E-Vision Intelligence Report

February 2023

Consumer Price Sensitivity Asserts Influence on EV Market

Key Findings

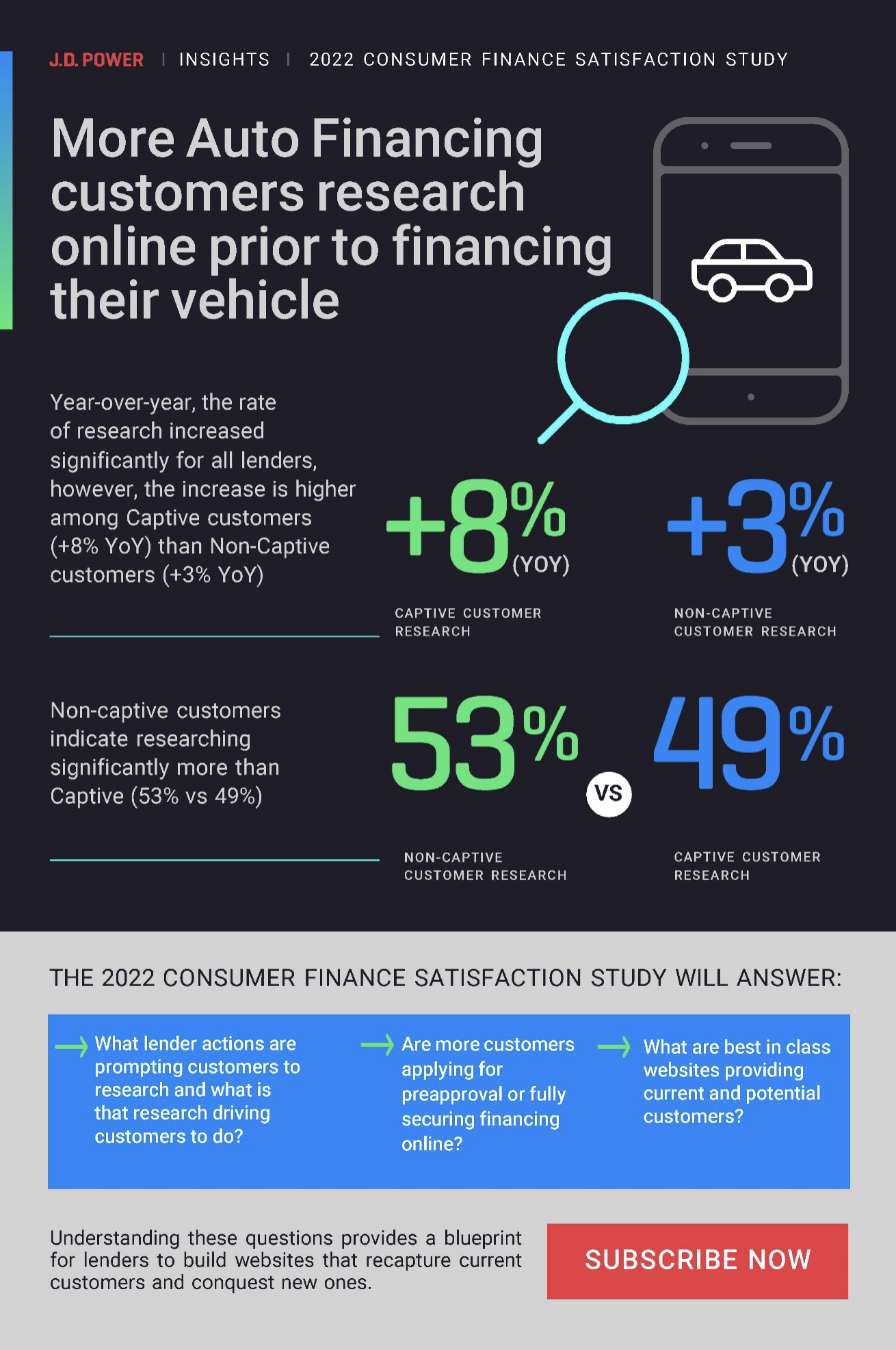

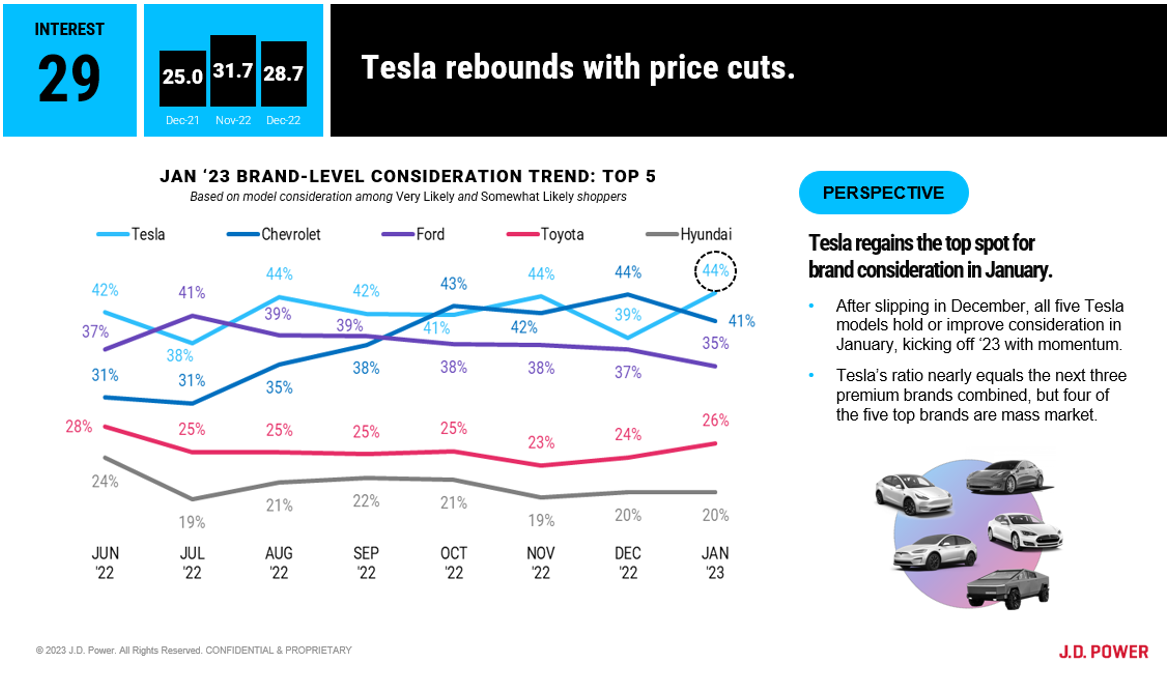

- Price Cuts Catapult Tesla to Top of Consumer Consideration List: After losing ground, Tesla has again emerged as the most-considered EV brand among shoppers, with 44% either “very likely” or “somewhat likely” to consider the brand for their next EV purchase.

