As the UK adopts incentives for battery-electric vehicle (BEV) purchases, the market suffered another decline in new-car deliveries last month. Autovista24 special content editor Phil Curry examines the situation.

The UK’s new-car market fell back into decline in July, as the country’s rollercoaster registrations ride continued.

In July, 140,154 new models were registered, according to data from the SMMT. This was a 5% decline compared to the same month last year. The fall comes despite the announcement of new incentives aimed at boosting the sales of BEV models.

Demand from private buyers fell by 3.2% to 51,646 units in the month. Meanwhile, fleet registrations also declined, with 85,594 units representing a 6.5% drop. Deliveries in the lower volume business sector climbed 10.4% to 2,914 units.

Across the first seven months of the year, UK registrations were up 2.4%. This was thanks to a strong performance in March, with further increases in May and June. In total, 1,182,373 units have been delivered so far in 2025.

Will incentives provide benefits?

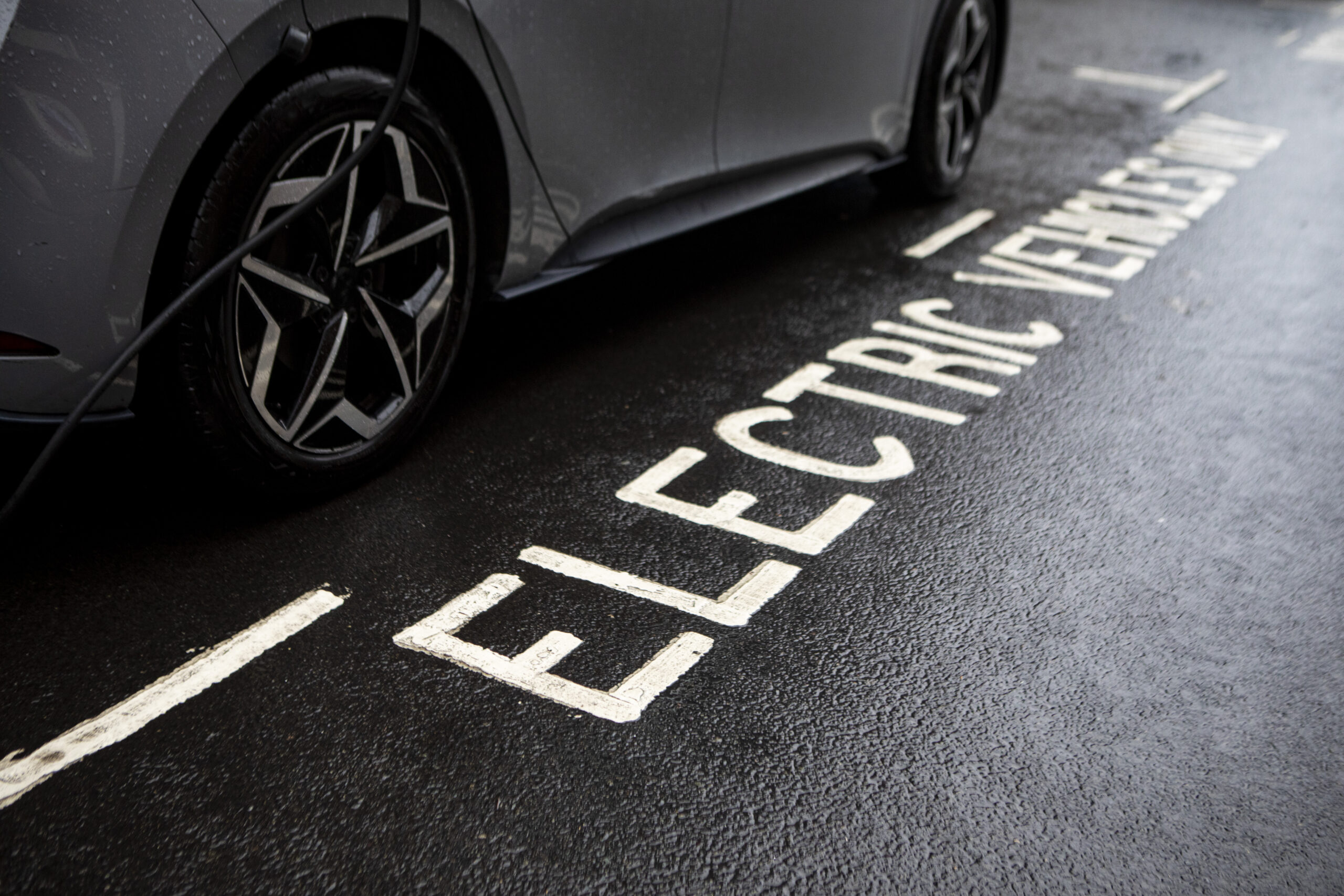

The UK government announced a new incentive scheme for the purchase of new BEVs, which became available during July.

The plans require manufacturers to nominate their passenger cars and light-commercial vehicles to be eligible. A split-tier incentive scheme means models will either qualify for a discount of £3,750 (€4,299) or £1,500.

The grant level is based on strict sustainability criteria. Carmakers must have committed to a science-based target on emissions. Specifically, a goal to cut greenhouse gas emissions in line with the Paris Agreement on climate change.

According to the Independent, manufacturers will need to demonstrate their vehicles meet minimum technical requirements. They must also submit details about the manufacturing process and have a net-zero target in place.

The carbon emissions of electricity grids in the manufacturing location will also be important. This will count towards an environmental score assigned to the vehicle assembly and battery production location. A weighting of 70% is applied to the assessment of CO2 emissions from battery manufacturing, and 30% to vehicle assembly.

Models will also need to cost below £37,000 to be eligible for the scheme. This is below the government’s expensive car supplement (ECS) threshold of £40,000, which still applies to BEVs.

Incentives momentum is essential

With £650 million applied, the incentive scheme will run until the end of April 2029. The aim is to boost BEV sales at a time when overall registrations remain below 2025’s 28% zero-emission vehicle (ZEV) mandate threshold.

As the UK moves towards the end of petrol and diesel new-car sales in 2030, these targets will get larger. While BEV uptake has improved, it has not hit the levels expected.

