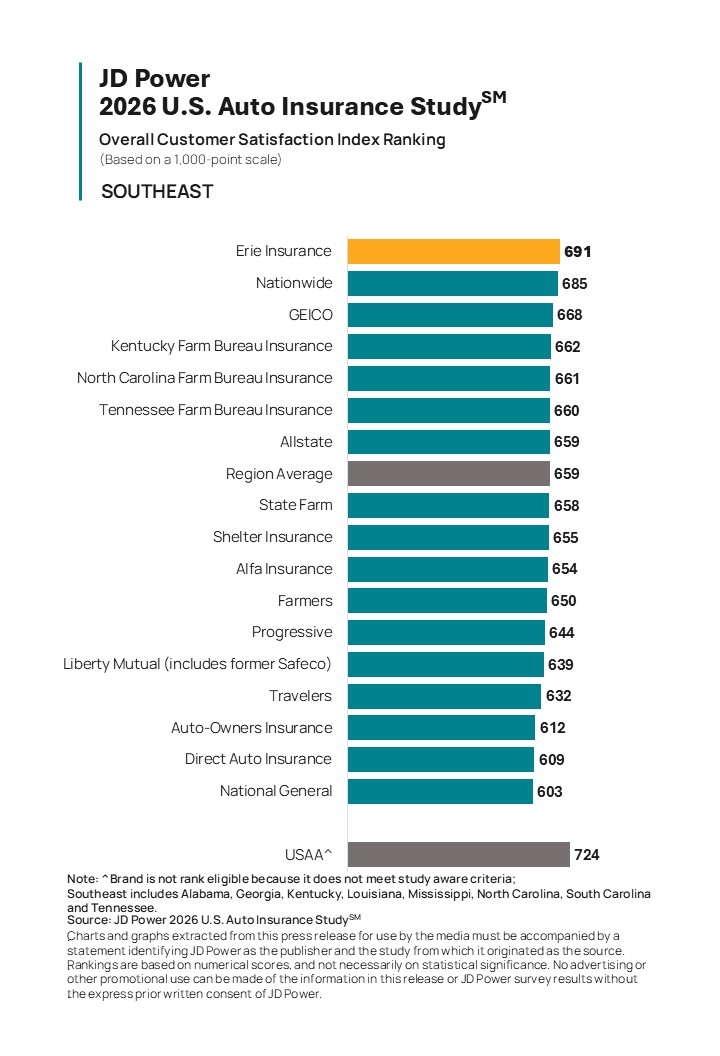

Southeast: Erie Insurance (691) (for a second consecutive year)

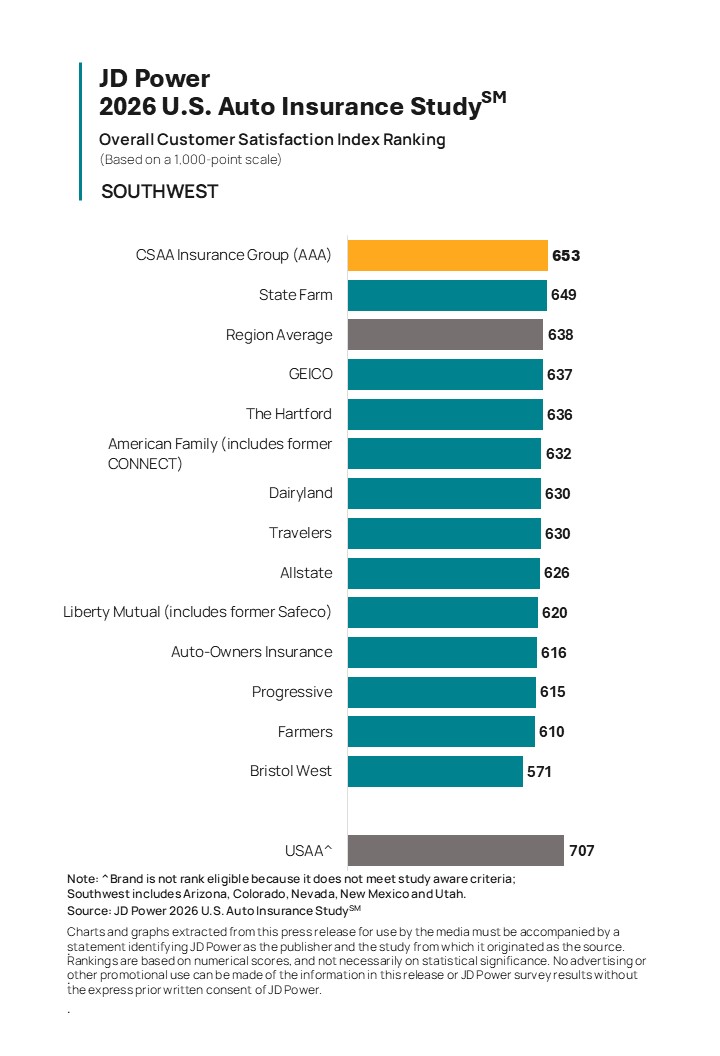

Southwest: CSAA Insurance Group (AAA) (653) (for a third consecutive year)