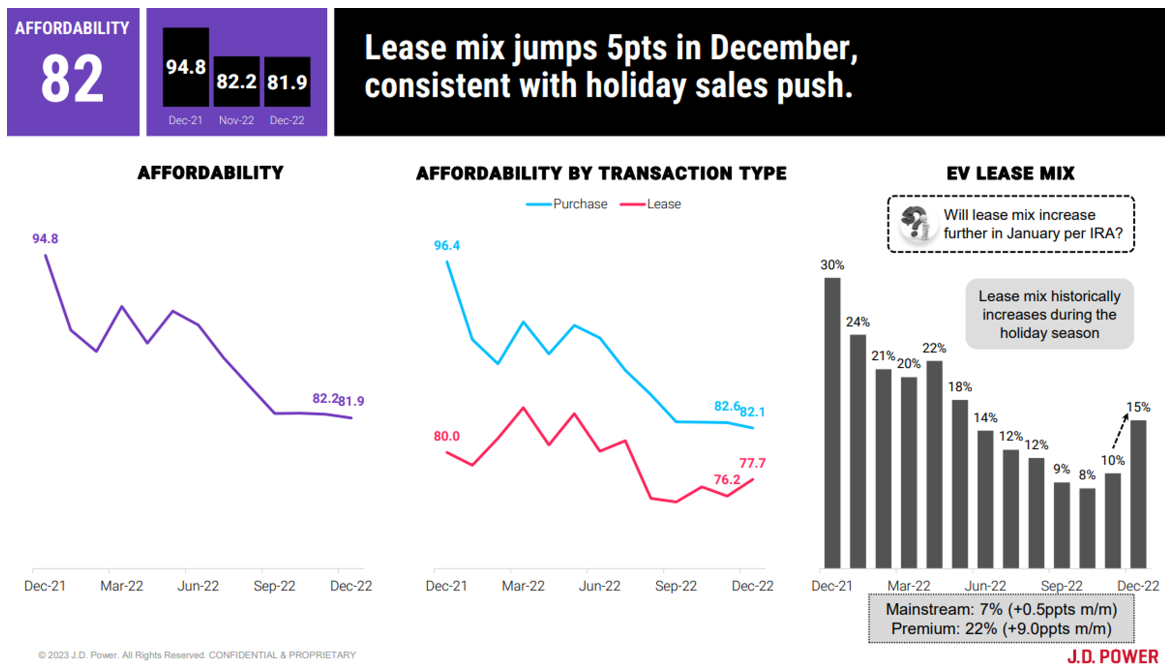

- Leasing Volumes Surge 46% on Tax Credit: EV leases accounted for 15% of total sales in December 2022. In January, that ratio is expected to jump to 22% as manufacturers take advantage of Inflation Reduction Act tax credit to incentivize leasing.

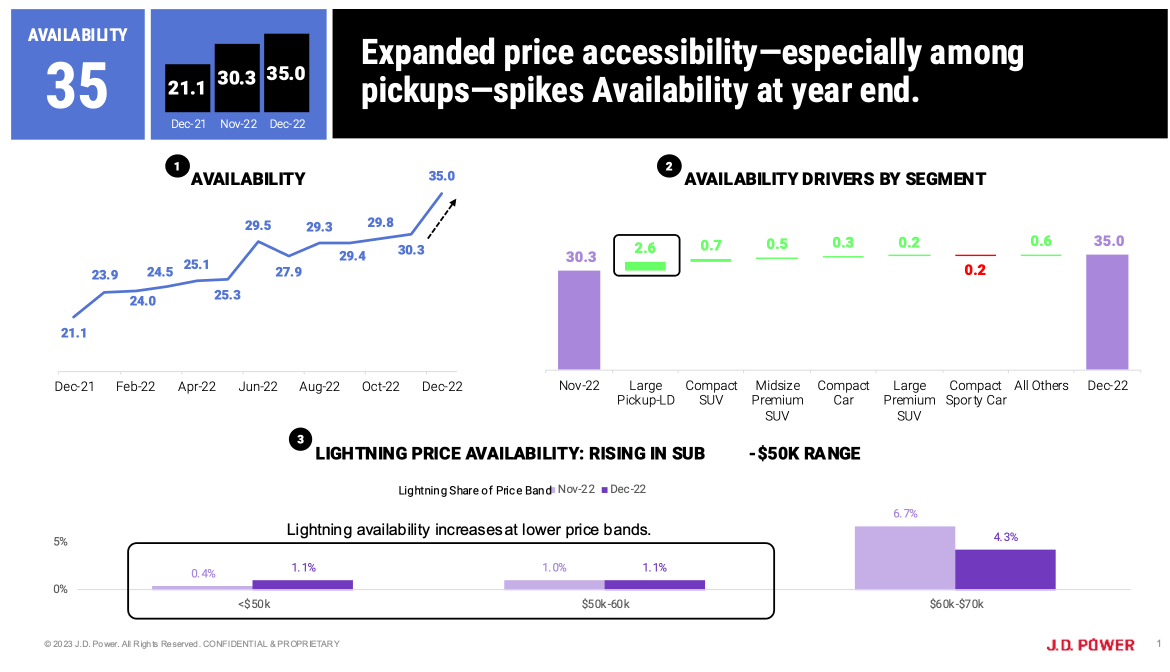

- Availability Grows for Lower-Priced Trims of Popular Models: Overall EV availability has increased 5 index points, driven largely by growing availability of lower-priced, lower trim-level versions of popular models, such as the Ford F-150 Lightning.