‘Rapid deployment and availability of this grant over the next few years will help provide the momentum that is essential to take the EV market from just one in four today, to four in five by the end of the decade,’ commented SMMT chief executive, Mike Hawes.

‘This announcement is a welcome response to consistent calls from the industry for more support, which will be in addition to the substantive subsidies already provided by manufacturers,’ he added.

Manufacturer response to incentives

With reduced prices coming into effect from 5 August, the first models to secure the £1,500 discount are:

- Citroën ë-C3 and Citroën ë-C3 Aircross

- Citroën ë-C4 and Citroën ë-C4 X

- Citroën ë-C5 Aircross

- Citroën ë-Berlingo

With no higher discounts awarded, this highlights the potential difficulty in achieving the required sustainability status for the maximum amount. Some carmakers have already begun including discounts against models at their own expense.

Announcing its support for the scheme, MG introduced a £1,500 discount on certain all-electric models, separate from governmental funding. Smart UK announced its own £1,500 incentive scheme, on top of existing offers. Volkswagen (VW) Group has introduced a £1,500 ‘government guarantee’, providing a discount to buyers while it waits for model eligibility.

Meanwhile, Chinese carmaker BYD has announced its own scheme after what it calls ‘uncertainty surrounding eligibility’ around the government scheme.

‘While BYD has formally applied to be included in the government-backed scheme, the brand may not be immediately eligible,’ the carmaker said. Therefore, it has increased its battery warranty to eight years and has launched five years of free servicing on selected models.

These moves are likely to increase the burden of manufacturer discounting. This already reached around £6.5 billion since the introduction of the ZEV Mandate in January 2024, according to the SMMT.

The government also provided details on plans for £63 million of funding to support at-home charging for households with driveways.

This aims to make it easier for councils to put channels in pavements. Drivers will then be able to run cables from their home to their vehicle parked on the road outside. The funding will also help transition NHS fleets and create thousands of charge points at business depots.

BEV growth slows

The incentives did little to affect BEV uptake in July. While model eligibility is confirmed, private buyers may be holding back, waiting to see which discounts are available.

In the month, BEV registrations increased by 9.1% year on year. This was the second-lowest improvement of the year, and the second time growth has been below 25%. It is also a far cry from the first quarter of 2025, when the total registration rise was 42.2%.

