The concern about inflation among bank customers in the United States is seemingly cooling but new worries about energy costs are bubbling up with each new summer heatwave.

The average utilization rate of electricity is on the rise and, as a result, the cost of summer season cooling is set to spike. That has customers worried that their energy bills will absorb any savings they might be seeing on consumer goods.

According to JD Power, the percentage of U.S. bank customers who are financially healthy[1] has remained steady and the overall level of concern regarding inflation has begun to fall, but customers in every financial category are at least somewhat worried about the size of their energy bill.

It’s a discouraging development for customers trying to dig out of the financial holes left by the last two years, as they try to discern how they can manage both their energy consumption and their budgets in the face of unrelenting weather.

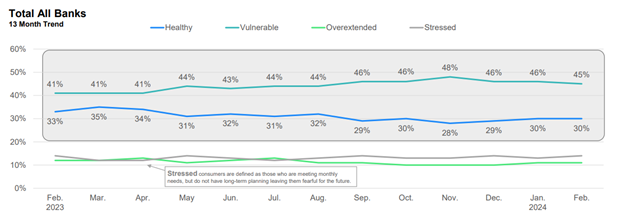

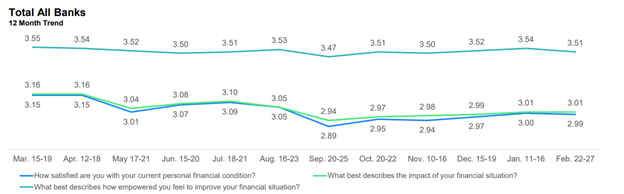

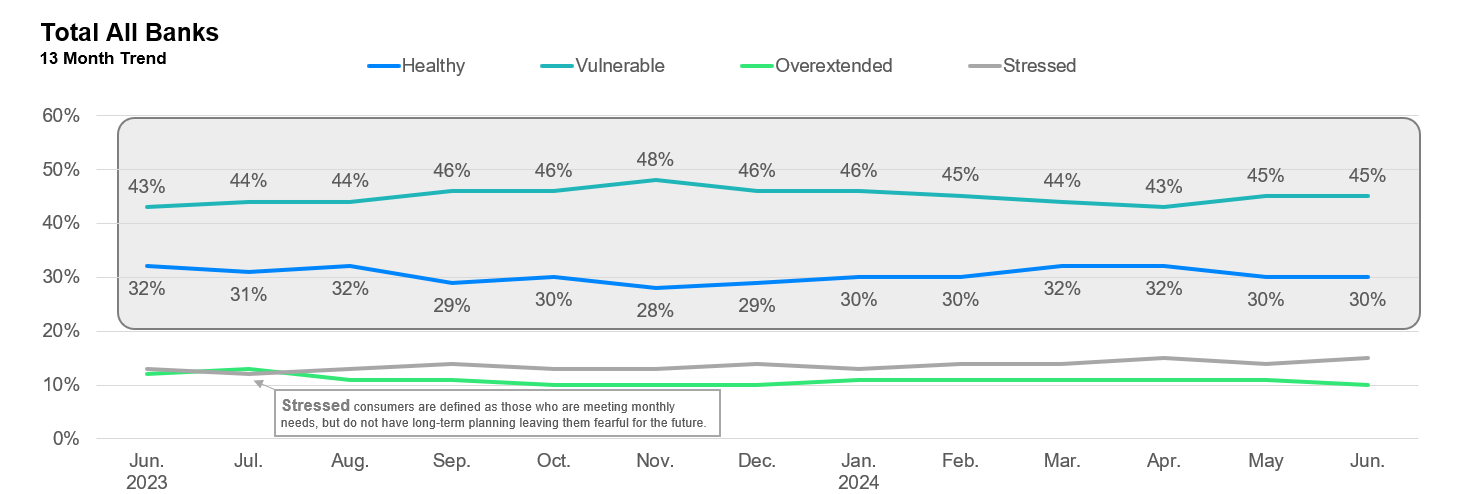

Financial Health Largely Flat as Inflation Concerns Wane

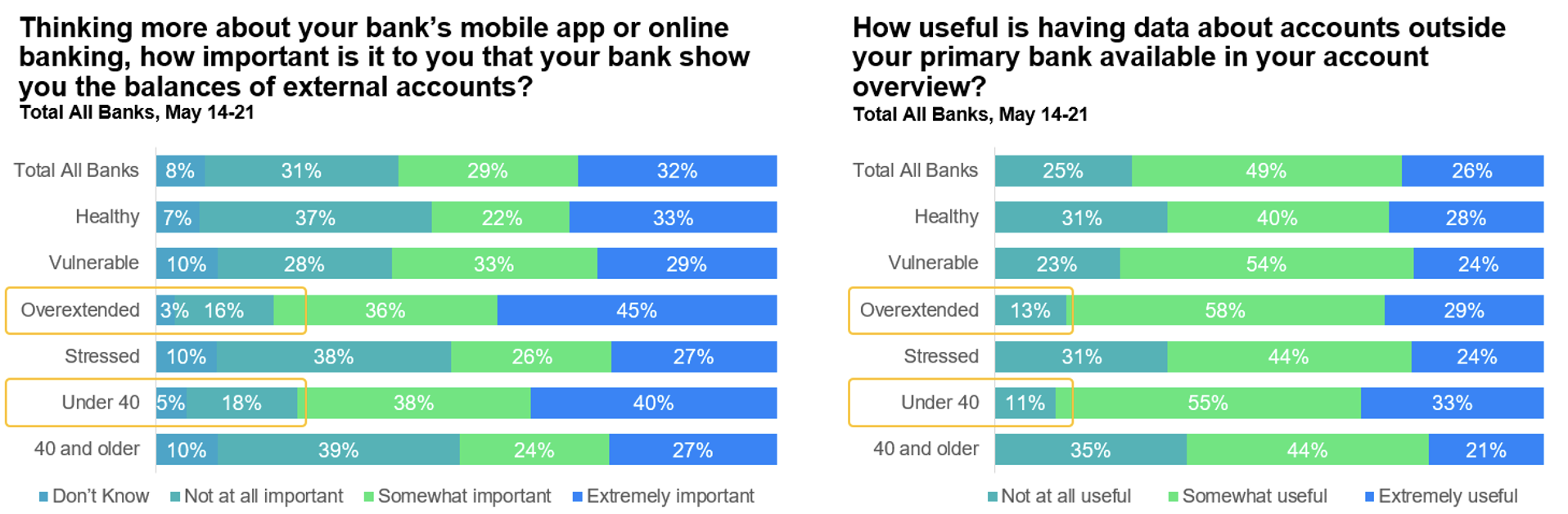

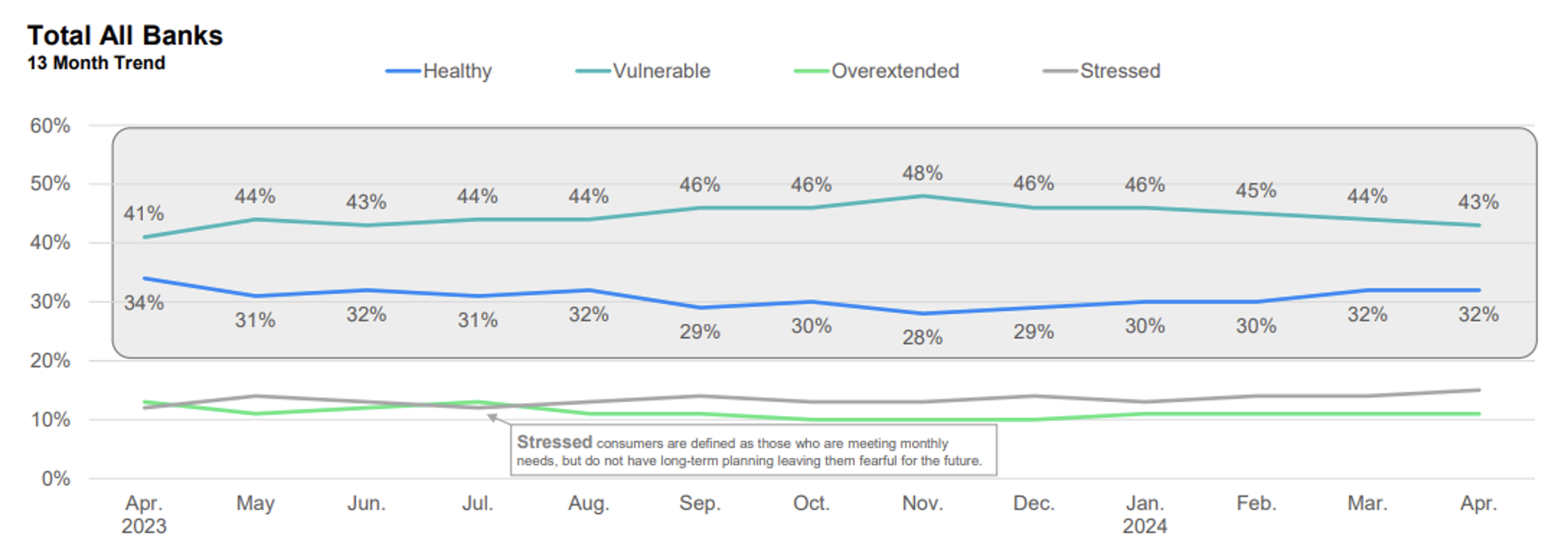

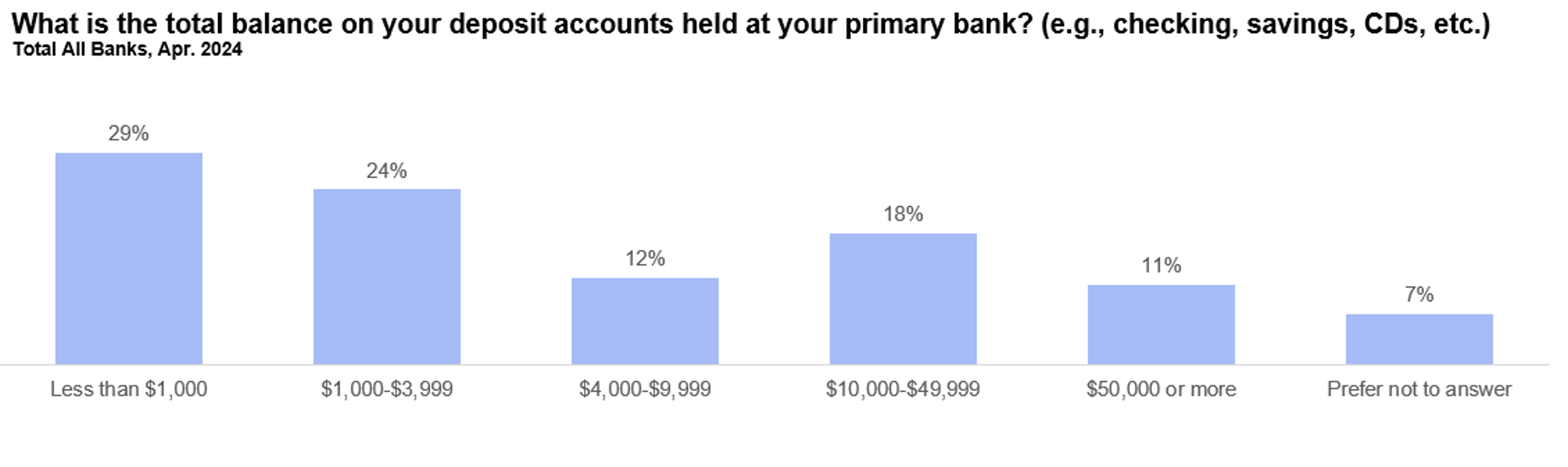

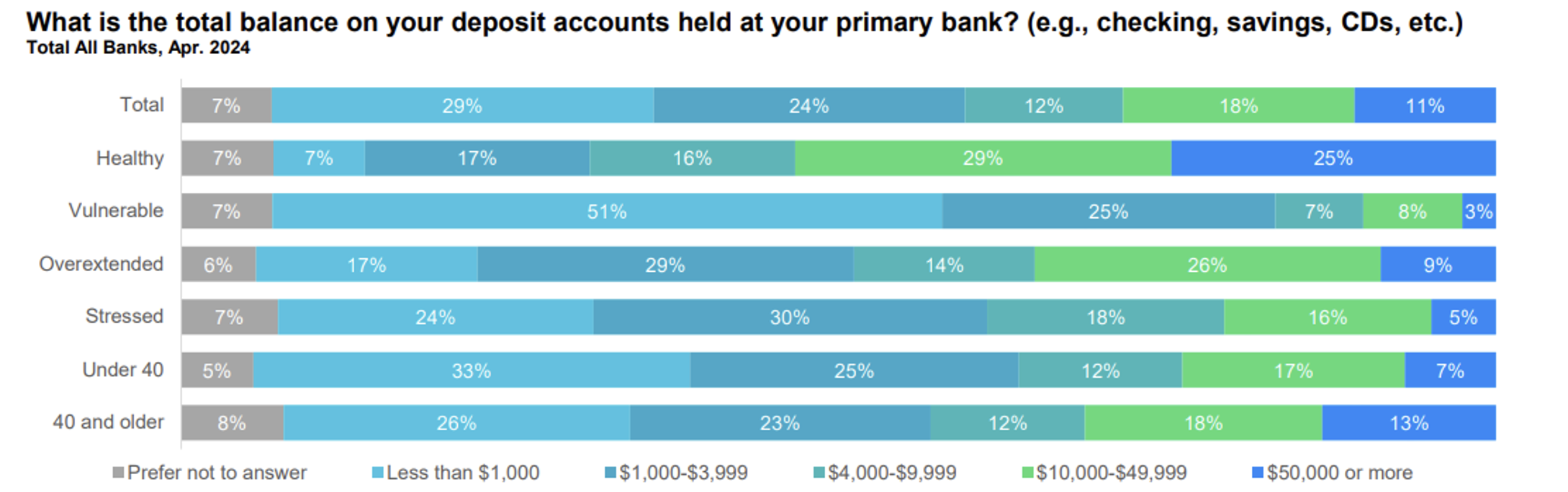

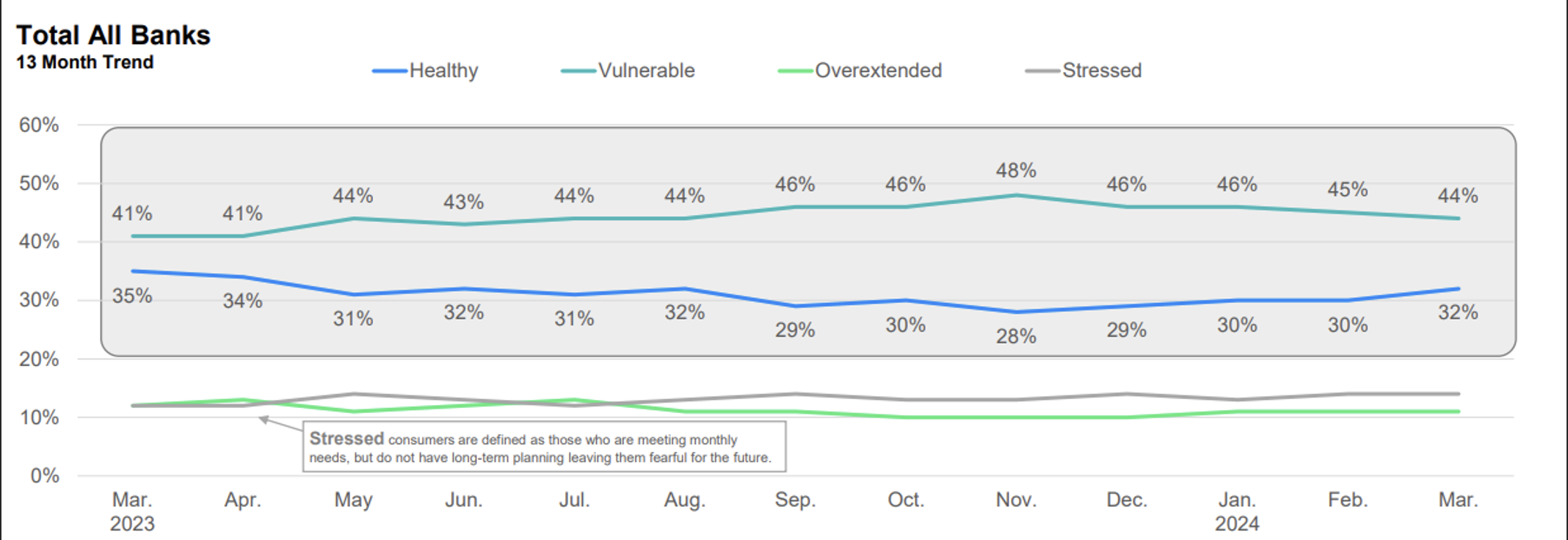