Executive Summary

If ever there were a sign that EVs are rapidly transforming from high-priced playthings into mainstream consumer goods that are highly sensitive to economic trends, it was the complete about-face of consumer interest in Tesla following the brand’s January 2023 price cuts. After dropping prices across its lineup by as much as 20% virtually overnight, consumer interest in Tesla spiked, reversing a recent trend of waning consumer interest.

According to the JD Power EV Index, a new analytics tool developed by JD Power to track the progress to parity of EVs with internal combustion engine (ICE) vehicles in the United States, the recent swing in Tesla brand consideration is part of a much larger trend toward consumer price sensitivity becoming an even more significant factor in the EV adoption curve. This E-Vision Intelligence Report dives into key data points trending in each monthly EV Index update, along with other data points gathered from JD Power studies and pulse surveys, to spotlight emerging trends and important shifts in EV consumer sentiment.

Price-Sensitive Tesla Shoppers

Tesla can be credited with breaking down many of the barriers that once existed to widespread EV adoption, but affordability has not historically been one of them. The most affordable version of its Model 3 sedan retailed for about $47,000 in December 2022, while the brand’s average transaction price hovered near $73,000 throughout most of 2022. During that same period, the JD Power EV Index identified a trend toward waning consumer interest in Tesla. In fact, from November to December 2022, the percentage of shoppers either “very likely” or “somewhat likely” to consider a Tesla for their next EV purchase fell to 39% from 44%, falling behind more mainstream offerings from Chevrolet.

Then, in mid-January of 2023, Tesla announced sweeping price cuts that brought the price of a base Model 3 down to $44,000 and cut the price of some models and trims by as much 20%. Immediately, consumer interest suddenly roared back, putting Tesla back on top of the brand consideration ranks, with 44% of EV shoppers indicating interest in the brand.

Suddenly, the brand that has been most closely associated with the premium market sentiment that has accompanied the growth of EVs, is starting to exhibit demand dynamics more in line with mainstream consumer goods. It should come as little surprise, then, that the other four brands at the top of the EV consideration list are all mainstream brands: Chevrolet (41%), Ford (35%), Toyota (26%) and Hyundai (20%).

Leasing Comes Back Big with Boost from Inflation Reduction Act

Another major shift in consumer behavior is afoot in EV leasing activity. After consistently trending downward since April 2022, EV lease mix increased to 15% in December, up five percentage points from the previous month. But that was just a harbinger of things to come. Based on an early look at January data, we find that EV lease mix has spiked to 22% of total EV volume.

That boost in month-over-month lease volume is, of course, driven by the Inflation Reduction Act and its provision designed to incentivize commercial fleets to go electric with a $7,500 federal tax credit for commercial EVs. The way the law is written, however, vehicles leased to consumers qualify as commerical. That means automakers can now opt to pass the $7,500 credit—or some portion of it—to customers who choose to lease rather than buy a new EV. Clearly, the policy has had an immediate and signifant effect on lease mix.

Lower-Trim EVs Gain Traction in December

There is a commonly used strategy in the auto industry called “launching rich.” It occurs when brands know they have a new vehicle launch that will garner lots of attention and consumer demand and use that momentum to drive sales of their highest priced trim packages at launch. It’s the logic behind special launch edition and first edition models that come loaded with every option, and it has been used widely in the EV space.

As a case in point, consider the Ford F-150 Lightning pickup, which, when it launched in the Spring of 2022, had an average transaction price of $85,600 according to the JD Power EV Index. By August, however, that average transaction price had decreased to $77,400 pulled down by increased sales volume in lower trim models priced in the sub-$50K range. In December, Ford announced a $4,000 price increase for 2023 models, bringing the average transaction price back up to $82,500.