In total, 29,825 new all-electric models took to UK roads last month, 2,490 units more than a year ago. This gave the technology a 21.3% market share. While this was up by 2.8 percentage points (pp), it was still below the ZEV mandate target of 28%.

In the first seven months of the year, BEV registrations increased by 31%, with 254,666 units delivered to customers. This is a rise of 60,235 passenger cars compared to the same period in 2024.

The 21.5% market share was 4.7pp higher than that achieved between January and July 2024. However, this is some way off the ZEV mandate target.

‘Confirming which models qualify for the new BEV grant, alongside compelling manufacturer discounts on a huge choice of exciting new vehicles, should send a strong signal to buyers that now is the time to switch,’ added Hawes.

‘That would mean increased demand for the rest of this year and into next, which is good news for the industry, car buyers and our environmental ambitions,’ he added.

Phenomenal PHEV performance

The standout powertrain in the UK during July was the plug-in hybrid (PHEV). It saw registrations increase by 33%, with 17,489 units delivered. This gave the technology a 12.5% market share, up from the 8.9% recorded in the same month last year.

In the first seven months of 2025, PHEVs have seen registrations improve by 31.5%. This means their growth rate is now higher than BEVs. In total, 124,528 units have been delivered, giving PHEVs a 10.5% hold of the market. This is a jump of 2.3pp year on year.

Combining BEVs and PHEVs, the electric vehicle (EV) market saw a rise of 16.9% in July. This equated to 6,830 more models taking to the road. Their share of 33.8% was up 6.4pp compared to the same month in 2024.

In the year to date, EV deliveries were up 31.2%, reaching 379,194 units. A 32.1% market share was up from the 25% recorded in the first seven months of 2024.

Hybrids struggling

Full hybrid (HEV) figures dropped for the second consecutive month and the third time in 2025. Deliveries were down 10% in July with 18,551 units, equating to a 13.2% market share. This was 0.8pp down year on year.

Between January and July, HEVs have seen registrations improve by 6.5%, with 165,328 deliveries. This provided the technology with a 14% share of the market, rising by just 0.5pp compared to 12 months prior.

The monthly market share between HEVs and PHEVs has been narrowing across 2025. The gap between the two powertrains in July was just 0.7pp, while in the year-to-date, PHEV trailed HEVs by 3.5pp. Momentum appears to be firmly behind PHEV powertrains in the UK market at present.

Combining EVs and HEVs, the electrified vehicle market saw a 7.8% improvement in July, with 4,758 more models delivered. This equated to a 47% share of the total, up 5.6pp.

Between January and July, registrations improved 22.5%, with 100,137 more units hitting the road. Its 46.1% share was up from 38.5% seen in the same period during 2024.

ICE continues to drop

While EVs flourish, internal-combustion engine (ICE) figures, which include mild-hybrid powertrains, continued to fall in the UK.

Petrol registrations declined by 14.7% in July, with 66,271 units delivered. However, this figure was still the highest total of any powertrain, even with 11,431 fewer models taking to the country’s roads than July 2024. The performance gave petrol a 47.3% share of total figures, down by 5.4pp.

Petrol is on a downward spiral, suffering declines in each month of the year so far. Figures between January and July were down by 10.1%, with 571,111 deliveries.

However, this is a difference of 63,856 units year on year. This means petrol held 48.3% of the UK market. Its share is still dominant, but down by 6.7pp compared to the same period last year.

Meanwhile, following its slight improvement in June, diesel returned to a decline in July. Figures were down 7.9%, with 8,018 registrations. This was a difference of just 690 units year on year. In terms of market share, diesel now lags well behind other powertrains. Its 5.7% hold in the month was 0.2pp down compared to July 2024.

In the first seven months of 2025, diesel has seen 66,740 registrations, a 10.9% decrease compared to 12 months prior. Its 5.6% market share was 0.9pp down on the same period last year.

These poor performances meant that the overall ICE market fell by 14% in July. It still led the electrified sector, with a 53% share. This was down, however, from the 58.6% market hold it recorded in July last year.

Across the first seven months of the year, ICE registrations were down 10.1%. Its 53.9% market share was still leading but was down by 7.6pp.