The number of customers who are financially healthy remains steady at 30%, while 45% fall into the vulnerable category.

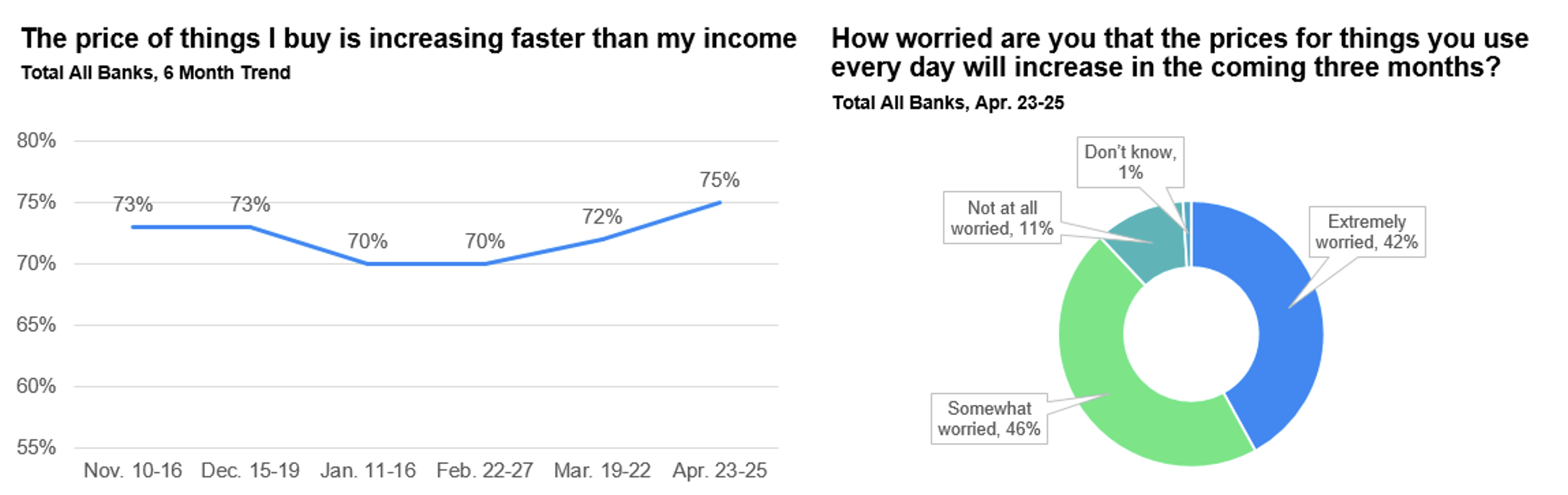

The number of bank customers who say that the cost of goods is increasing faster than their income decreased to 69%, the lowest level this calendar year.

Energy Tensions Rise

Just as inflation concerns have started to subside, a new worry has emerged. Nearly one-third (32%) of customers are extremely worried their energy costs will rise this summer, and 85% are at least somewhat concerned. These fears are highest among vulnerable consumers.

What’s more, more than half (55%) of customers say they are making daily attempts to reduce their energy usage by lowering their consumption, a rate that is highest among stressed customers (65%) and those over the age of 40 (63%). Interestingly, even among financially healthy customers, 55% say they have made daily adjustments, showing the universality of these concerns.