Methodology

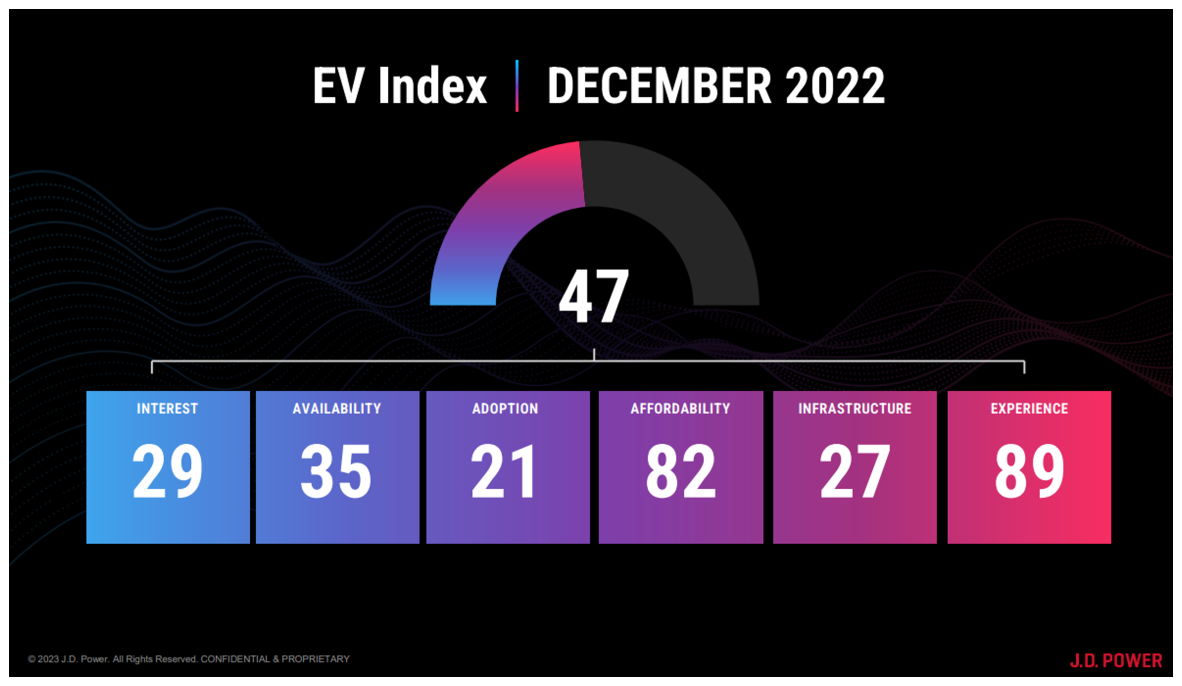

This JD Power E-Vision Intelligence Report is based on data and insights from the JD Power EV Index and the JD Power EV Consideration pulse survey. The JD Power EV Index is an analytics tool to benchmark the growing EV market in the United States. It tracks millions of data points aggregated into six categories—interest, availability, adoption, affordability, infrastructure and experience—to evaluate the progress to parity of EVs with ICE vehicles in the U.S. Each month, JD Power’s electric vehicle practice will analyze these data points, and others to spotlight emerging trends and important shifts in consumer sentiment that are helping to define the fast-moving EV marketplace.

Find out More

This report was authored by Elizabeth Krear, vice president, electric vehicle practice; Brent Gruber, executive director, electric vehicle practice; Stewart Stropp, executive director, electric vehicle practice; and Kristen Richter, senior analyst, electric vehicle practice at JD Power. The JD Power E-Vision initiative is a company-wide program focused on maximizing JD Power industry-leading EV data, analytics, insights and solutions. Please contact us at the numbers below to connect with the authors or to learn more about the underlying research.

Media Contacts

Shane Smith; East Coast; 424-903-3665; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]