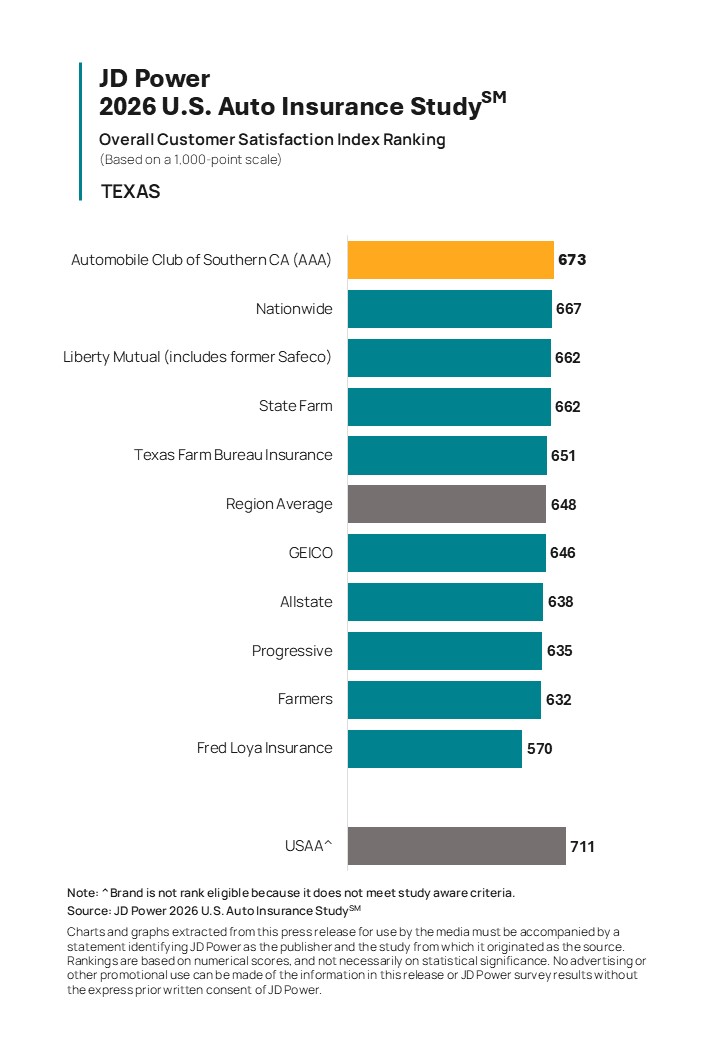

Texas: Automobile Club of Southern CA (AAA) (673)

Usage-Based Insurance (UBI): Nationwide (711) (for a third consecutive year)

The U.S. Auto Insurance Study, now in its 27th year, measures customer satisfaction with auto insurers based on performance in seven core dimensions on a poor-to-perfect rating scale. Individual dimensions measured are (in order of importance): level of trust; price for coverage; people; ease of doing business; product/coverage offerings; problem resolution; and digital channels. This year’s study is based on responses from 52,216 auto insurance customers and was fielded from April 2025 through April 2026.

For more information about the U.S. Auto Insurance Study, visit https://www.jdpower.com/business/insurance/auto-insurance-study.

About JD Power

JD Power delivers mission-critical data, analytics and intelligence that help businesses improve customer experience and operational performance with confidence and clarity. Using proprietary, comprehensive data–including millions of consumer interactions and authoritative automotive datasets–combined with advanced analytics, artificial intelligence and deep industry expertise, JD Power enables leaders to respond to market shifts, make smarter decisions and drive measurable performance improvements.

As an objective source of deep insight into real-world customer interactions with brands and products, JD Power provides the independent intelligence organizations need to anticipate change, strengthen customer engagement and advance growth. Learn more at JDPower.com.

Media Relations Contacts

Joe LaMuraglia, JD Power; East Coast; 714-621-6224; [email protected]

John Roderick; East Coast; 631-584-2200; [email protected]

About JD Power and Advertising/Promotional Rules: www.jdpower.com/business/about-us/press-release-info

1JD Power AI and Insurance Special Report, January 2026

2JD Power AI and Insurance Special Report, January 2026