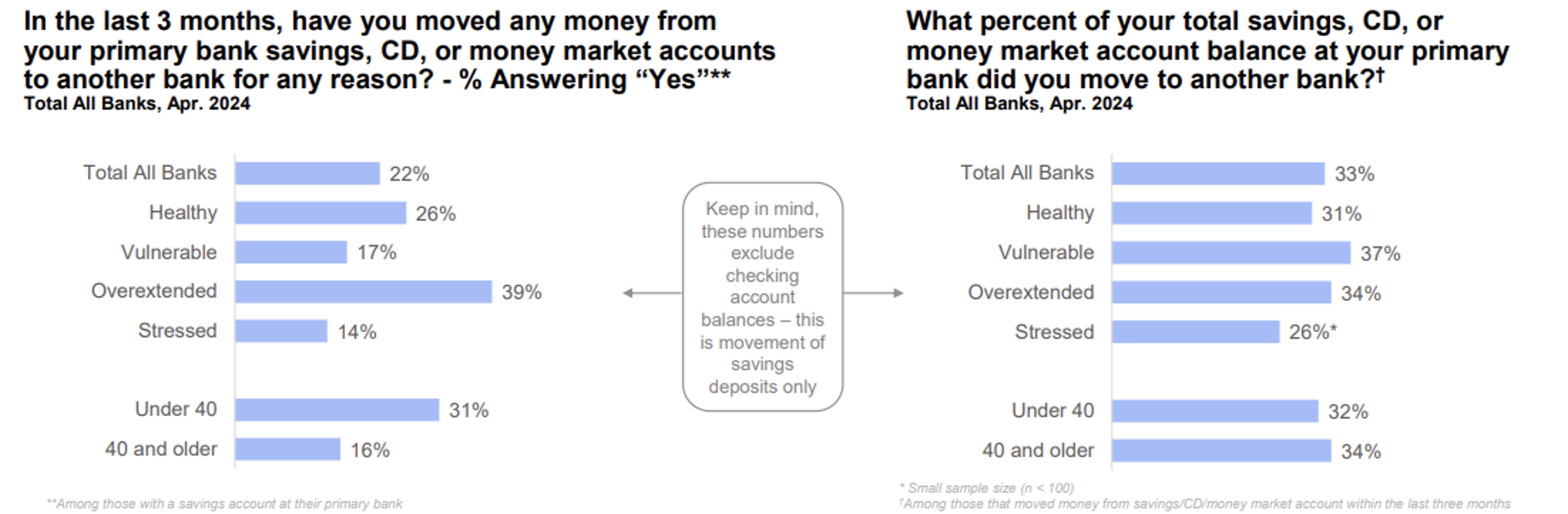

Customers have also begun to get assistance to pay for their utilities. Overall, 13% say that they have received financial assistance from the government or other organizations. The rate is highest for customers that are overextended (20%) and under the age of 40 (17%).

Rising Financial Temperatures

It certainly appears that just as customers have begun to get a reprieve from inflation, energy costs are here to throw everyone a curveball. But the reality is that if it wasn’t energy costs, it would be holiday shopping or travel plans or any other cyclical cost. The truth is that the financial health of customers in the United States has just not recovered yet, and that puts increased pressure on banks to help their customers manage these challenges.

While many banks are well-positioned to come to the rescue with budgeting tools, assistance programs, and a host of other solutions that are available to their customers, those solutions will only help if customers are aware of them and trust the institutions from which they are coming. It’s incumbent on the banks to communicate with their customers and proactively offer personalized help that meets their unique financial needs.

Find out More

This Banking and Payments Intelligence Report is based on responses from 4,000 retail bank customers nationwide and was fielded in June 2024. It was authored by Jennifer White, senior director of banking and payments intelligence at JD Power. Please contact us at the numbers below to connect with Ms. White or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]

[1] JD Power measures the financial health of any consumer as a metric combining their spending/savings ratio, creditworthiness, and safety net items like insurance coverage. Consumers are placed on a continuum from healthy to vulnerable.